You might also like

- Aqua Bounty - Case AnswersDocument6 pagesAqua Bounty - Case AnswersAblorh Mensah Abraham50% (4)

- The Toyota Kata Practice Guide: Practicing Scientific Thinking Skills for Superior Results in 20 Minutes a DayFrom EverandThe Toyota Kata Practice Guide: Practicing Scientific Thinking Skills for Superior Results in 20 Minutes a DayRating: 4.5 out of 5 stars4.5/5 (7)

- On July 1 2014 Melanie Thornhill Began Her Third MonthDocument1 pageOn July 1 2014 Melanie Thornhill Began Her Third MonthTaimour HassanNo ratings yet

- Format of Final Accounts ACC 415 UITMDocument2 pagesFormat of Final Accounts ACC 415 UITMAifaa ArinaNo ratings yet

- Chapter 2 Test BankDocument29 pagesChapter 2 Test BankMhmdd Nour AlameddineNo ratings yet

- Progress Driven Spun Pile CombineDocument3 pagesProgress Driven Spun Pile CombineRyanNo ratings yet

- Allama Iqbal Open University, Islamabad: (Department of CommerceDocument4 pagesAllama Iqbal Open University, Islamabad: (Department of Commerceilyas muhammadNo ratings yet

- PPMC November 2023-WorkbookDocument40 pagesPPMC November 2023-Workbookanil sharmaNo ratings yet

- Business DashboardDocument47 pagesBusiness DashboardRalph BeranaNo ratings yet

- Practice Sums - Sessions - 3-4Document58 pagesPractice Sums - Sessions - 3-4Vibhuti AnandNo ratings yet

- ChartDocument1 pageChartSaiVamsiNo ratings yet

- Straight Razor RulerDocument1 pageStraight Razor RulerEdson GordianoNo ratings yet

- KING FOR A DAY INTERACTIVE TAB by Faith No More @Document5 pagesKING FOR A DAY INTERACTIVE TAB by Faith No More @Carol CostaNo ratings yet

- HTEW WorkbookDocument22 pagesHTEW Workbookmarofav559No ratings yet

- Grid PadDocument1 pageGrid PadFREDNo ratings yet

- Prepositio N KalimatDocument36 pagesPrepositio N Kalimatkiki sNo ratings yet

- Business Plan WorkbookDocument15 pagesBusiness Plan WorkbookDarkchild HeavensNo ratings yet

- Year Fed Min Wage Min Wage Relative To 1970 CPI Wage/CPIDocument5 pagesYear Fed Min Wage Min Wage Relative To 1970 CPI Wage/CPIJohnny AppleseedNo ratings yet

- Zo Ledger 2013Document27 pagesZo Ledger 2013saif RashidNo ratings yet

- Summary of Or's For SHSVPDocument2 pagesSummary of Or's For SHSVPolophs piatNo ratings yet

- Business Plan WorkbookDocument15 pagesBusiness Plan WorkbookvangheliexNo ratings yet

- Mag 201807 06 mfaEGYDocument2 pagesMag 201807 06 mfaEGYBookratNo ratings yet

- Brooklyn Community District 9: Total PopulationDocument40 pagesBrooklyn Community District 9: Total PopulationcouncilkNo ratings yet

- Attendance List: NO Name Unit/Department TTDDocument1 pageAttendance List: NO Name Unit/Department TTDwaka holdingNo ratings yet

- DAMATH BoardDocument4 pagesDAMATH BoardJoan DalilisNo ratings yet

- Licks (Diminished Scale)Document1 pageLicks (Diminished Scale)MarioNo ratings yet

- The Australian Economy and Financial Markets: July 2019Document33 pagesThe Australian Economy and Financial Markets: July 2019Amita SinghNo ratings yet

- Mortgage Rates JuneDocument6 pagesMortgage Rates JuneChris CoNo ratings yet

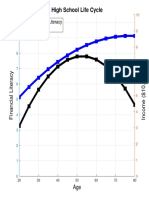

- High School Life Cycle: Financial Literacy IncomeDocument1 pageHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsNo ratings yet

- Date Cemexcpo IpycDocument25 pagesDate Cemexcpo IpycthalibritNo ratings yet

- SopranosDocument1 pageSopranosFernando DíazNo ratings yet

- Graphing Coordinate PlaneDocument1 pageGraphing Coordinate PlaneDonovan KwanNo ratings yet

- Cartesian Plane Print Out ForDocument1 pageCartesian Plane Print Out Forn82fthrmy4No ratings yet

- Fender InsDocument4 pagesFender InsRyszardaNo ratings yet

- SD0131000 CPG 1Document1 pageSD0131000 CPG 1dolhofNo ratings yet

- 5 Minute Practice PDFDocument1 page5 Minute Practice PDFNebojša JoksimovićNo ratings yet

- 5 Minute Practice PDFDocument1 page5 Minute Practice PDFNebojša JoksimovićNo ratings yet

- 5 Minute Practice PDFDocument1 page5 Minute Practice PDFNebojša JoksimovićNo ratings yet

- 5 Minute Practice: Standard TuningDocument1 page5 Minute Practice: Standard TuningHéctor Sanmanuel TorresNo ratings yet

- 5 Minute Practice PDFDocument1 page5 Minute Practice PDFNebojša JoksimovićNo ratings yet

- Set of Four Quadrant Graph PaperDocument1 pageSet of Four Quadrant Graph PaperCardin PatrickNo ratings yet

- Angèle - Balance Ton Quoi (Guitar 1)Document1 pageAngèle - Balance Ton Quoi (Guitar 1)Leander LyonsNo ratings yet

- SLASH Warm Up ExerciseDocument1 pageSLASH Warm Up ExerciseIncredible MaxNo ratings yet

- SLASH Warm Up Exercise PDFDocument1 pageSLASH Warm Up Exercise PDFRonaldo OrtizNo ratings yet

- School Oral Health Examination Card: Name of Pupil: Grade/ Section: Guide Questions Y NDocument4 pagesSchool Oral Health Examination Card: Name of Pupil: Grade/ Section: Guide Questions Y Nrene conaNo ratings yet

- Final Porfolio PaperDocument15 pagesFinal Porfolio PaperDeep DualNo ratings yet

- Jadwal Lebaran 22,23 April 2023Document4 pagesJadwal Lebaran 22,23 April 2023Choirul AnwarNo ratings yet

- Cbe 2016 - 17Document147 pagesCbe 2016 - 17Abate GashawNo ratings yet

- Como Criar Frases CromáticasDocument2 pagesComo Criar Frases CromáticasMoisesNo ratings yet

- Academic Monitoring Report: M F T M F T M F T M F T M F T M F TDocument1 pageAcademic Monitoring Report: M F T M F T M F T M F T M F T M F TYanna HyunNo ratings yet

- 2021 12 MSCI SouthAfrica Annual Property Index UnfrozenDocument3 pages2021 12 MSCI SouthAfrica Annual Property Index UnfrozenAlister HumanNo ratings yet

- Dalily Plan SheetDocument1 pageDalily Plan Sheet5hubhiNo ratings yet

- BVM - Presentation - J P Morgan - Jan. 2011Document65 pagesBVM - Presentation - J P Morgan - Jan. 2011Saurabh Kumar KarnNo ratings yet

- Al Adiyat - Al ZalzalahDocument1 pageAl Adiyat - Al Zalzalahlubis -No ratings yet

- Padrao 1 Padrao 2 Padrao 3: Standard TuningDocument1 pagePadrao 1 Padrao 2 Padrao 3: Standard TuningGabriel de AndradeNo ratings yet

- Musical (5 e 10 Minutos) : Exercicio 4 (Diagonal Com Saltos) Kiko Loureiro Guitar WorkoutDocument1 pageMusical (5 e 10 Minutos) : Exercicio 4 (Diagonal Com Saltos) Kiko Loureiro Guitar WorkoutArthur MonteiroNo ratings yet

- Autumn Leaves: Freely 110Document2 pagesAutumn Leaves: Freely 110Andreson SouzaNo ratings yet

- Autumn LeavesDocument2 pagesAutumn LeavesChristianNo ratings yet

- Boiler EquationsDocument155 pagesBoiler Equationspulakjaiswal85No ratings yet

- En Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSDocument2 pagesEn Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSsantiyrhNo ratings yet

- 2019 EventDocument11 pages2019 EventTanu GoyalNo ratings yet

- Análise PEST TemplateDocument2 pagesAnálise PEST TemplateAlef Luiz Camargo EsperandioNo ratings yet

- Bad Intent (Solo) - Frank Gambale - Concert With ClassDocument6 pagesBad Intent (Solo) - Frank Gambale - Concert With ClassKurtis LeCompteNo ratings yet

- A. Natural System: Terms and Definitions: 1. Type of SystemsDocument10 pagesA. Natural System: Terms and Definitions: 1. Type of SystemsMajane TognoNo ratings yet

- A. Statement of Financial Position (Balance Sheet)Document5 pagesA. Statement of Financial Position (Balance Sheet)Majane TognoNo ratings yet

- RRL TaxDocument6 pagesRRL TaxMajane TognoNo ratings yet

- RRL FinalDocument5 pagesRRL FinalMajane TognoNo ratings yet

- Management Advisory Services Test Banks 2Document37 pagesManagement Advisory Services Test Banks 2Majane TognoNo ratings yet

- Choco LitDocument1 pageChoco LitMajane TognoNo ratings yet

- What Is Talent Management?Document3 pagesWhat Is Talent Management?KataNo ratings yet

- P5 Syl2012 InterDocument12 pagesP5 Syl2012 InterVimal ShuklaNo ratings yet

- Literature ReviewDocument2 pagesLiterature ReviewSatish Nagireddy50% (4)

- Proforma Mahindra TeqoDocument1 pageProforma Mahindra Teqop m yadavNo ratings yet

- HLB Receipt-2023-01-13Document1 pageHLB Receipt-2023-01-13Nur NabilaNo ratings yet

- China Pakistan Economic CorridorDocument48 pagesChina Pakistan Economic CorridorRana ZaibNo ratings yet

- Long Range BudgetingDocument8 pagesLong Range BudgetingDahlia E. MakataNo ratings yet

- Manual The BoardroomDocument25 pagesManual The Boardroomradhika100% (1)

- Supplements SLCMDocument50 pagesSupplements SLCMAkshra MahajanNo ratings yet

- A Study On Employee SatisfactionDocument97 pagesA Study On Employee SatisfactionAvinash Joseph0% (1)

- Polangui Executive Summary 2012Document4 pagesPolangui Executive Summary 2012Retis, Thirdy SamanthaNo ratings yet

- Engineering Management Case Study #3 MOTORBUS Company: Que Sera SeraDocument5 pagesEngineering Management Case Study #3 MOTORBUS Company: Que Sera SeraApril Lyn SantosNo ratings yet

- PQU.M1 Module 1 Quality and Quality ManagementDocument22 pagesPQU.M1 Module 1 Quality and Quality Managementidris ekrem gülerNo ratings yet

- Abm CoursesDocument8 pagesAbm CoursesLiezl De JesusNo ratings yet

- Project On HSBCDocument11 pagesProject On HSBCShwetaMamaniaNo ratings yet

- Star River Electronic LTDDocument1 pageStar River Electronic LTDendiaoNo ratings yet

- Agamata Relevant Costing Chap 9 Short Term Decision PDFDocument2 pagesAgamata Relevant Costing Chap 9 Short Term Decision PDFJaira MoradaNo ratings yet

- Industrial ProjectDocument50 pagesIndustrial ProjectShrilogapriyaNo ratings yet

- Business Simulation Gallanosa National High School G4-Stem 2Document1 pageBusiness Simulation Gallanosa National High School G4-Stem 2KENNETH POLONo ratings yet

- Wealth InequalityDocument4 pagesWealth InequalityChun KedNo ratings yet

- Sree Narayana Guru College of Commerce... PrinceDocument7 pagesSree Narayana Guru College of Commerce... Princeakshay shirkeNo ratings yet

- Ch12 - Creating & Pricing Products - Group 6Document44 pagesCh12 - Creating & Pricing Products - Group 6helena danNo ratings yet

- Concord Jul19 PDFDocument49 pagesConcord Jul19 PDFsankhaginNo ratings yet

- DELOITTE - 2024 Global Automotive Consumer StudyDocument26 pagesDELOITTE - 2024 Global Automotive Consumer StudyAcevagner_StonedAceFrehleyNo ratings yet

- Lecture Topic 4 StudentDocument36 pagesLecture Topic 4 StudentSaaliha SaabiraNo ratings yet