You might also like

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesFrom EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesNo ratings yet

- XX. CIR vs. Fitness by Design, IncDocument11 pagesXX. CIR vs. Fitness by Design, IncStef OcsalevNo ratings yet

- BIR Ruling DA - VAT-021 121-10Document3 pagesBIR Ruling DA - VAT-021 121-10Jemila Paula Diala100% (1)

- GSTV70P4 November 27 December 3 (PG 144) SamplechapterDocument2 pagesGSTV70P4 November 27 December 3 (PG 144) SamplechapterSatyakanth SunkaraNo ratings yet

- CIRT Audit Report Highlights Rs. 423m IrregularitiesDocument27 pagesCIRT Audit Report Highlights Rs. 423m IrregularitiesHamid AliNo ratings yet

- BIR Ruling DA - C-018 075-10Document2 pagesBIR Ruling DA - C-018 075-10Mark Lord Morales BumagatNo ratings yet

- BIR Ruling 9.15.2009Document3 pagesBIR Ruling 9.15.2009Larry Tobias Jr.No ratings yet

- ELP IDT Newsletter April 2023 FinalDocument12 pagesELP IDT Newsletter April 2023 FinalELP LawNo ratings yet

- Sample Memo on Tax Fraud AuditDocument1 pageSample Memo on Tax Fraud AuditClarissa SawaliNo ratings yet

- Attachment 1Document2 pagesAttachment 1khabrilaalNo ratings yet

- CR Islr OriginalDocument1 pageCR Islr OriginalGeraldine AlvarezNo ratings yet

- The Institute of Chartered Accountants of IndiaDocument42 pagesThe Institute of Chartered Accountants of IndiaXpacNo ratings yet

- 2020 Tax Updates: Key SC and CTA Rulings on Income Tax and VATDocument12 pages2020 Tax Updates: Key SC and CTA Rulings on Income Tax and VATCarlota VillaromanNo ratings yet

- GST Automated NoticesDocument6 pagesGST Automated NoticesMaunik ParikhNo ratings yet

- 2307 FormDocument3 pages2307 FormK and F Construction Dev't CorpNo ratings yet

- TAX UPDATES SEMINAR KEY COURT RULINGSDocument9 pagesTAX UPDATES SEMINAR KEY COURT RULINGSJennilyn TugelidaNo ratings yet

- AnkitDocument4 pagesAnkitsitNo ratings yet

- Jammu& Kashmir.: (Package: GTI-03)Document12 pagesJammu& Kashmir.: (Package: GTI-03)Gulshan MaanNo ratings yet

- EFPS Home - EFiling and Payment SystemDocument2 pagesEFPS Home - EFiling and Payment SystemJinkieNo ratings yet

- GST Audit Amendment Notes by Pankaj GargDocument12 pagesGST Audit Amendment Notes by Pankaj GargGopal Airan100% (2)

- Deputy Commissioner Reports on Wealth Statement and Tax Audit IssuesDocument6 pagesDeputy Commissioner Reports on Wealth Statement and Tax Audit IssuesMajid SaeedNo ratings yet

- Tax office audit report on Hyundai EngineeringDocument2 pagesTax office audit report on Hyundai EngineeringShahaan ZulfiqarNo ratings yet

- RMO No.34-2018Document3 pagesRMO No.34-2018kkabness101 YULNo ratings yet

- B4-NOV-MSDocument13 pagesB4-NOV-MSCerealis FelicianNo ratings yet

- Field Training Report 127411Document7 pagesField Training Report 127411deepak mauryaNo ratings yet

- Accounting Ledgers and Entries in GST: CMA Bhogavalli Mallikarjuna GuptaDocument6 pagesAccounting Ledgers and Entries in GST: CMA Bhogavalli Mallikarjuna GuptaRohan KulkarniNo ratings yet

- CA Final GST and Customs Flow Charts Nov 2018Document173 pagesCA Final GST and Customs Flow Charts Nov 2018Amar ShahNo ratings yet

- 2019 To 2015 TAX BAR Q ADocument87 pages2019 To 2015 TAX BAR Q AJade Ligan EliabNo ratings yet

- RR 22-2020 (Notice of Discrepancy) PDFDocument3 pagesRR 22-2020 (Notice of Discrepancy) PDFilovelawschoolNo ratings yet

- RMO No. 6-2023Document11 pagesRMO No. 6-2023Anostasia NemusNo ratings yet

- India Localization & VAT With Respect To SD: Kumar ArmugamDocument47 pagesIndia Localization & VAT With Respect To SD: Kumar ArmugamjkanoongoNo ratings yet

- Deferred Tax CalculatorDocument2 pagesDeferred Tax Calculatoramitanshu chaturvediNo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- Gujarat Revenue 2011 Chap 5Document42 pagesGujarat Revenue 2011 Chap 5Anurag YadavNo ratings yet

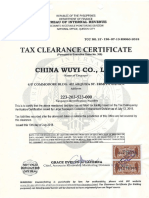

- REPUBLIC OF THE PHILIPPINES TAX CLEARANCE CERTIFICATEDocument1 pageREPUBLIC OF THE PHILIPPINES TAX CLEARANCE CERTIFICATEliuNo ratings yet

- Tax Administration/ Reforms in Pakistan: Fazal Amin ShahDocument12 pagesTax Administration/ Reforms in Pakistan: Fazal Amin ShahMubashir SheheryarNo ratings yet

- GST-RFD-01 Application for Refund of ITC on Export of Goods & ServicesDocument3 pagesGST-RFD-01 Application for Refund of ITC on Export of Goods & ServiceskotisanampudiNo ratings yet

- RMC No. 42-03 - Rules On Assessment of National INternal Revenue Taxes Covered by A LN Under The Relief System PDFDocument12 pagesRMC No. 42-03 - Rules On Assessment of National INternal Revenue Taxes Covered by A LN Under The Relief System PDFCkey ArNo ratings yet

- 19524-1998 - Issuance of Permit To Print Sales InvoicesDocument1 page19524-1998 - Issuance of Permit To Print Sales InvoicesPhilAeonNo ratings yet

- 2307 Jan 2018 ENCS v3 BIRDocument2 pages2307 Jan 2018 ENCS v3 BIRlnbsanclementeNo ratings yet

- Pa Tax Brief - September 2018Document9 pagesPa Tax Brief - September 2018Teresita TibayanNo ratings yet

- Certificate of Creditable Tax Withheld at Source: Marfrancisco, Pinamalayan, Oriental MindoroDocument5 pagesCertificate of Creditable Tax Withheld at Source: Marfrancisco, Pinamalayan, Oriental MindoroChristcelda lozadaNo ratings yet

- G.R. No. 173854Document6 pagesG.R. No. 173854sofiaqueenNo ratings yet

- List of Assets (RMO 26-2010)Document6 pagesList of Assets (RMO 26-2010)d-fbuser-49417072No ratings yet

- RMO No. 34-2020Document1 pageRMO No. 34-2020Joel SyNo ratings yet

- Pilmico Vs CIRDocument9 pagesPilmico Vs CIRERNIL L BAWANo ratings yet

- Bir1600 July52019 - 2 PDFDocument2 pagesBir1600 July52019 - 2 PDFMaureen AlapaapNo ratings yet

- October 2020 Tax AlertDocument5 pagesOctober 2020 Tax AlertRheneir MoraNo ratings yet

- Finalisation Account Under GSTDocument20 pagesFinalisation Account Under GSTkbharathNo ratings yet

- G.R. No. 178090 Panasonic Vs CIRDocument4 pagesG.R. No. 178090 Panasonic Vs CIRRene ValentosNo ratings yet

- Ostrea Mineral - Yellow For FileDocument7 pagesOstrea Mineral - Yellow For FileJaime II LustadoNo ratings yet

- Factoring Charges Not Interest for TDSDocument3 pagesFactoring Charges Not Interest for TDSSaksham ShrivastavNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- Concept Note Sales Tax On ServicesDocument7 pagesConcept Note Sales Tax On ServicesAhmed RehanNo ratings yet

- Circular 4 2019Document7 pagesCircular 4 2019Kartik Santhanam IyerNo ratings yet

- Goods and Services Tax: Enter GSTIN/UIN of The TaxpayerDocument1 pageGoods and Services Tax: Enter GSTIN/UIN of The TaxpayerSandeepKumarJenaNo ratings yet

- MTF Tax Journal November 2021Document15 pagesMTF Tax Journal November 2021Christine Jane RodriguezNo ratings yet

- Domestic Sales Invoices for Oil and Gas Development Company Limited in May 2019Document1 pageDomestic Sales Invoices for Oil and Gas Development Company Limited in May 2019APNA VIP KASHMIRNo ratings yet

- Rmo 43-90 PDFDocument5 pagesRmo 43-90 PDFRieland Cuevas67% (3)

- Chief Collectorate Customs Quetta ObservationsDocument15 pagesChief Collectorate Customs Quetta ObservationsHamid AliNo ratings yet

- Accounts HeadDocument17 pagesAccounts Headrizashaan100% (1)

- General Financial RulesDocument220 pagesGeneral Financial RulesSaeed RasoolNo ratings yet

- 1.JIAP ObservationsDocument70 pages1.JIAP ObservationsHamid AliNo ratings yet

- Office of The Director General Audit, Inland Revenue & Customs (South)Document1 pageOffice of The Director General Audit, Inland Revenue & Customs (South)Hamid AliNo ratings yet

- AIR UAB West Wharf 2018-19Document7 pagesAIR UAB West Wharf 2018-19Hamid AliNo ratings yet

- Production of Record DG Valuation, Adj-I and Adj-IiDocument7 pagesProduction of Record DG Valuation, Adj-I and Adj-IiHamid AliNo ratings yet

- 16 05 19Document4 pages16 05 19Hamid AliNo ratings yet

- 16 05 19Document4 pages16 05 19Hamid AliNo ratings yet

- Revised Syllabus CE-2016 10 Jul 2015Document158 pagesRevised Syllabus CE-2016 10 Jul 2015Muhammad Faisal TahirNo ratings yet

- S 125Document317 pagesS 125ronaldosilva2100% (1)

- Hoisting and Rigging Plan ChecklistDocument5 pagesHoisting and Rigging Plan ChecklistRaja GuruNo ratings yet

- 92 - 96 Prelude Wiring DiagramsDocument19 pages92 - 96 Prelude Wiring Diagramssean112194% (31)

- Tel No: +603 7804 4036 47301 Petaling Jaya, Selangor, Malaysia. Fax No: +603 7804 4032Document1 pageTel No: +603 7804 4036 47301 Petaling Jaya, Selangor, Malaysia. Fax No: +603 7804 4032CAPT. MOHD KHAIRUL ANAM ILIASNo ratings yet

- Article PT3 ESSAY - Form 2 - Exam 2b (KELVIN)Document2 pagesArticle PT3 ESSAY - Form 2 - Exam 2b (KELVIN)Kelvin83% (6)

- Model Papers of AD SujectsDocument10 pagesModel Papers of AD SujectsOmar RashdiNo ratings yet

- Measuring Pavement Macrotexture Depth Using A Volumetric TechniqueDocument3 pagesMeasuring Pavement Macrotexture Depth Using A Volumetric Techniquedannychacon27No ratings yet

- Irc 34-2011 Recommendations For Road Construction in Areas Affected by Water Logging Flooding and Salts Infestation PDFDocument36 pagesIrc 34-2011 Recommendations For Road Construction in Areas Affected by Water Logging Flooding and Salts Infestation PDFਸੁਖਬੀਰ ਸਿੰਘ ਮਾਂਗਟ100% (5)

- Project On Steel Industry For OPMDocument18 pagesProject On Steel Industry For OPMsunilsony123No ratings yet

- EGR TuningbotDocument1 pageEGR TuningbotPablo NuñezNo ratings yet

- Amhara National Regional State Public Procurement and Property Disposal Service (Anrs PPPDS)Document20 pagesAmhara National Regional State Public Procurement and Property Disposal Service (Anrs PPPDS)Eyob LakewNo ratings yet

- Propulsion 2 QBDocument9 pagesPropulsion 2 QBu2b11517No ratings yet

- Ea 0002Document1 pageEa 0002fereetNo ratings yet

- CCE-TMS-300 Track Construction Requirements and TolerancesDocument58 pagesCCE-TMS-300 Track Construction Requirements and TolerancesSamuel Carlos Sanjuán TorresNo ratings yet

- Wa0035.Document17 pagesWa0035.Sama OdirNo ratings yet

- ITDP Presentation - C4C W5Document49 pagesITDP Presentation - C4C W5ITDP IndiaNo ratings yet

- PST Personal Survival Technique CourseDocument143 pagesPST Personal Survival Technique CourseAlhaj Massoud100% (1)

- Optical Transceiver Market2016 PDFDocument8 pagesOptical Transceiver Market2016 PDFjim1234u0% (1)

- Common Carrier Responsibility for Passengers After AlightingDocument2 pagesCommon Carrier Responsibility for Passengers After AlightingJose RolandNo ratings yet

- J&K introduces new rules for vehicle registrationDocument3 pagesJ&K introduces new rules for vehicle registrationHILAL AHMADNo ratings yet

- Pega Il 0310 TD VFC HoistDocument2 pagesPega Il 0310 TD VFC HoistsalesgglsNo ratings yet

- CJ4 FC MemItems REV1 Jun2018Document43 pagesCJ4 FC MemItems REV1 Jun2018brianNo ratings yet

- Thredbo MTB Trail Map 2023 24 Low ResDocument2 pagesThredbo MTB Trail Map 2023 24 Low Resunknown12862No ratings yet

- Asp Sealing Products LTD.: Pending Indent (Purchase Order) On Dated 05-JAN-2017 For "All" GroupDocument46 pagesAsp Sealing Products LTD.: Pending Indent (Purchase Order) On Dated 05-JAN-2017 For "All" GroupAnkit BinjolaNo ratings yet

- CV PelautDocument1 pageCV PelautWesly Rombo Botax100% (5)

- Ebook Lithium Battery GuidebookDocument29 pagesEbook Lithium Battery GuidebookMilind MohapatraNo ratings yet

- ManualDocument255 pagesManualblogeraryanNo ratings yet

- Bollard Pull Calculations - An Introduction (Part I)Document1 pageBollard Pull Calculations - An Introduction (Part I)Chanaka DilshanNo ratings yet

- EN 1358 751 101d 2017 05 OnlineDocument114 pagesEN 1358 751 101d 2017 05 Onlineemilio Alons83% (6)

- Association of American Railroads: Manual of Standards Recommended PracticesDocument20 pagesAssociation of American Railroads: Manual of Standards Recommended PracticesFabiano OliveiraNo ratings yet