You might also like

- NREL Wind To Hydrogen Project - Renewable Hydrogen Production For Energy Storage & Transportation PDFDocument26 pagesNREL Wind To Hydrogen Project - Renewable Hydrogen Production For Energy Storage & Transportation PDFJosePPMolinaNo ratings yet

- Hydropower Market Report - Executive SummaryDocument8 pagesHydropower Market Report - Executive Summaryhimiko togaNo ratings yet

- Guidelines For Grid Connected Solar Rooftop Program Under SOURA GRUHA YOJANE (SGY) Scheme For FY 2019-20Document5 pagesGuidelines For Grid Connected Solar Rooftop Program Under SOURA GRUHA YOJANE (SGY) Scheme For FY 2019-20sapmayanNo ratings yet

- 212Document58 pages212aliNo ratings yet

- A123 20AH Data SheetDocument2 pagesA123 20AH Data SheetXavier ReibánNo ratings yet

- Renewable Energy (Re) Resources: Philippine Wholesale Electricity Spot Market (Wesm)Document17 pagesRenewable Energy (Re) Resources: Philippine Wholesale Electricity Spot Market (Wesm)Jonathan SantiagoNo ratings yet

- Status of Allocation of Bays-FinalDocument6 pagesStatus of Allocation of Bays-FinalRaji VydaniNo ratings yet

- Ererer PDFDocument24 pagesErerer PDFkishorNo ratings yet

- 2.1. China Wind Market Is Booming by L. JunfengDocument31 pages2.1. China Wind Market Is Booming by L. Junfengquantum_leap_windNo ratings yet

- Product Flyer MT - en 50 - 80kw ReadDocument2 pagesProduct Flyer MT - en 50 - 80kw ReadsyamprasadNo ratings yet

- Pensana PLC Corporate Presentation Spring 2022Document24 pagesPensana PLC Corporate Presentation Spring 202210evenwoodcloseNo ratings yet

- SDT 4 15kw ReadDocument2 pagesSDT 4 15kw ReadDan DepNo ratings yet

- China Wind Market Is Booming: - : Growth Not Only On-Shore But Off-ShoreDocument31 pagesChina Wind Market Is Booming: - : Growth Not Only On-Shore But Off-ShoreycexcelNo ratings yet

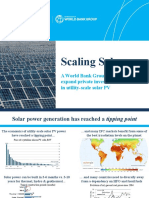

- 04-Scaling-Solar External-Presentation Global English Jan17Document16 pages04-Scaling-Solar External-Presentation Global English Jan17Amit KumarNo ratings yet

- Attachment - Fuel Demand Calculation For Marina VesselsDocument1 pageAttachment - Fuel Demand Calculation For Marina VesselsFranz OttNo ratings yet

- EnglishDocument12 pagesEnglishNagNo ratings yet

- Growatt 1200 - 1500 TL3-SDocument1 pageGrowatt 1200 - 1500 TL3-SmatthieuNo ratings yet

- SDG Investment Fair 2022 - 11april22-Reviewed - SEGEPLAN (1) CPKDCDocument13 pagesSDG Investment Fair 2022 - 11april22-Reviewed - SEGEPLAN (1) CPKDCCeciliaPivaralNo ratings yet

- Elan - 72 5BB P-Type PERC Bifacial PV ModuleDocument2 pagesElan - 72 5BB P-Type PERC Bifacial PV Modulenitin9860No ratings yet

- Sro 575 I 2019 22-05-2019Document4 pagesSro 575 I 2019 22-05-2019Saira JawedNo ratings yet

- GROWATT Three Phase InverterDocument6 pagesGROWATT Three Phase InverterAlexandru ImrehNo ratings yet

- Rbain1209 PDFDocument31 pagesRbain1209 PDFRopiudin EnergiNo ratings yet

- Africa CEC Session 3 - Ministry of Water and Energy Ethiopia - Beyene - 220613Document33 pagesAfrica CEC Session 3 - Ministry of Water and Energy Ethiopia - Beyene - 220613adaneNo ratings yet

- Glamox - GMO Onshore Catalouge2017Document26 pagesGlamox - GMO Onshore Catalouge2017Enling GohNo ratings yet

- SGY Revised Guidelines 1Document5 pagesSGY Revised Guidelines 1Aziz AhemadNo ratings yet

- Cost AccountingDocument5 pagesCost Accountingjaveria saherNo ratings yet

- SPF3000TL HVM48Document1 pageSPF3000TL HVM48Isaak TladiNo ratings yet

- Growatt 2500TL 6000TL XDocument1 pageGrowatt 2500TL 6000TL Xjoelleyser01No ratings yet

- Invest NE 2019 Brochure Final e VersionDocument28 pagesInvest NE 2019 Brochure Final e VersionWing CrabNo ratings yet

- Pampa Camarones High Grade Copper Operation in Chile: The CompanyDocument1 pagePampa Camarones High Grade Copper Operation in Chile: The CompanyBotacura Minerals acuña moralesNo ratings yet

- Benchmark Order FY 2019-20Document2 pagesBenchmark Order FY 2019-20sricharan majhiNo ratings yet

- Characterization of Da/dn Test Results at Negative Stress Ratios and Incorporation in Damage Tolerance Life PredictionsDocument25 pagesCharacterization of Da/dn Test Results at Negative Stress Ratios and Incorporation in Damage Tolerance Life PredictionspuhumightNo ratings yet

- 169339868707status of Bay Allocation 31.07.2023Document9 pages169339868707status of Bay Allocation 31.07.2023Vaibhav KapoorNo ratings yet

- Lol 10-03Document1 pageLol 10-03elvisxt300No ratings yet

- Economics 3rd Edition Krugman Solutions ManualDocument35 pagesEconomics 3rd Edition Krugman Solutions Manualsalariedshopbook.gczx100% (27)

- Dwnload Full Economics 3rd Edition Krugman Solutions Manual PDFDocument35 pagesDwnload Full Economics 3rd Edition Krugman Solutions Manual PDFpaulettechandlerh7i9100% (13)

- Entarara BoreholeDocument1 pageEntarara Boreholestifler 254No ratings yet

- Why Nuclear Electricity For India?Document40 pagesWhy Nuclear Electricity For India?Anuradha KaliaNo ratings yet

- Dr. Arunachalam PresentationDocument40 pagesDr. Arunachalam PresentationinnocentshahNo ratings yet

- Why Nuclear Electricity For India?Document40 pagesWhy Nuclear Electricity For India?santhoshvspNo ratings yet

- UOP FCC Bitumen Processing Case StudyDocument22 pagesUOP FCC Bitumen Processing Case Studysaleh4060No ratings yet

- Sofar HYD 5K 20KTL 3PHDocument1 pageSofar HYD 5K 20KTL 3PHEdy EdwardNo ratings yet

- System Voltage Considerations: Section 4Document4 pagesSystem Voltage Considerations: Section 4harmlesdragonNo ratings yet

- Yiguang 2018Document6 pagesYiguang 2018Abir HezziNo ratings yet

- Presentación Técnica #06 - Roudnev Aleks - Weir Minerals PDFDocument167 pagesPresentación Técnica #06 - Roudnev Aleks - Weir Minerals PDFclaudiovillNo ratings yet

- Cost Trends For Offshore WindDocument17 pagesCost Trends For Offshore WindMohamed Al-OdatNo ratings yet

- Macroeconomics 2nd Edition Krugman Solutions ManualDocument35 pagesMacroeconomics 2nd Edition Krugman Solutions Manualzeusplanchetzeck1100% (19)

- Dwnload Full Macroeconomics 2nd Edition Krugman Solutions Manual PDFDocument35 pagesDwnload Full Macroeconomics 2nd Edition Krugman Solutions Manual PDFdunderexpugner7scf100% (8)

- Lecture 2 Design Controlsand Criteria Part 2Document16 pagesLecture 2 Design Controlsand Criteria Part 2Ndanu MercyNo ratings yet

- Haytham Ibrahim's Assignment No.3 PDFDocument10 pagesHaytham Ibrahim's Assignment No.3 PDFAhmed KhairiNo ratings yet

- 2018 09 26 Product Show Track 3 Session 1 CoiroDocument17 pages2018 09 26 Product Show Track 3 Session 1 CoiroVarun ZotaNo ratings yet

- Se HD Wave Single Phase Inverter Datasheet Na 2018 10Document2 pagesSe HD Wave Single Phase Inverter Datasheet Na 2018 10jy4661No ratings yet

- Torqeedo - Onepager - Cruise-RT - 2021 - EN - RGB - 210211Document2 pagesTorqeedo - Onepager - Cruise-RT - 2021 - EN - RGB - 210211Dedi MisbahNo ratings yet

- Annual Report On US Wind Power Perfomance Trends-2007 (Presentation)Document45 pagesAnnual Report On US Wind Power Perfomance Trends-2007 (Presentation)erickcastro77No ratings yet

- Shore Power: Applicability and AssumptionsDocument5 pagesShore Power: Applicability and AssumptionsmattiturboNo ratings yet

- HidropowerDocument7 pagesHidropowerCarlos Alberto Llamoca IngaNo ratings yet

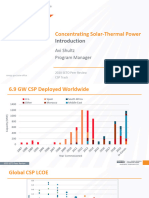

- 2020 SETO Peer Review Breakout Presentations - Concentrating Solar-Thermal PowerDocument31 pages2020 SETO Peer Review Breakout Presentations - Concentrating Solar-Thermal PowerAmlr FadilrNo ratings yet

- Microeconomics Canadian 2nd Edition Krugman Solutions ManualDocument35 pagesMicroeconomics Canadian 2nd Edition Krugman Solutions Manualimbreedjejunity.8hi2yz100% (19)

- Rechargeable Sealed Lead-Acid Battery: 6 Volt 4.5 Amp. HrsDocument2 pagesRechargeable Sealed Lead-Acid Battery: 6 Volt 4.5 Amp. HrsJuan EsNo ratings yet

- Engleza Referat-Pantilimonescu IonutDocument13 pagesEngleza Referat-Pantilimonescu IonutAilenei RazvanNo ratings yet

- Sundar Pichai PDFDocument6 pagesSundar Pichai PDFHimanshi Patle100% (1)

- Mission and VisionDocument5 pagesMission and VisionsanjedNo ratings yet

- SCERT Kerala State Syllabus 9th Standard English Textbooks Part 1-1Document104 pagesSCERT Kerala State Syllabus 9th Standard English Textbooks Part 1-1Athulya ThondangattilNo ratings yet

- Tangerine - Breakfast Set Menu Wef 16 Dec UpdatedDocument3 pagesTangerine - Breakfast Set Menu Wef 16 Dec Updateddeveloper louNo ratings yet

- Toolbox TalkDocument14 pagesToolbox Talkcall_mustafas2361No ratings yet

- Dry Compressing Vacuum PumpsDocument62 pagesDry Compressing Vacuum PumpsAnonymous zwSP5gvNo ratings yet

- Words of Radiance: Book Two of The Stormlight Archive - Brandon SandersonDocument6 pagesWords of Radiance: Book Two of The Stormlight Archive - Brandon Sandersonxyrytepa0% (3)

- Ch-10 Human Eye Notes FinalDocument27 pagesCh-10 Human Eye Notes Finalkilemas494No ratings yet

- 25 Middlegame Concepts Every Chess Player Must KnowDocument2 pages25 Middlegame Concepts Every Chess Player Must KnowKasparicoNo ratings yet

- Hockney-Falco Thesis: 1 Setup of The 2001 PublicationDocument6 pagesHockney-Falco Thesis: 1 Setup of The 2001 PublicationKurayami ReijiNo ratings yet

- Csir Life Sciences Fresh Instant NotesDocument4 pagesCsir Life Sciences Fresh Instant NotesAlps Ana33% (3)

- Imabalacat DocuDocument114 pagesImabalacat DocuJänrëýMåmårìlSälängsàngNo ratings yet

- CII Sohrabji Godrej GreenDocument30 pagesCII Sohrabji Godrej GreenRITHANYAA100% (2)

- Grade 7 Nap MayDocument6 pagesGrade 7 Nap Mayesivaks2000No ratings yet

- SG110CX: Multi-MPPT String Inverter For SystemDocument2 pagesSG110CX: Multi-MPPT String Inverter For SystemKatherine SmithNo ratings yet

- Noise and DB Calculations: Smart EDGE ECE Review SpecialistDocument2 pagesNoise and DB Calculations: Smart EDGE ECE Review SpecialistLM BecinaNo ratings yet

- Mushroom Project - Part 1Document53 pagesMushroom Project - Part 1Seshadev PandaNo ratings yet

- Answers For Some QuestionsDocument29 pagesAnswers For Some Questionsyogeshdhuri22No ratings yet

- Optimized Maximum Power Point Tracker For Fast Changing Environmental ConditionsDocument7 pagesOptimized Maximum Power Point Tracker For Fast Changing Environmental ConditionsSheri ShahiNo ratings yet

- Introduction To EthicsDocument18 pagesIntroduction To EthicsMarielle Guerra04No ratings yet

- Lab 3 Arduino Led Candle Light: CS 11/group - 4 - Borromeo, Galanida, Pabilan, Paypa, TejeroDocument3 pagesLab 3 Arduino Led Candle Light: CS 11/group - 4 - Borromeo, Galanida, Pabilan, Paypa, TejeroGladys Ruth PaypaNo ratings yet

- IR2153 Parte6Document1 pageIR2153 Parte6FRANK NIELE DE OLIVEIRANo ratings yet

- Li JinglinDocument3 pagesLi JinglincorneliuskooNo ratings yet

- Smart Door Lock System Using Face RecognitionDocument5 pagesSmart Door Lock System Using Face RecognitionIJRASETPublicationsNo ratings yet

- Is 2 - 2000 Rules For Rounded Off For Numericals PDFDocument18 pagesIs 2 - 2000 Rules For Rounded Off For Numericals PDFbala subramanyamNo ratings yet

- Multinational MarketingDocument11 pagesMultinational MarketingraghavelluruNo ratings yet

- Project Quality Plan (JFJS-788)Document18 pagesProject Quality Plan (JFJS-788)mominNo ratings yet

- Very Narrow Aisle MTC Turret TruckDocument6 pagesVery Narrow Aisle MTC Turret Truckfirdaushalam96No ratings yet