You might also like

- James Traficant - Testimony RE: US Bankruptcy 1993Document4 pagesJames Traficant - Testimony RE: US Bankruptcy 1993Ven Geancia100% (1)

- Regulation of Financial Markets Take Home ExamDocument22 pagesRegulation of Financial Markets Take Home ExamBrandon TeeNo ratings yet

- Checking Account StatementDocument2 pagesChecking Account StatementjohanNo ratings yet

- CPWD - BBP - Finance and Accounts - V1.0 PDFDocument68 pagesCPWD - BBP - Finance and Accounts - V1.0 PDFAbhay KumarNo ratings yet

- Strategic Management PaperDocument97 pagesStrategic Management PaperElle Woods100% (3)

- Competitive Profile Matrix (CPM)Document8 pagesCompetitive Profile Matrix (CPM)Akhil Mehta0% (1)

- Final StramaDocument74 pagesFinal StramaRalphDesiEscueta94% (36)

- MBL Limit 75K: COMPANY XY Strategic Management PaperDocument137 pagesMBL Limit 75K: COMPANY XY Strategic Management PaperStef Tanhueco100% (1)

- Ayala Land's Strategic Management AnalysisDocument161 pagesAyala Land's Strategic Management Analysisjohn marco faustNo ratings yet

- #BWNLLSV #000000P5U1TYY0A5#000JML90F Urijah K Keshka 1658 Larkspur LN BEAUMONT CA 92223-2085Document5 pages#BWNLLSV #000000P5U1TYY0A5#000JML90F Urijah K Keshka 1658 Larkspur LN BEAUMONT CA 92223-2085andy100% (3)

- Filinvest Land's Strategic ManagementDocument69 pagesFilinvest Land's Strategic ManagementChristian PerezNo ratings yet

- Dlsu PaperDocument245 pagesDlsu Papersdfkshfdsfh75% (4)

- STRAMA Shellyn E Gomez Revised PDFDocument243 pagesSTRAMA Shellyn E Gomez Revised PDFAilene Quinto100% (1)

- Strategic Management Plan (Bpi)Document93 pagesStrategic Management Plan (Bpi)Sido Angel Mae BarbonNo ratings yet

- STRAMADocument58 pagesSTRAMAKaithe Wenceslao100% (4)

- Strama 2015Document72 pagesStrama 2015Millicent Matienzo100% (5)

- Barkin' Blends Dog Café Success StoryDocument18 pagesBarkin' Blends Dog Café Success StoryZia Irra Alegre0% (1)

- Soriano vs. People and BSP GR NO. 162336, FEB. 1, 2010Document2 pagesSoriano vs. People and BSP GR NO. 162336, FEB. 1, 2010Julio100% (1)

- Strategic Management Paper of ABC Insurance CorporationDocument180 pagesStrategic Management Paper of ABC Insurance CorporationPROF. ERWIN M. GLOBIO, MSIT80% (20)

- Strategic Management Paper of ABC Insurance Corporation PDFDocument180 pagesStrategic Management Paper of ABC Insurance Corporation PDFRex dela CruzNo ratings yet

- Boost Bibingkinitan's Brand RecognitionDocument83 pagesBoost Bibingkinitan's Brand RecognitionEnsot Soriano100% (1)

- DMCI Homes Strategic Management PaperDocument207 pagesDMCI Homes Strategic Management PaperPio CampolivasNo ratings yet

- BTEC HND in Management/Marketing/Human Resource Strategic PlanningDocument13 pagesBTEC HND in Management/Marketing/Human Resource Strategic PlanningArmie SalcedoNo ratings yet

- Strategic Management Sample Research Paper PDFDocument14 pagesStrategic Management Sample Research Paper PDFMohammed Abu Salah100% (6)

- Chapter 1: Introduction: A. Company BackgroundDocument30 pagesChapter 1: Introduction: A. Company Backgroundwangyu roqueNo ratings yet

- STRAMA Dont Like You She Likes Evreryone.. 1Document128 pagesSTRAMA Dont Like You She Likes Evreryone.. 1Jasper MonteroNo ratings yet

- ORGANIZATIONAL CHART AND MARKET POSITION ANALYSISDocument9 pagesORGANIZATIONAL CHART AND MARKET POSITION ANALYSISjancat_06100% (2)

- SAMPLE Nissan Westgate Strama PaperDocument92 pagesSAMPLE Nissan Westgate Strama Papermariadaniellecuyson100% (1)

- Summary SmartDocument2 pagesSummary SmartGerra Lanuza0% (1)

- Final StramaDocument75 pagesFinal StramaChristian Jay Patiño Orpano100% (1)

- Jollibee Food Corporation Strategic Management PlanDocument99 pagesJollibee Food Corporation Strategic Management Planmichelle angela maramag100% (3)

- METROBANK STRATEGIC PLANNING AND MANAGEMENTDocument28 pagesMETROBANK STRATEGIC PLANNING AND MANAGEMENTAnderei Acantilado67% (9)

- Strama Paper FINALCOPY 1-10Document136 pagesStrama Paper FINALCOPY 1-10Aira Dela Cruz100% (1)

- San Miguel Corporation Annual Report and Financial StatementsDocument360 pagesSan Miguel Corporation Annual Report and Financial StatementsCharmaine Magdangal50% (2)

- CHAPTER I To IV StramaDocument76 pagesCHAPTER I To IV StramaIra Matienzo100% (2)

- PLDT CASE STUDY: Organizational Culture and Employee BehaviorDocument15 pagesPLDT CASE STUDY: Organizational Culture and Employee BehaviorAisah ReemNo ratings yet

- S120030 Sychingping Kenneth Strama Final Revised Security Bank PDFDocument197 pagesS120030 Sychingping Kenneth Strama Final Revised Security Bank PDFJacq Phoebe100% (1)

- METROBANKDocument28 pagesMETROBANKMa Teresa Angelyn100% (5)

- Metrobank - AnalysisDocument28 pagesMetrobank - AnalysisMeditacio Monto89% (27)

- BDO Unibank Philippines largest bankDocument7 pagesBDO Unibank Philippines largest bankJana Kryzl DibdibNo ratings yet

- Strategic Management Paper On PuregoldDocument86 pagesStrategic Management Paper On PuregoldRaraj61% (28)

- Comparative Analysis of Mutual Fund of HDFC ICICIDocument33 pagesComparative Analysis of Mutual Fund of HDFC ICICIAniket Ramteke100% (1)

- BPI/MS Strategic Management PlanDocument76 pagesBPI/MS Strategic Management PlanRochwell MercadoNo ratings yet

- Far Eastern University - Makati: Institute of Accounts, Business & FinanceDocument35 pagesFar Eastern University - Makati: Institute of Accounts, Business & FinanceJanriggs Rodriguez100% (1)

- A Strategic Management Paper on Savemore's Growth StrategyDocument32 pagesA Strategic Management Paper on Savemore's Growth Strategyangelica100% (2)

- Puregold Price Club Inc. Case StudyDocument22 pagesPuregold Price Club Inc. Case StudyREGIE ANN CATILOCNo ratings yet

- Metrobank Case StudyDocument22 pagesMetrobank Case StudySharmaine R. Oribiana100% (1)

- Strama Okay Na QSPMDocument74 pagesStrama Okay Na QSPMBianca VillaNo ratings yet

- Bank of The Philippine IslandsDocument5 pagesBank of The Philippine IslandsCaryl Almira SayreNo ratings yet

- METROBANK STRATEGIC PLANNINGDocument28 pagesMETROBANK STRATEGIC PLANNINGsheila mae adayaNo ratings yet

- Bpi Bdo MetrobankDocument33 pagesBpi Bdo MetrobankMikio Norberte100% (1)

- Strama Paper Efa - SampleDocument16 pagesStrama Paper Efa - SampleSheilaMarieAnnMagcalasNo ratings yet

- CC StramaDocument40 pagesCC Stramaamcagirl100% (2)

- STRAMA Table of ContentsDocument7 pagesSTRAMA Table of ContentsKareen RanteNo ratings yet

- StramaCaseNo 2 PDFDocument13 pagesStramaCaseNo 2 PDFRufino Gerard Moreno100% (2)

- Strategic Management PaperDocument35 pagesStrategic Management PaperAlexyss Alip100% (1)

- STRAMADocument4 pagesSTRAMACarl MoliculesNo ratings yet

- Danica StramaDocument5 pagesDanica StramaDanica GabuatNo ratings yet

- GROUP1 UmajiDocument11 pagesGROUP1 UmajiKevin Matibag100% (3)

- CenturyDocument35 pagesCenturyKathy V. Chua-Grimme0% (2)

- SM MegamallsDocument6 pagesSM Megamallsjona empalNo ratings yet

- BDO Business StudyDocument14 pagesBDO Business StudyPhaul QuicktrackNo ratings yet

- Acdi OutputDocument8 pagesAcdi OutputVj Lentejas IIINo ratings yet

- (PNB) Company BackgroundDocument1 page(PNB) Company BackgroundAlbert Ocno Almine100% (2)

- Final Strama PaperDocument68 pagesFinal Strama Paperthrezce_1350% (2)

- DocstestingnielDocument67 pagesDocstestingnielelrosimo100% (2)

- Bank of The Philippine IslandDocument5 pagesBank of The Philippine IslandAdeline Mangulad MontebonNo ratings yet

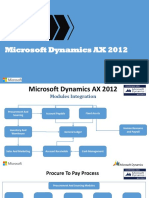

- Modules InterConDocument9 pagesModules InterConAmith PrasannaNo ratings yet

- CV of Mohd. Sariful Islam (Cashier)Document3 pagesCV of Mohd. Sariful Islam (Cashier)Sariful IslamNo ratings yet

- Personocratia Money.Document1 pagePersonocratia Money.negreibsNo ratings yet

- Part I-Introduction (Financial Market)Document56 pagesPart I-Introduction (Financial Market)Steve Jhon James TantingNo ratings yet

- Claravall vs. CADocument8 pagesClaravall vs. CAAnonymous oDPxEkdNo ratings yet

- R Gordon RichardDocument8 pagesR Gordon RichardCalWonkNo ratings yet

- Study Guide For Credit Life Disability InsuranceDocument204 pagesStudy Guide For Credit Life Disability InsuranceBounna PhoumalavongNo ratings yet

- IPL ReviewerDocument5 pagesIPL ReviewerPrincessNo ratings yet

- Big Data For Retail BankingDocument9 pagesBig Data For Retail BankingSaratNo ratings yet

- USAID Mission Closure ChecklistsDocument41 pagesUSAID Mission Closure Checklistswedaje2003No ratings yet

- NEW GOVT ACCOUNTING SYSTEM MANUALDocument12 pagesNEW GOVT ACCOUNTING SYSTEM MANUALCarlota Nicolas VillaromanNo ratings yet

- Aea HIVEpv TOjad WDocument14 pagesAea HIVEpv TOjad WAadarshNo ratings yet

- Annu Singhal: Professional ObjectiveDocument2 pagesAnnu Singhal: Professional ObjectiveKumaravel JaganathanNo ratings yet

- Soal Penyisihan SMK Oan2017 PDFDocument31 pagesSoal Penyisihan SMK Oan2017 PDFnuria amaliaNo ratings yet

- Annex A. LTG FS 2013. NarraCapital FS 2012&2013 PDFDocument331 pagesAnnex A. LTG FS 2013. NarraCapital FS 2012&2013 PDFJohn Alfer Bag-oNo ratings yet

- Advertisement and Promotion Strategy of Jamuna Bank Ltd.Document60 pagesAdvertisement and Promotion Strategy of Jamuna Bank Ltd.SAEID RAHMANNo ratings yet

- Lit Rview Credit AppraisalDocument4 pagesLit Rview Credit AppraisalHari KrishnanNo ratings yet

- Supertech ORBDocument9 pagesSupertech ORBGreen Realtech Projects Pvt LtdNo ratings yet

- Digital InitiativeDocument215 pagesDigital Initiativehema mishraNo ratings yet

- Indiapost Blue Book FinalDocument135 pagesIndiapost Blue Book Finalজ্যোতিৰ্ময় বসুমতাৰীNo ratings yet

- Cross Rates - November 12 2019Document1 pageCross Rates - November 12 2019Lisle Daverin BlythNo ratings yet

- Gmail - Your Booking Confirmation PDFDocument8 pagesGmail - Your Booking Confirmation PDFvillanuevamarkdNo ratings yet

- CSCI262 Trustedcomputing 1+2Document86 pagesCSCI262 Trustedcomputing 1+2ami_haroonNo ratings yet