You might also like

- Digital TransformationDocument22 pagesDigital TransformationJohn Ekpikhe100% (4)

- BSP Organizational StructureDocument1 pageBSP Organizational StructureJason MablesNo ratings yet

- Landbank vs Cacayuran Rulings on Locus Standi, Loan Validity and Ultra Vires ActsDocument14 pagesLandbank vs Cacayuran Rulings on Locus Standi, Loan Validity and Ultra Vires ActsPatatas SayoteNo ratings yet

- Financial Asset at Amortized CostDocument14 pagesFinancial Asset at Amortized CostLorenzo Diaz DipadNo ratings yet

- PWD BookDocument248 pagesPWD BookShahid Malik69% (13)

- Principles of Working Capital ManagementDocument45 pagesPrinciples of Working Capital ManagementSohini ChakrabortyNo ratings yet

- Sbi Car LoanDocument10 pagesSbi Car LoanShweta Yashwant Chalke100% (2)

- Rule 57 Cases (Originals)Document76 pagesRule 57 Cases (Originals)Anonymous Ig5kBjDmwQNo ratings yet

- Assignment - 2 The Role of Working Capital in Firm's LiquidityDocument11 pagesAssignment - 2 The Role of Working Capital in Firm's Liquidityparth limbachiyaNo ratings yet

- Wordsatello CorporationDocument6 pagesWordsatello Corporationcyrell015No ratings yet

- Descriptive AnalysisDocument61 pagesDescriptive AnalysisSrinivas NuluNo ratings yet

- Diego Alejandro Muñoz Codigo: 2260388 Preguntas en InglesDocument3 pagesDiego Alejandro Muñoz Codigo: 2260388 Preguntas en InglesDiego Alejandro Muñoz CuevasNo ratings yet

- Chapter Two Literature Review: I. Gross Concept II. Net ConceptDocument26 pagesChapter Two Literature Review: I. Gross Concept II. Net ConceptSachchithananthan ArikaranNo ratings yet

- JK Tecnology FileDocument75 pagesJK Tecnology FileAhmed JunaidNo ratings yet

- Fci Project SreeDocument94 pagesFci Project SreeLiju LawrenceNo ratings yet

- WCM SelfDocument17 pagesWCM Selfnitik chakmaNo ratings yet

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocument11 pages1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageNo ratings yet

- Cash Mang Ultra TechDocument5 pagesCash Mang Ultra TechSalkam PradeepNo ratings yet

- Working Capital ManagementDocument97 pagesWorking Capital ManagementravijillaNo ratings yet

- Importance of Working CapitalDocument4 pagesImportance of Working CapitalChaitanya DachepallyNo ratings yet

- Importance of Working Capital ManagementDocument2 pagesImportance of Working Capital Managementxxtha999No ratings yet

- Auiding FinishDocument51 pagesAuiding Finishdominic wurdaNo ratings yet

- The Importance of Working Capital ManagementDocument2 pagesThe Importance of Working Capital ManagementparthNo ratings yet

- New SaifDocument72 pagesNew SaifNasir RaineNo ratings yet

- Working Capital ManagmentDocument4 pagesWorking Capital ManagmentKundan kumarNo ratings yet

- Working Capital ManagementDocument19 pagesWorking Capital ManagementInes MiladiNo ratings yet

- Chapter - 1: 1.1 Cash ManagementDocument66 pagesChapter - 1: 1.1 Cash Managementgagana sNo ratings yet

- Gns 4 SuccessDocument10 pagesGns 4 SuccessOluwafemi ipinlayeNo ratings yet

- Unit 05Document98 pagesUnit 05Shah Maqsumul Masrur TanviNo ratings yet

- Chapter - 1: 1.1 Cash ManagementDocument9 pagesChapter - 1: 1.1 Cash Managementgagana sNo ratings yet

- Working Capital ManagementDocument9 pagesWorking Capital ManagementSahil PasrijaNo ratings yet

- ChapterDocument26 pagesChapterHeather NealNo ratings yet

- Literature ReviewDocument16 pagesLiterature Reviewধ্রুবজ্যোতি গোস্বামীNo ratings yet

- Operarting Cycle of A Company: MoneyDocument4 pagesOperarting Cycle of A Company: Money9987303726No ratings yet

- Last Report Yamaha MotorsDocument75 pagesLast Report Yamaha MotorsNasir RaineNo ratings yet

- Project On Working Capital ManagementDocument16 pagesProject On Working Capital ManagementVineeth VtNo ratings yet

- Docfinama2 Satello CorporationDocument6 pagesDocfinama2 Satello Corporationcyrell015No ratings yet

- Financial Management AssignementDocument14 pagesFinancial Management AssignementHARSHINI KudiaNo ratings yet

- New Edited Cash ManagementDocument59 pagesNew Edited Cash Managementdominic wurdaNo ratings yet

- WORKING CAPITAL MANAGEMENT: THE KEY TO CASH FLOWDocument15 pagesWORKING CAPITAL MANAGEMENT: THE KEY TO CASH FLOWSameer MunawarNo ratings yet

- Starting File YamahaDocument85 pagesStarting File YamahaAhmed JunaidNo ratings yet

- Wa0079.Document5 pagesWa0079.Walter tawanda MusosaNo ratings yet

- What Is Working Capital Management (WCM)Document26 pagesWhat Is Working Capital Management (WCM)Sudip BaruaNo ratings yet

- Study on Working Capital Management of Sarvottam Chemical LtdDocument60 pagesStudy on Working Capital Management of Sarvottam Chemical LtdjubinNo ratings yet

- Agricultural Financial Management BDocument25 pagesAgricultural Financial Management Bbryan rabonzaNo ratings yet

- Working Capital RatiosDocument28 pagesWorking Capital RatiosShubham JayaswalNo ratings yet

- New Microsoft Word DocumentDocument4 pagesNew Microsoft Word DocumentMasudRanaNo ratings yet

- Saif New ReportDocument95 pagesSaif New ReportNasir RaineNo ratings yet

- Working Capital Management by Birla GroupDocument39 pagesWorking Capital Management by Birla GroupHajra ShahNo ratings yet

- New Research 2017Document19 pagesNew Research 2017SAKSHI GUPTANo ratings yet

- Role of Banks in Working Capital ManagementDocument59 pagesRole of Banks in Working Capital Managementashwin thakurNo ratings yet

- Working CapitalDocument7 pagesWorking CapitalSreenath SreeNo ratings yet

- Part-6_Working-Capital-Management-and-Financial-ForecastingDocument76 pagesPart-6_Working-Capital-Management-and-Financial-ForecastingRicah Delos Reyes RubricoNo ratings yet

- Higher Return of CapitalDocument10 pagesHigher Return of CapitalShesha Nimna GamageNo ratings yet

- Business Finance CWDocument31 pagesBusiness Finance CWDenisho DeeNo ratings yet

- Working Capital ManagementDocument82 pagesWorking Capital ManagementAnacristina PincaNo ratings yet

- Cash ManagementDocument54 pagesCash Managementash aminNo ratings yet

- Sudhakar PVCDocument49 pagesSudhakar PVCAnusha ReddyNo ratings yet

- Business Finance IIDocument73 pagesBusiness Finance IIyakubu I saidNo ratings yet

- Working Capital Management Through Ratio AnalysisDocument87 pagesWorking Capital Management Through Ratio AnalysisDasari AnilkumarNo ratings yet

- Concept of Working Capital ManagementDocument3 pagesConcept of Working Capital Managementmonish147852No ratings yet

- Working Capital ManagementDocument7 pagesWorking Capital ManagementSwati KunwarNo ratings yet

- Synopsis 29.12.2022 - Amale Pradip GanpatDocument8 pagesSynopsis 29.12.2022 - Amale Pradip Ganpatarchana bagalNo ratings yet

- Why Is Financial Management So Important in BusinessDocument3 pagesWhy Is Financial Management So Important in BusinessReuben EscarlanNo ratings yet

- IntroductionDocument2 pagesIntroductionDinkar KumarNo ratings yet

- Year - Capacity Utilization (%)Document1 pageYear - Capacity Utilization (%)Shesha Nimna GamageNo ratings yet

- Higher Return of CapitalDocument10 pagesHigher Return of CapitalShesha Nimna GamageNo ratings yet

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocument11 pages1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageNo ratings yet

- 1.1. Importance of Working Capital ManagementDocument7 pages1.1. Importance of Working Capital ManagementShesha Nimna GamageNo ratings yet

- Higher Return of CapitalDocument10 pagesHigher Return of CapitalShesha Nimna GamageNo ratings yet

- Correct AnswersDocument2 pagesCorrect AnswersShesha Nimna GamageNo ratings yet

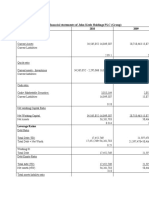

- Ratio Analysis On Financial Statements of John Keels Holdings PLC (Group)Document11 pagesRatio Analysis On Financial Statements of John Keels Holdings PLC (Group)Shesha Nimna GamageNo ratings yet

- Financial ManagementDocument1 pageFinancial ManagementShesha Nimna GamageNo ratings yet

- Year - Capacity Utilization (%)Document1 pageYear - Capacity Utilization (%)Shesha Nimna GamageNo ratings yet

- Question OneDocument16 pagesQuestion OneShesha Nimna GamageNo ratings yet

- Correct AnswersDocument2 pagesCorrect AnswersShesha Nimna GamageNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementShesha Nimna GamageNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementShesha Nimna GamageNo ratings yet

- WC PrinciplesDocument4 pagesWC PrinciplesShesha Nimna GamageNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementShesha Nimna GamageNo ratings yet

- AssetsDocument2 pagesAssetsShesha Nimna GamageNo ratings yet

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocument11 pages1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageNo ratings yet

- Profit Margin ComponentsDocument2 pagesProfit Margin ComponentsShesha Nimna GamageNo ratings yet

- 04Document10 pages04Shesha Nimna GamageNo ratings yet

- 1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapDocument11 pages1.1 The Importance of Working Capital Management Working Capitalit Is The Capital Used To Run The Day-To-Day Business Operations. Usually, The GapShesha Nimna GamageNo ratings yet

- Higher Return of CapitalDocument10 pagesHigher Return of CapitalShesha Nimna GamageNo ratings yet

- Higher Return of CapitalDocument10 pagesHigher Return of CapitalShesha Nimna GamageNo ratings yet

- Research IntroductionDocument3 pagesResearch IntroductionShesha Nimna GamageNo ratings yet

- CompereDocument1 pageCompereShesha Nimna GamageNo ratings yet

- Financial Audit Process: Terms of EngagementDocument1 pageFinancial Audit Process: Terms of EngagementShesha Nimna GamageNo ratings yet

- Annual Statistics 2018Document21 pagesAnnual Statistics 2018Shesha Nimna GamageNo ratings yet

- Blended Learning Desing For ACF 201Document2 pagesBlended Learning Desing For ACF 201Shesha Nimna GamageNo ratings yet

- Y BankDocument6 pagesY BankShesha Nimna GamageNo ratings yet

- Find The Value of XDocument1 pageFind The Value of XShesha Nimna GamageNo ratings yet

- TCQT ÔN TẬPDocument11 pagesTCQT ÔN TẬPPhước Đinh TriệuNo ratings yet

- MBA Specializations in Finance, HR, Marketing & ITDocument5 pagesMBA Specializations in Finance, HR, Marketing & ITVidhi ShahNo ratings yet

- Simple Finance Add On - v1Document409 pagesSimple Finance Add On - v1paridasg100% (1)

- A Message From The Secretary of The TreasuryDocument26 pagesA Message From The Secretary of The TreasurylosangelesNo ratings yet

- Daily Derivative Report 27 January 2016: NiftyDocument4 pagesDaily Derivative Report 27 January 2016: NiftyAyesha ShaikhNo ratings yet

- Marks.: (Semester & LncomeDocument8 pagesMarks.: (Semester & LncomeChetan MNo ratings yet

- Cash Management Cover LetterDocument9 pagesCash Management Cover Letterrqaeibifg100% (2)

- Letter To Premier Dwight Ball From David Vardy and Ron PenneyDocument3 pagesLetter To Premier Dwight Ball From David Vardy and Ron PenneyDesmond SullivanNo ratings yet

- Nature Description: PT Telekomunikasi Selular and Its Subsidiaries Trial Balance July 31, 2019Document102 pagesNature Description: PT Telekomunikasi Selular and Its Subsidiaries Trial Balance July 31, 2019Agniyyy TNo ratings yet

- Hilton CH 15 Select SolutionsDocument11 pagesHilton CH 15 Select SolutionsPiyushSharmaNo ratings yet

- The International ForecasterDocument44 pagesThe International Forecaster9roger95170No ratings yet

- Financing of Constructed FacilitiesDocument24 pagesFinancing of Constructed FacilitiesLyka TanNo ratings yet

- The Pizza Theory of Business ValuationDocument3 pagesThe Pizza Theory of Business ValuationBharat SahniNo ratings yet

- Service TaxDocument17 pagesService Taxvenky_1986100% (2)

- Chapter 4 - Post Merger ReorganisationDocument16 pagesChapter 4 - Post Merger ReorganisationAbhishek SinghNo ratings yet

- Book of Accounts: Prepared By: Marichu C. CarretasDocument62 pagesBook of Accounts: Prepared By: Marichu C. Carretaskiera hshaNo ratings yet

- Effects of RibaDocument1 pageEffects of RibaMimie LscNo ratings yet

- Business Combination: Consolidated Financial StatementsDocument9 pagesBusiness Combination: Consolidated Financial StatementsJuuzuu GearNo ratings yet

- Tata AigDocument4 pagesTata AigHarpal Singh MassanNo ratings yet

- Presentation Audit of Acquisition and Payment CycleDocument38 pagesPresentation Audit of Acquisition and Payment CycleSyaffiq UbaidillahNo ratings yet

- Week 4 Money Market and Inter Bank Call Loan by LCLEJARDEDocument24 pagesWeek 4 Money Market and Inter Bank Call Loan by LCLEJARDEErica CadagoNo ratings yet

- Bonus Loan FormDocument2 pagesBonus Loan FormPATCOMC CooperativeNo ratings yet

- Carandang vs. de GuzmanDocument14 pagesCarandang vs. de GuzmancharlougalaNo ratings yet