You might also like

- Answers HBS Case Goldman Sachs Nikkei Put WarrentDocument8 pagesAnswers HBS Case Goldman Sachs Nikkei Put WarrentSander Chewy67% (3)

- Mile High CyclesDocument3 pagesMile High CyclesAmmar Hassan100% (4)

- Salem Telephone Company Case StudyDocument4 pagesSalem Telephone Company Case StudyTôn Thiện Đức100% (4)

- Danshui Plant No. 2Document2 pagesDanshui Plant No. 2Sahil Kashyap83% (6)

- 16-2 Prestige Telephone CompanyDocument3 pages16-2 Prestige Telephone CompanyYJ26126100% (5)

- Case Study: Danshui Plant No2Document3 pagesCase Study: Danshui Plant No2Abdelhamid JenzriNo ratings yet

- Case Classic Pen Company Activity Based CostingDocument20 pagesCase Classic Pen Company Activity Based CostingAlee Di Vaio83% (6)

- Questions 1 and 2: Costing of A 100-Unit Batch of CS-29 CarburetorsDocument3 pagesQuestions 1 and 2: Costing of A 100-Unit Batch of CS-29 Carburetorsshephard007100% (3)

- Forest GumpDocument12 pagesForest Gumpɹɐʞ Thye100% (2)

- Boston CreameryDocument5 pagesBoston CreameryTheeraphog Phonchuai100% (1)

- Kreative Kasuals Woeking NotesDocument3 pagesKreative Kasuals Woeking NotesAashima GroverNo ratings yet

- Salem CaseDocument4 pagesSalem CaseChris Dunham100% (3)

- Prestige Data ServicesDocument2 pagesPrestige Data ServicesSubrata Dass100% (4)

- Case Study - Prestige Telephone Co.Document12 pagesCase Study - Prestige Telephone Co.James Cullen100% (3)

- SunAir Boat BuildersDocument3 pagesSunAir Boat Buildersram_prabhu00325% (4)

- Precision Motors Division CaseDocument9 pagesPrecision Motors Division CaseAliza Rizvi50% (2)

- SectionB Group16 DanshuiDocument5 pagesSectionB Group16 DanshuiRishabh Vijay100% (1)

- Case Study MOPDocument6 pagesCase Study MOPLorenc BogovikuNo ratings yet

- Solutions Huron AutomotiveDocument13 pagesSolutions Huron Automotiveshreyansh1200% (1)

- Alberta Gauge Company CaseDocument2 pagesAlberta Gauge Company Casenidhu291No ratings yet

- Danshui PlantDocument5 pagesDanshui PlantSabbirAhmedNo ratings yet

- Import Distributors, Inc. : Case 26-1Document2 pagesImport Distributors, Inc. : Case 26-1NishaNo ratings yet

- Bed and Breakfast Business Plan PDFDocument17 pagesBed and Breakfast Business Plan PDFAngela Bau100% (2)

- Prestige Telephone Company (Solutions)Document4 pagesPrestige Telephone Company (Solutions)Joseph Loyola71% (7)

- Assignment - Group 2 - Prestige Telephone CompanyDocument4 pagesAssignment - Group 2 - Prestige Telephone Companyjohnychauhan1No ratings yet

- Prestige Telephone CompanyDocument2 pagesPrestige Telephone Companygharelu10100% (1)

- Horizon InsuranceDocument4 pagesHorizon Insurancemokoto67% (3)

- Lilac Flour Mills: Managerial Accounting and Control - IIDocument9 pagesLilac Flour Mills: Managerial Accounting and Control - IISoni Kumari50% (4)

- Danshui Plant No 2Document5 pagesDanshui Plant No 2Thao Nguyen100% (2)

- Case Solution-Liquid Chemical CompanyDocument2 pagesCase Solution-Liquid Chemical CompanyDHRUV SONAGARANo ratings yet

- Winter Jam Coffee ShopDocument20 pagesWinter Jam Coffee ShopAndra MantaNo ratings yet

- Review For Final ExamDocument4 pagesReview For Final ExamAnkita PanchalNo ratings yet

- Marketing Strategic Plan: Teacher Jose Eduardo Lievano CastiblancoDocument29 pagesMarketing Strategic Plan: Teacher Jose Eduardo Lievano Castiblancoborrasnicolas100% (1)

- Accounting Report - Prestige Telephone CompanyDocument15 pagesAccounting Report - Prestige Telephone CompanyMuhaizarMarkamNo ratings yet

- Prestige Telephone CompanyDocument13 pagesPrestige Telephone CompanyKim Alexis MirasolNo ratings yet

- PrestigeDocument10 pagesPrestigeSumit ChandraNo ratings yet

- Prestige Telephone Company - Question 1Document1 pagePrestige Telephone Company - Question 1Kim Alexis MirasolNo ratings yet

- Case 16-2Document3 pagesCase 16-2gusneri100% (1)

- Draft For Phone RevisionsDocument10 pagesDraft For Phone RevisionsHualu Zhao100% (1)

- Prestige Telephone CompanyDocument5 pagesPrestige Telephone CompanyCylver RoseNo ratings yet

- Prestige TelecommsDocument4 pagesPrestige TelecommsLBS17100% (1)

- Prestige Telephone Company (Online Case Analysis)Document21 pagesPrestige Telephone Company (Online Case Analysis)astha50% (2)

- Case Solution Prestige Telephone ComapnyDocument2 pagesCase Solution Prestige Telephone Comapnygangster91No ratings yet

- Danshui Plant 2Document1 pageDanshui Plant 2Ankit VermaNo ratings yet

- Classic Pen Company CaseDocument16 pagesClassic Pen Company CaseSambit Dash100% (4)

- Danshui Plant 2Document13 pagesDanshui Plant 2Bernard EugineNo ratings yet

- Prestige FinalDocument11 pagesPrestige FinalRahul Tiwari0% (2)

- Danshui Plant 2 - 2019Document19 pagesDanshui Plant 2 - 2019louie florentine Sanchez67% (3)

- Case: Danshui Plant No. 2: Presented By:-Group 9Document7 pagesCase: Danshui Plant No. 2: Presented By:-Group 9LOKESH YADAV100% (2)

- Dhanshui PlantDocument7 pagesDhanshui PlantAkanksha Nikita Khalkho100% (1)

- Hospital Supply, IncDocument3 pagesHospital Supply, Incmade3875% (4)

- Danshui Plant 2 - Group 6 - Section BDocument13 pagesDanshui Plant 2 - Group 6 - Section BSoumyajit Lahiri100% (8)

- ON Prestige Telephone CompanyDocument5 pagesON Prestige Telephone CompanyNivedita NandaNo ratings yet

- Prestige AMA Case StudyDocument9 pagesPrestige AMA Case StudymansNo ratings yet

- ACT1 - Case 2 - Gabriela BecheanuDocument3 pagesACT1 - Case 2 - Gabriela Becheanuadit.goenka0802No ratings yet

- 16 2 Prestige Telephone CompanyDocument3 pages16 2 Prestige Telephone CompanyAnunobi JaneNo ratings yet

- Case 16 2 - Prestige 4343 Additional NotesDocument3 pagesCase 16 2 - Prestige 4343 Additional NotesFedro SusantanaNo ratings yet

- Case Study Salem TelephoneDocument3 pagesCase Study Salem TelephoneahbahkNo ratings yet

- Case Study Salem TelephoneDocument3 pagesCase Study Salem Telephoneahbahk100% (2)

- Prestige Telephone Company SlidesDocument13 pagesPrestige Telephone Company SlidesHarsh MaheshwariNo ratings yet

- Prestige Telephone CompanyDocument2 pagesPrestige Telephone CompanyArbaz AbbasNo ratings yet

- Salem CaseDocument4 pagesSalem CaseNathan YanskyNo ratings yet

- Mmoench - 03 - Homework For Session 3Document6 pagesMmoench - 03 - Homework For Session 3Matt Moench100% (2)

- Prestige Telephone Company Case Study Report UneditedDocument13 pagesPrestige Telephone Company Case Study Report UneditedAmor0% (1)

- Salem Telephone CompanyDocument13 pagesSalem Telephone Companyahujadeepti2581No ratings yet

- Operations Management KeyDocument30 pagesOperations Management KeyNur Al AhadNo ratings yet

- FINN Lect01Document14 pagesFINN Lect01Nur Al AhadNo ratings yet

- The Bass Diffusion ModelDocument2 pagesThe Bass Diffusion ModelNur Al AhadNo ratings yet

- Positioning GuidelinesDocument3 pagesPositioning GuidelinesNur Al Ahad86% (7)

- AdvertisementDocument14 pagesAdvertisementNur Al AhadNo ratings yet

- Case Stuy 004Document4 pagesCase Stuy 004Nur Al AhadNo ratings yet

- High Commission of India, Dhaka: Indian Scholarship Scheme (2012-13)Document4 pagesHigh Commission of India, Dhaka: Indian Scholarship Scheme (2012-13)Nur Al AhadNo ratings yet

- The Modern Mantra For Innovative Management Is "Managerial Effectiveness"Document4 pagesThe Modern Mantra For Innovative Management Is "Managerial Effectiveness"Nur Al AhadNo ratings yet

- Initial Talking On PotatoDocument2 pagesInitial Talking On PotatoNur Al AhadNo ratings yet

- Executive Summary: Description of The BusinessDocument11 pagesExecutive Summary: Description of The BusinessNur Al AhadNo ratings yet

- Calculating GDP in BangladeshDocument5 pagesCalculating GDP in BangladeshNur Al Ahad50% (2)

- Sareers-Standing Out From The PackDocument17 pagesSareers-Standing Out From The PackNur Al AhadNo ratings yet

- Business Laws in Ban Glades 1Document8 pagesBusiness Laws in Ban Glades 1Nur Al AhadNo ratings yet

- Time ValueDocument4 pagesTime ValueNur Al AhadNo ratings yet

- Financial ManagementDocument9 pagesFinancial ManagementNur Al AhadNo ratings yet

- International Marketing Lecture NotesDocument7 pagesInternational Marketing Lecture Notesrahul_kalaniNo ratings yet

- Wharton MBADocument23 pagesWharton MBANur Al AhadNo ratings yet

- Bond ValuationDocument29 pagesBond ValuationNur Al AhadNo ratings yet

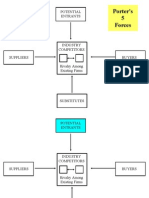

- Porter's 5 Forces: Potential EntrantsDocument25 pagesPorter's 5 Forces: Potential EntrantsNur Al Ahad100% (2)

- Sawyers - CVP AnalysisDocument47 pagesSawyers - CVP AnalysisTrisha Mae AlburoNo ratings yet

- Q. 1 How Will You Use Management Accounting in Corporate Decisions? Elaborate With ExamplesDocument7 pagesQ. 1 How Will You Use Management Accounting in Corporate Decisions? Elaborate With ExamplesParvathyNo ratings yet

- Assignment Leverage and Capital StructureDocument6 pagesAssignment Leverage and Capital StructureCristopherson PerezNo ratings yet

- Ma2chapter PDFDocument42 pagesMa2chapter PDFLinh LeNo ratings yet

- Topics: Break-Even Analysis, Operating and Financial Leverage, and Optimal Capital StructureDocument5 pagesTopics: Break-Even Analysis, Operating and Financial Leverage, and Optimal Capital StructuremagoimoiNo ratings yet

- Accounting For Managers: Prof. Dr. Mohamed YoussefDocument34 pagesAccounting For Managers: Prof. Dr. Mohamed Youssefrahmat idrusNo ratings yet

- Check Figures For Problems and Cases Ray Garrison and Eric Noreen Managerial Accounting, 10 EditionDocument5 pagesCheck Figures For Problems and Cases Ray Garrison and Eric Noreen Managerial Accounting, 10 EditionSheennah Lee LimNo ratings yet

- Managerial Accounting: Standard MBA ProgramDocument33 pagesManagerial Accounting: Standard MBA ProgramAnne KawNo ratings yet

- 2016 MSC Cut-Off Grade Optimisation For A Bimetallic DepositDocument126 pages2016 MSC Cut-Off Grade Optimisation For A Bimetallic DepositYusuf Efe OzdemirNo ratings yet

- Session 12 CVP AnalysisDocument52 pagesSession 12 CVP Analysismuskan mittalNo ratings yet

- Nam NamDocument50 pagesNam NamDaNn UyNo ratings yet

- Cyber Café and Xerox Lamination: Profile No.: 143 NIC Code: 63992Document11 pagesCyber Café and Xerox Lamination: Profile No.: 143 NIC Code: 63992Shivam SyalNo ratings yet

- CH - 5 - Break Even AnalysisDocument48 pagesCH - 5 - Break Even AnalysisNitish KhatanaNo ratings yet

- Name: Score: Course & Section: DateDocument11 pagesName: Score: Course & Section: DateDan RyanNo ratings yet

- Property Management Business Plan ExampleDocument32 pagesProperty Management Business Plan ExampleSomNo ratings yet

- Sem Vi Tybcom Cost PDFDocument3 pagesSem Vi Tybcom Cost PDFYogesh GiriNo ratings yet

- Appendix A Pricing Products and ServicesDocument23 pagesAppendix A Pricing Products and ServicesJaved AhmedNo ratings yet

- Chapter 16 - Costs, Scale of Production and Break-Even AnalysisDocument3 pagesChapter 16 - Costs, Scale of Production and Break-Even AnalysisSol CarvajalNo ratings yet

- ENT05 Course Syllabus AY 16-17Document20 pagesENT05 Course Syllabus AY 16-17Aleezah Gertrude RegadoNo ratings yet

- SM Roberta S. Russell Ch02 8eDocument20 pagesSM Roberta S. Russell Ch02 8eImbaguestNo ratings yet

- Capitulo 4 Contabilidad Gerencial para EnviarDocument5 pagesCapitulo 4 Contabilidad Gerencial para EnviarDaniel RuizNo ratings yet

- GSCG Casebook (Oct 2015)Document150 pagesGSCG Casebook (Oct 2015)yahya_c100% (3)

- A. Contribution Margin: AnswerDocument3 pagesA. Contribution Margin: Answerrook semayNo ratings yet

- Kingfisher Senior High School: Marketing PlanDocument38 pagesKingfisher Senior High School: Marketing PlanMuyano, Mira Joy M.No ratings yet

- Breif Marketting Mix 7psDocument16 pagesBreif Marketting Mix 7psMarco IbrahimNo ratings yet