You might also like

- The Investor's Guide to Investing in Direct Participation Oil and Gas ProgramsFrom EverandThe Investor's Guide to Investing in Direct Participation Oil and Gas ProgramsRating: 5 out of 5 stars5/5 (1)

- Exam NotesDocument7 pagesExam NotesAmit VadiNo ratings yet

- Philippine Income Taxation - IncomeDocument48 pagesPhilippine Income Taxation - IncomeJenny Malabrigo, MBANo ratings yet

- Chapter 3 Concept of IncomeDocument12 pagesChapter 3 Concept of IncomeGlomarie GonayonNo ratings yet

- Module 6 CGT - 1Document3 pagesModule 6 CGT - 1Marklein DumangengNo ratings yet

- Dividend Policy: e As Cost of Equity in TheDocument43 pagesDividend Policy: e As Cost of Equity in TheVelayudham ThiyagarajanNo ratings yet

- Income Taxation Module 3 Concept of IncomeDocument24 pagesIncome Taxation Module 3 Concept of IncomeRichel San AgustinNo ratings yet

- Questions Financial Accouing 1-Year 1-Sem MbaDocument7 pagesQuestions Financial Accouing 1-Year 1-Sem Mbakingmaker9999No ratings yet

- Profit Is A Fundamental Concept in Economics and BDocument1 pageProfit Is A Fundamental Concept in Economics and BYenula StephanosNo ratings yet

- Definition of Corporate Finance: 2. Who Is The Head of Finance in Corporation?Document11 pagesDefinition of Corporate Finance: 2. Who Is The Head of Finance in Corporation?Ismail HossainNo ratings yet

- Financial StatementsDocument12 pagesFinancial StatementsJonabed PobadoraNo ratings yet

- 5th Semester Finance True False FullDocument12 pages5th Semester Finance True False FullTorreus Adhikari75% (4)

- Dealings in Property NotesDocument6 pagesDealings in Property NotesLinrhay RicohermosoNo ratings yet

- Notes On Income TaxationDocument21 pagesNotes On Income TaxationBen Dela Cruz100% (2)

- Definition of Corporate Finance: 2. Who Is The Head of Finance in Corporation?Document12 pagesDefinition of Corporate Finance: 2. Who Is The Head of Finance in Corporation?AshrafulNo ratings yet

- F3 Chapter 1Document14 pagesF3 Chapter 1Ali ShahnawazNo ratings yet

- Module 13 Regular Deductions 3Document16 pagesModule 13 Regular Deductions 3Donna Mae FernandezNo ratings yet

- Dividend Policy: e As Cost of Equity in TheDocument43 pagesDividend Policy: e As Cost of Equity in TheBala RanganathNo ratings yet

- TaxationDocument5 pagesTaxationHyuga NejiNo ratings yet

- MSJG Income Tax Chapter 3 NotesDocument3 pagesMSJG Income Tax Chapter 3 NotesMar Sean Jan GabiosaNo ratings yet

- Business Unit 3Document8 pagesBusiness Unit 3akanksha nandaNo ratings yet

- Business Review Chapter 3Document18 pagesBusiness Review Chapter 3TanishNo ratings yet

- Engineering Economy TermsDocument5 pagesEngineering Economy TermsRio PerezNo ratings yet

- The Costs of Production: HeadingDocument4 pagesThe Costs of Production: HeadingAn KhanhNo ratings yet

- Coroporate FinanceDocument21 pagesCoroporate FinanceWijdane BroukiNo ratings yet

- Gross Income - WPS OfficeDocument3 pagesGross Income - WPS OfficeNour Aira NaoNo ratings yet

- Business Math 1Document2 pagesBusiness Math 1Ralph EgeNo ratings yet

- ZOLINA, ZANDRIX WEN B. - Homework 1Document3 pagesZOLINA, ZANDRIX WEN B. - Homework 1ZOLINA, ZANDRIX WEN B.No ratings yet

- SUBJECT CODE & NAME MCC 401 & Management of Financial ServicesDocument6 pagesSUBJECT CODE & NAME MCC 401 & Management of Financial ServicesMrinal KalitaNo ratings yet

- Chap 12 CapitalDocument5 pagesChap 12 CapitalTyra Lim Ah KenNo ratings yet

- Present Value: Rate Return Investment Percentage AmountDocument6 pagesPresent Value: Rate Return Investment Percentage AmountArs KhanNo ratings yet

- Income Tax (1) - FinalDocument50 pagesIncome Tax (1) - FinalMay Encarnina P. Gaoiran100% (5)

- PFTP PostMidsemDocument236 pagesPFTP PostMidsemMS ArshaqNo ratings yet

- Solution Manual For Financial Management Theory and Practice 14th Edition by Brigham and Ehrhardt ISBN 1111972214 9781111972219Document36 pagesSolution Manual For Financial Management Theory and Practice 14th Edition by Brigham and Ehrhardt ISBN 1111972214 9781111972219caseywestfmjcgodkzr100% (22)

- Accounting Terms: DirectionDocument5 pagesAccounting Terms: Directionkthesmart4No ratings yet

- 8TH Sem Tax Paper PDFDocument25 pages8TH Sem Tax Paper PDFAnamika VatsaNo ratings yet

- Topic 3: Finance Chapter 11: Role of Financial Management Strategic Role of Financial ManagementDocument12 pagesTopic 3: Finance Chapter 11: Role of Financial Management Strategic Role of Financial Managementstregas123No ratings yet

- Group-3 Forro Written ReportDocument3 pagesGroup-3 Forro Written ReportShaira BaltazarNo ratings yet

- 4 Revenue AccountsDocument1 page4 Revenue Accountsapi-299265916No ratings yet

- Chapter 4 - Gross IncomeDocument9 pagesChapter 4 - Gross Incomechesca marie penarandaNo ratings yet

- Finance InterviewDocument23 pagesFinance InterviewArpit MalviyaNo ratings yet

- Gross Income: Module No. 3-4 Inclusive Week: August 23-27, 2021 Module Overview Reference / Research LinksDocument13 pagesGross Income: Module No. 3-4 Inclusive Week: August 23-27, 2021 Module Overview Reference / Research LinksHeigh Ven100% (1)

- Unit 5 - Inclusions & Exclusions To Bus & Other Sources of IncomeDocument10 pagesUnit 5 - Inclusions & Exclusions To Bus & Other Sources of IncomeJoseph Anthony RomeroNo ratings yet

- Finance Management Notes MbaDocument12 pagesFinance Management Notes MbaSandeep Kumar SahaNo ratings yet

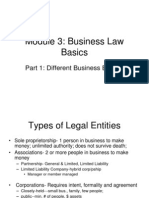

- Business Law - BasicDocument30 pagesBusiness Law - BasicGama Kristian AdikurniaNo ratings yet

- Capital Budgeting Cash Flows: Answers To Review Questions 8-1Document5 pagesCapital Budgeting Cash Flows: Answers To Review Questions 8-1Asere JazminNo ratings yet

- Cost of CapitalDocument18 pagesCost of CapitalAishvarya PujarNo ratings yet

- Income From Business/ProfessionDocument3 pagesIncome From Business/Professionubaid7491No ratings yet

- Solution Manual For Corporate Finance A Focused Approach 5th Edition by Ehrhardt Brigham ISBN 1133947530 9781133947530Document36 pagesSolution Manual For Corporate Finance A Focused Approach 5th Edition by Ehrhardt Brigham ISBN 1133947530 9781133947530heathernashdnjbczemra100% (24)

- Unit 3 - FinanceDocument16 pagesUnit 3 - Financeadriana zugastiNo ratings yet

- KodigoDocument3 pagesKodigostructural mechanicsNo ratings yet

- Inctax Lecture Notes Froup 2 and 6Document27 pagesInctax Lecture Notes Froup 2 and 6KrizahMarieCaballeroNo ratings yet

- Accounting ExamplesDocument124 pagesAccounting ExamplesGirish KhareNo ratings yet

- Corporate Finance Notes 3Document11 pagesCorporate Finance Notes 3ccapgomesNo ratings yet

- TAX1 ReviewerDocument97 pagesTAX1 ReviewerAbdulwahid MadumNo ratings yet

- Topic 3: Finance Chapter 11: Role of Financial Management Strategic Role of Financial ManagementDocument12 pagesTopic 3: Finance Chapter 11: Role of Financial Management Strategic Role of Financial ManagementNikolas CiniNo ratings yet

- Lesson 6 Tax Planning With Reference To Specific Magement DecisionDocument49 pagesLesson 6 Tax Planning With Reference To Specific Magement DecisionkelvinNo ratings yet

- Becker REG - Chapter 1 OutlineDocument5 pagesBecker REG - Chapter 1 OutlineCassandra TangNo ratings yet

- Accounting I Crib SheetDocument1 pageAccounting I Crib SheetschinniNo ratings yet

- Leave RulesDocument10 pagesLeave RulesjijinaNo ratings yet

- Poverty Affidavit 2021Document5 pagesPoverty Affidavit 2021Almir OmerovicNo ratings yet

- Social Security System: Updates On The Core ProcessesDocument3 pagesSocial Security System: Updates On The Core ProcessesSam LagoNo ratings yet

- ACCA F7 December 2015 NotesDocument280 pagesACCA F7 December 2015 NotesopentuitionID100% (3)

- Informatica Tool 7.5 Years of Experience ResumeDocument6 pagesInformatica Tool 7.5 Years of Experience ResumeShruti SharmaNo ratings yet

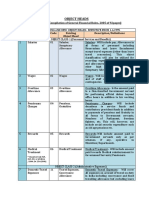

- Object Head List PDFDocument6 pagesObject Head List PDFLal ZahawmaNo ratings yet

- Om 6cpc PDFDocument36 pagesOm 6cpc PDFmaxie1024No ratings yet

- Deepak Esidential Status - Important NoteDocument1 pageDeepak Esidential Status - Important NoteDeepak YadavNo ratings yet

- AP PRC 10 Pensions HPL FormulaDocument3 pagesAP PRC 10 Pensions HPL FormulaSEKHARNo ratings yet

- Compendium 8th EditionDocument251 pagesCompendium 8th EditiondfgNo ratings yet

- De Smith & Teri Patterson E-MailsDocument2 pagesDe Smith & Teri Patterson E-MailsRobert LeeNo ratings yet

- Employee ExitPolicy PDFDocument3 pagesEmployee ExitPolicy PDFNarayanshankar S S100% (1)

- Atal Pension YojanaDocument2 pagesAtal Pension YojanakrithikNo ratings yet

- PP PDFDocument12 pagesPP PDFavinash reddyNo ratings yet

- Employee DataDocument1 pageEmployee DataomkassNo ratings yet

- Best Judgment AssessmentDocument9 pagesBest Judgment AssessmentkagalwalaaNo ratings yet

- General Provident Fund RulesDocument65 pagesGeneral Provident Fund RulesAhmed FawadNo ratings yet

- Tqas - General MathematicsDocument4 pagesTqas - General MathematicsSamuel T. Catulpos Jr.No ratings yet

- Lalit Mohan Pandey Uttarakhand PensionDocument3 pagesLalit Mohan Pandey Uttarakhand PensionRajeshPandeyNo ratings yet

- 18 - IND AS 19 - Employee Benefit - Final (R)Document28 pages18 - IND AS 19 - Employee Benefit - Final (R)S Bharhath kumarNo ratings yet

- MST 111 ReviewerDocument10 pagesMST 111 ReviewerJohn MichaelNo ratings yet

- LIC Superannuation Claim FormDocument3 pagesLIC Superannuation Claim FormKrishnakumar100% (1)

- Payment Receipt 0005743148Document1 pagePayment Receipt 0005743148Chitradeep FalguniyaNo ratings yet

- Payroll Canadian 1St Edition Dryden Test Bank Full Chapter PDFDocument37 pagesPayroll Canadian 1St Edition Dryden Test Bank Full Chapter PDFhebexuyenod8q100% (6)

- Income From SalariesDocument15 pagesIncome From SalariesAyesha MominNo ratings yet

- Orissa Development Authorities Act, 1982Document62 pagesOrissa Development Authorities Act, 1982Latest Laws TeamNo ratings yet

- Tax Rebyuwer MidtermDocument12 pagesTax Rebyuwer MidtermChua chua100% (1)

- AFCA - Rules PDFDocument50 pagesAFCA - Rules PDFkkNo ratings yet

- Taxes On Savings: Jonathan Gruber Public Finance and Public PolicyDocument51 pagesTaxes On Savings: Jonathan Gruber Public Finance and Public PolicyGaluh WicaksanaNo ratings yet

- App1616765 PDFDocument2 pagesApp1616765 PDFRutik MoreNo ratings yet