You might also like

- l04 Tax Planning StrategiesDocument4 pagesl04 Tax Planning Strategiesapi-408733519No ratings yet

- #6. Unholy Grails by Nick Radge, 2012 - 224 PGDocument1 page#6. Unholy Grails by Nick Radge, 2012 - 224 PGpatar greatNo ratings yet

- Po 3000033325Document2 pagesPo 3000033325Berlin GohNo ratings yet

- Cambridge Primary End of Series Report May 2021 - tcm142-627850Document80 pagesCambridge Primary End of Series Report May 2021 - tcm142-627850Shaimaa MuhammedNo ratings yet

- Regents Exams and Answers: Algebra II Revised EditionFrom EverandRegents Exams and Answers: Algebra II Revised EditionNo ratings yet

- 1-244909879656 G0093424359 PDFDocument9 pages1-244909879656 G0093424359 PDFSufian QayyumNo ratings yet

- Examiners Comments: Summer Exam - 2018Document12 pagesExaminers Comments: Summer Exam - 2018Fareha RiazNo ratings yet

- Examiners Comments: Summer Exam - 2018Document12 pagesExaminers Comments: Summer Exam - 2018Fareha RiazNo ratings yet

- 18554pcc Sugg Comments Nov09 gp1 PDFDocument4 pages18554pcc Sugg Comments Nov09 gp1 PDFGaurang AgarwalNo ratings yet

- CommentsW17 PDFDocument14 pagesCommentsW17 PDFFareha RiazNo ratings yet

- Caribbean Examinations Council: Report On Candidates' Work in The MAY/JUNE 2005Document7 pagesCaribbean Examinations Council: Report On Candidates' Work in The MAY/JUNE 2005Tavoy JamesNo ratings yet

- Summary of Head Examiners CommentsDocument5 pagesSummary of Head Examiners Commentsvijayant_1No ratings yet

- English As A Second Language (Speaking Endorsement)Document21 pagesEnglish As A Second Language (Speaking Endorsement)Saikit TamNo ratings yet

- Chinese As A Second Language: Paper 0523/01 Reading and WritingDocument6 pagesChinese As A Second Language: Paper 0523/01 Reading and WritingMaryam ShahidNo ratings yet

- November 2020 Examiner ReportDocument9 pagesNovember 2020 Examiner ReportXi WNo ratings yet

- English As A Second Language (Speaking Endorsement)Document21 pagesEnglish As A Second Language (Speaking Endorsement)Saikit TamNo ratings yet

- Examiners' Comment: Winter Exam - 2016Document14 pagesExaminers' Comment: Winter Exam - 2016Fareha RiazNo ratings yet

- Accounting Studies 2009 Assessment Report AnalysisDocument6 pagesAccounting Studies 2009 Assessment Report AnalysistoroahouseNo ratings yet

- Foreign Language Indonesian: Paper 0545/02 Reading and Directed Writing Key PointsDocument9 pagesForeign Language Indonesian: Paper 0545/02 Reading and Directed Writing Key PointsBrytistaNo ratings yet

- WAC01 - 01 - Pef - 20150305 (Accounting Edexcel IAL 2015 January Unit Examiner's Report)Document9 pagesWAC01 - 01 - Pef - 20150305 (Accounting Edexcel IAL 2015 January Unit Examiner's Report)James JoneNo ratings yet

- Corporate Secretaryship Examiners Report - Octoter 2011Document5 pagesCorporate Secretaryship Examiners Report - Octoter 2011imuranganwaNo ratings yet

- English As A Second Language (Speaking Endorsement)Document71 pagesEnglish As A Second Language (Speaking Endorsement)JohnIcebergNo ratings yet

- STEP 2 2019 Report, Hints, Mark SchemeDocument46 pagesSTEP 2 2019 Report, Hints, Mark SchemeJesse Drake100% (1)

- Examiners summarize key issues in candidates' exam performanceDocument7 pagesExaminers summarize key issues in candidates' exam performanceprashanthchakka4424No ratings yet

- English As A Second Language (Speaking Endorsement) : Paper 0510/11 Reading and Writing (Core) 11Document63 pagesEnglish As A Second Language (Speaking Endorsement) : Paper 0510/11 Reading and Writing (Core) 11Mohamed HussainNo ratings yet

- June 2018 Examiner ReportDocument69 pagesJune 2018 Examiner ReportaileelynnlamNo ratings yet

- Section 1Document7 pagesSection 1Khawaja SaifNo ratings yet

- English As A Second Language (Speaking Endorsement)Document26 pagesEnglish As A Second Language (Speaking Endorsement)Thinzar Tin winNo ratings yet

- Ministry of EducationDocument17 pagesMinistry of EducationShabnilMaharajNo ratings yet

- Bengali: Paper 3204/01 CompositionDocument4 pagesBengali: Paper 3204/01 Compositionmstudy123456No ratings yet

- Bengali: Paper 3204/01 CompositionDocument4 pagesBengali: Paper 3204/01 Compositionmstudy123456No ratings yet

- Examiners' Report/ Principal Examiner Feedback June 2011: International GCSE Spanish (4SP0) Paper 2Document8 pagesExaminers' Report/ Principal Examiner Feedback June 2011: International GCSE Spanish (4SP0) Paper 2EinsteinNo ratings yet

- Hindi: Paper 3195/01 CompositionDocument4 pagesHindi: Paper 3195/01 Compositionmstudy123456No ratings yet

- June 2021 Examiner ReportDocument30 pagesJune 2021 Examiner ReportPwintNo ratings yet

- Hindi: Section A - Letter, Report, Dialogue or SpeechDocument4 pagesHindi: Section A - Letter, Report, Dialogue or Speechmstudy123456No ratings yet

- Japanese (Foreign Language) : Section 1Document10 pagesJapanese (Foreign Language) : Section 1ぺレーラアヌクNo ratings yet

- 0549 m22 Er EnglishDocument7 pages0549 m22 Er Englishabdulhaadimotorwala34No ratings yet

- Examiner's Report: June 2014Document4 pagesExaminer's Report: June 2014ZhareenmNo ratings yet

- English As A Second Language (Speaking Endorsement)Document71 pagesEnglish As A Second Language (Speaking Endorsement)Kshitij SoniNo ratings yet

- Examiners Report 2016 - Updated 31-01-2017Document8 pagesExaminers Report 2016 - Updated 31-01-2017Saad Ahsan0% (1)

- FEDERAL EXAMINER REPORTSDocument49 pagesFEDERAL EXAMINER REPORTShome143No ratings yet

- ChineseDocument10 pagesChinesejanicechuNo ratings yet

- Business Management Behavioural StudiesDocument5 pagesBusiness Management Behavioural StudiesMohayman AbdullahNo ratings yet

- Business StudiesDocument9 pagesBusiness StudiesWonder Bee NzamaNo ratings yet

- November 2020 Examiner ReportDocument31 pagesNovember 2020 Examiner ReportXi WNo ratings yet

- Bengali: Paper 3204/01 CompositionDocument6 pagesBengali: Paper 3204/01 CompositionAhmed NaserNo ratings yet

- Grade 7 English p2 2022Document8 pagesGrade 7 English p2 2022Kudakwashe MusvaireNo ratings yet

- Chinese As A Second LanguageDocument6 pagesChinese As A Second LanguageMaryam ShahidNo ratings yet

- 2019 May Cambridge Primary Checkpoint End of Series Report May 2019 - tcm142-546983Document149 pages2019 May Cambridge Primary Checkpoint End of Series Report May 2019 - tcm142-546983Hildebrando GiraldoNo ratings yet

- Indvl and Soc Subject Report 2019Document9 pagesIndvl and Soc Subject Report 2019RITA CHANDRANNo ratings yet

- Hindi: Paper 3195/01 CompositionDocument3 pagesHindi: Paper 3195/01 Compositionmstudy123456No ratings yet

- Corporate Financial Management Examiners Report October 2012Document4 pagesCorporate Financial Management Examiners Report October 2012imuranganwaNo ratings yet

- Chinese As A Second LanguageDocument8 pagesChinese As A Second LanguageMaryam ShahidNo ratings yet

- P4 Exam Report June 2011Document4 pagesP4 Exam Report June 2011Duc Anh NguyenNo ratings yet

- English As Second Language StudiesDocument5 pagesEnglish As Second Language Studiesdchan_26No ratings yet

- P5 Examiners' report on Dec 2007 examDocument2 pagesP5 Examiners' report on Dec 2007 exammconquerer8196No ratings yet

- Pakistan StudiesDocument6 pagesPakistan StudiesMubashra AhmadNo ratings yet

- Cambridge Primary End of Series Report May 2023 - tcm142-687678Document87 pagesCambridge Primary End of Series Report May 2023 - tcm142-687678Nigar RasulzadaNo ratings yet

- 1123 - s19 - Examiner's ReportDocument23 pages1123 - s19 - Examiner's ReportAden FatimaNo ratings yet

- 21) Dec 2005 - ERDocument2 pages21) Dec 2005 - ERNgo Sy VinhNo ratings yet

- STEP 2 - Examiners Report - Hints & Solutions - Mark Schemes 2018Document62 pagesSTEP 2 - Examiners Report - Hints & Solutions - Mark Schemes 2018tony dooNo ratings yet

- Pakistan Institute of Public Finance Accountants: Winter Exam-2019Document3 pagesPakistan Institute of Public Finance Accountants: Winter Exam-2019IbrahimGorgageNo ratings yet

- Pak Affair.Document3 pagesPak Affair.IbrahimGorgageNo ratings yet

- Medical Attendance Rules 2005 - 1Document6 pagesMedical Attendance Rules 2005 - 1IbrahimGorgageNo ratings yet

- Medical Attendance Rulea 2005..Document6 pagesMedical Attendance Rulea 2005..IbrahimGorgageNo ratings yet

- Pakistan Institute of Public Finance Accountants: Winter Exam-2019Document3 pagesPakistan Institute of Public Finance Accountants: Winter Exam-2019IbrahimGorgageNo ratings yet

- Pakistan Institute of Public Finance Accountants: Winter Exam-2019Document3 pagesPakistan Institute of Public Finance Accountants: Winter Exam-2019IbrahimGorgageNo ratings yet

- Implementation of NPIs 6 NovDocument1 pageImplementation of NPIs 6 NovIbrahimGorgageNo ratings yet

- Sec-008 - Damp Proof Course & Water ProofingDocument4 pagesSec-008 - Damp Proof Course & Water ProofingIbrahimGorgageNo ratings yet

- New Doc 2020-08-21 - 1Document1 pageNew Doc 2020-08-21 - 1IbrahimGorgageNo ratings yet

- Cash Award JudgmentDocument8 pagesCash Award JudgmentIbrahimGorgageNo ratings yet

- 2019 PolicyDocument3 pages2019 PolicyIbrahimGorgageNo ratings yet

- Statistical Officer Research Officer English MCQs September 2020Document2 pagesStatistical Officer Research Officer English MCQs September 2020IbrahimGorgageNo ratings yet

- Signature & Seal of The Head of Office Signature & Seal of The Head of DepartmentDocument4 pagesSignature & Seal of The Head of Office Signature & Seal of The Head of DepartmentIbrahimGorgageNo ratings yet

- Public Works 7Document12 pagesPublic Works 7IbrahimGorgageNo ratings yet

- Notice of Public Sector Classes Sept2020Document1 pageNotice of Public Sector Classes Sept2020IbrahimGorgageNo ratings yet

- Misoprostol For Treatment of Early Pregnancy LossDocument2 pagesMisoprostol For Treatment of Early Pregnancy LossJuan KipronoNo ratings yet

- Pakistan Institute of Public Finance Accoutants: Schedule Winter Exam-2020Document2 pagesPakistan Institute of Public Finance Accoutants: Schedule Winter Exam-2020IbrahimGorgageNo ratings yet

- Statistical Officer Research Officer English MCQs September 2020Document2 pagesStatistical Officer Research Officer English MCQs September 2020IbrahimGorgageNo ratings yet

- HC Jobs 2020Document1 pageHC Jobs 2020IbrahimGorgageNo ratings yet

- Application Form: Post Applied ForDocument2 pagesApplication Form: Post Applied ForIbrahimGorgageNo ratings yet

- B.A. Private Annual 2020 Objection ListDocument15 pagesB.A. Private Annual 2020 Objection ListIbrahimGorgageNo ratings yet

- BPSC AddressDocument1 pageBPSC AddressIbrahimGorgageNo ratings yet

- The Balochistan Government Employees Benevolent Fund Act, 2018 Act No. XV of 2018Document5 pagesThe Balochistan Government Employees Benevolent Fund Act, 2018 Act No. XV of 2018M A Khan FarazNo ratings yet

- Combined Ad No 01-2020Document9 pagesCombined Ad No 01-2020Ameer Hamza CheemaNo ratings yet

- HC Jobs 2020Document1 pageHC Jobs 2020IbrahimGorgageNo ratings yet

- FPSC AddressDocument1 pageFPSC AddressIbrahimGorgageNo ratings yet

- HC Jobs 2020Document1 pageHC Jobs 2020IbrahimGorgageNo ratings yet

- Statistical Officer Research Officer English MCQs September 2020Document2 pagesStatistical Officer Research Officer English MCQs September 2020IbrahimGorgageNo ratings yet

- Government Jobs in BalochistanDocument5 pagesGovernment Jobs in BalochistanIbrahimGorgageNo ratings yet

- Nil TFDocument3 pagesNil TFlachimolala. kookieee97No ratings yet

- Maximum Volume: Annual Report & AccountsDocument104 pagesMaximum Volume: Annual Report & Accountslodhi12No ratings yet

- Can India Afford To Boycott Chinese ProductsDocument2 pagesCan India Afford To Boycott Chinese ProductsSowmya MinnuNo ratings yet

- Garcia vs. Court of AppealsDocument12 pagesGarcia vs. Court of AppealsJoannah SalamatNo ratings yet

- Internship CertificateDocument19 pagesInternship CertificatesaiNo ratings yet

- Assurance Wireless ApplicationDocument2 pagesAssurance Wireless ApplicationMichelle KajikawaNo ratings yet

- Essentials of a Valid Contract of SaleDocument78 pagesEssentials of a Valid Contract of Salenitesh kumar satsangiNo ratings yet

- Task 7: Sreejith E M Jr. Research Analyst Intern 22FMCG30B15Document23 pagesTask 7: Sreejith E M Jr. Research Analyst Intern 22FMCG30B15Sreejitha EmNo ratings yet

- Consolidated Intercompany TransactionsDocument73 pagesConsolidated Intercompany TransactionsFatima AL-Sayed100% (1)

- Study Guide Topic A: European CouncilDocument9 pagesStudy Guide Topic A: European CouncilAaqib ChaturbhaiNo ratings yet

- Credit AppraisalDocument11 pagesCredit AppraisalKunal GoelNo ratings yet

- OCWchapter 7Document22 pagesOCWchapter 7Charmine agbonNo ratings yet

- Btec HND in Business (Finance) : Assignment Cover SheetDocument27 pagesBtec HND in Business (Finance) : Assignment Cover SheetViệt PhongNo ratings yet

- "Centralni Hali" Case:: Background Information For The Creation of Anti-Corruption Guide For The Municipal AdministrationDocument4 pages"Centralni Hali" Case:: Background Information For The Creation of Anti-Corruption Guide For The Municipal AdministrationPetrus van DuyneNo ratings yet

- Role and Functions of RBI: HistoryDocument9 pagesRole and Functions of RBI: HistorydimpledeepaNo ratings yet

- Slides Set3Document116 pagesSlides Set3Vaishnavi GnanasekaranNo ratings yet

- Jiban Bima CorporationDocument88 pagesJiban Bima CorporationPromiti SarkerNo ratings yet

- Module 8 Blm1 Week 7Document23 pagesModule 8 Blm1 Week 7sheinamae quelnatNo ratings yet

- ICICI Case StudyDocument11 pagesICICI Case StudyRavee Mishra0% (1)

- Hospitality Industry and Lodging or Real EstateDocument17 pagesHospitality Industry and Lodging or Real EstateRommel VinluanNo ratings yet

- Invoice 614918Document1 pageInvoice 614918Santiago SánchezNo ratings yet

- Internship Report On Allied Bank of PakistanDocument86 pagesInternship Report On Allied Bank of Pakistanshrewd_tycoon94% (17)

- Answer KeyDocument9 pagesAnswer KeyDeepakshiNo ratings yet

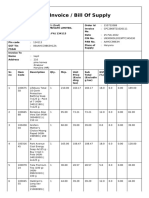

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- Pepsi Killing SoftlyDocument32 pagesPepsi Killing SoftlyVamsi ReddyNo ratings yet

- Document WPS OfficeDocument1 pageDocument WPS OfficeSayan DasNo ratings yet