You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- A B C D of E-BankingDocument75 pagesA B C D of E-Bankinglove tannaNo ratings yet

- Introduction of Online BankingDocument18 pagesIntroduction of Online BankingRavi Kashyap506No ratings yet

- New Black Book SanjayDocument71 pagesNew Black Book Sanjayshilpa jaiswal0% (1)

- Popular Uses and Security of ATM CardsDocument29 pagesPopular Uses and Security of ATM CardsMaruti a alavandiNo ratings yet

- Black Book Payment BankDocument62 pagesBlack Book Payment BankVicky VishwakarmaNo ratings yet

- Debit Card - Project Wark PDFDocument158 pagesDebit Card - Project Wark PDFManisha GuptaNo ratings yet

- Credit Cards Explained: Types, Features & MoreDocument27 pagesCredit Cards Explained: Types, Features & Morevineeth bunnyNo ratings yet

- Ranson Dantis Project Black Book TybmsDocument87 pagesRanson Dantis Project Black Book Tybmsranson dantisNo ratings yet

- Plastic Money Report on Credit and Debit CardsDocument55 pagesPlastic Money Report on Credit and Debit CardsDisha100% (1)

- Certificate and Project Report on Plastic MoneyDocument54 pagesCertificate and Project Report on Plastic MoneyRupesh Gupta57% (7)

- Growth of The Use of Plastic Money in IndiaDocument46 pagesGrowth of The Use of Plastic Money in IndiaHarshitGupta81% (21)

- Loans and Advances ManagementDocument18 pagesLoans and Advances ManagementSONIYA SINHA50% (4)

- Essential Guide to E-BankingDocument64 pagesEssential Guide to E-BankingRkenterpriseNo ratings yet

- Plastic Money in IndiaDocument71 pagesPlastic Money in IndiaDexter LoboNo ratings yet

- E Banking Report - Punjab National BankDocument65 pagesE Banking Report - Punjab National BankParveen ChawlaNo ratings yet

- Online Payment SystemDocument30 pagesOnline Payment SystemDjks YobNo ratings yet

- Plastic Money in IndiaDocument46 pagesPlastic Money in IndiaShrutikaKadam71% (7)

- Personal LoanDocument31 pagesPersonal LoanAravindVenkatraman100% (1)

- A Study of Credit Cards in Indian ScenarioDocument11 pagesA Study of Credit Cards in Indian ScenarioWifi Internet Cafe & Multi ServicesNo ratings yet

- Retail Banking Black BookDocument95 pagesRetail Banking Black Bookomprakash shindeNo ratings yet

- Credit Card InfoDocument79 pagesCredit Card Info888 Harshali polNo ratings yet

- Repoprt On Loans & Advances PDFDocument66 pagesRepoprt On Loans & Advances PDFTitas Manower50% (4)

- Retail Banking in India - An IntroductionDocument73 pagesRetail Banking in India - An Introductionnatakhatnirmal33% (3)

- Plastic Money in IndiaDocument35 pagesPlastic Money in IndiatarachandmaraNo ratings yet

- Consumer Perceptions of Plastic Money in PakistanDocument35 pagesConsumer Perceptions of Plastic Money in PakistanMaryam Zaidi60% (5)

- Plastic Money Word FileDocument60 pagesPlastic Money Word Fileshah sanket100% (1)

- Customer Satisfaction with ATM Services in SolanDocument75 pagesCustomer Satisfaction with ATM Services in Solandinesh_v_0076945100% (2)

- Online Banking Services Icici BankDocument51 pagesOnline Banking Services Icici BankMubeenNo ratings yet

- Yes BankDocument24 pagesYes Banktrisanka banikNo ratings yet

- POPULARITY OF CREDIT CARDS ISSUED BY DIFFERENT BANKSDocument25 pagesPOPULARITY OF CREDIT CARDS ISSUED BY DIFFERENT BANKSNaveed Karim Baksh75% (8)

- Credit CardDocument81 pagesCredit CardsuryakantshrotriyaNo ratings yet

- Finacle Command - TM For Transaction Maintainance Part - I - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersDocument4 pagesFinacle Command - TM For Transaction Maintainance Part - I - Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersShubham PathakNo ratings yet

- E Banking Project... P...Document69 pagesE Banking Project... P...Rohit Patil100% (1)

- Mobile banking conceptual model summaryDocument21 pagesMobile banking conceptual model summaryGill Varinder SinghNo ratings yet

- A Study On Plastic MoneyDocument43 pagesA Study On Plastic MoneyxcvNo ratings yet

- Alternate Revenue Sources Bank IDBI BankDocument35 pagesAlternate Revenue Sources Bank IDBI Bankalkanm75060% (5)

- A Study On Credit CardsDocument49 pagesA Study On Credit CardsSai Charan100% (1)

- Online Banking Services Icici BankDocument10 pagesOnline Banking Services Icici BankMohmmedKhayyumNo ratings yet

- HDFC Online BankingDocument24 pagesHDFC Online BankingAmardeep SinghNo ratings yet

- Study On Loans and AdvancesDocument58 pagesStudy On Loans and AdvancesUday Gowda100% (1)

- Axis Bank Debit and Credit Card SonamDocument81 pagesAxis Bank Debit and Credit Card SonamsonamNo ratings yet

- Banking FraudDocument24 pagesBanking FraudchaitudscNo ratings yet

- Scams in Banking SectorDocument90 pagesScams in Banking SectorDr Sachin Chitnis M O UPHC AiroliNo ratings yet

- Study of ICICI Home LoansDocument107 pagesStudy of ICICI Home LoansMukesh AwasthiNo ratings yet

- Plastic MoneyDocument74 pagesPlastic MoneySimranNo ratings yet

- Limitations of E-Banking: Security, Cost, AwarenessDocument1 pageLimitations of E-Banking: Security, Cost, AwarenessanithapblNo ratings yet

- Effect of Payment Banks on India's Financial SystemDocument6 pagesEffect of Payment Banks on India's Financial SystemNithin JoseNo ratings yet

- Types of Loan Offered by SBIDocument88 pagesTypes of Loan Offered by SBIShilpa Nikam67% (3)

- History of Payment BanksDocument4 pagesHistory of Payment Banksanshul4clNo ratings yet

- Bhavesh Jhala 1 PDFDocument42 pagesBhavesh Jhala 1 PDFAniket AutkarNo ratings yet

- Bank SynopsisDocument7 pagesBank SynopsisNiro ThakurNo ratings yet

- Payments Bank - WikipediaDocument12 pagesPayments Bank - WikipediaThiago FernandesNo ratings yet

- Payment Bank - A Need of Digital India: Abhinav National Monthly Refereed Journal of Research inDocument5 pagesPayment Bank - A Need of Digital India: Abhinav National Monthly Refereed Journal of Research inmonica niroliaNo ratings yet

- Payments BankDocument14 pagesPayments BankDurjoy BhattacharjeeNo ratings yet

- A Report OnDocument26 pagesA Report OnNihar HindochaNo ratings yet

- State Bank of India: A Pivotal Role in India's Banking SectorDocument91 pagesState Bank of India: A Pivotal Role in India's Banking Sectoraditya desaiNo ratings yet

- Payment and Small BanksDocument27 pagesPayment and Small BanksDr.Satish RadhakrishnanNo ratings yet

- Evolution of Insolvency and Bankrupt y Code 2016Document29 pagesEvolution of Insolvency and Bankrupt y Code 2016LAXMI KANTA GIRINo ratings yet

- Working Capital AnlysisDocument33 pagesWorking Capital AnlysisLAXMI KANTA GIRINo ratings yet

- Final ProjectDocument33 pagesFinal ProjectLAXMI KANTA GIRINo ratings yet

- Estimating Working Capital Requirements for TATA CompanyDocument35 pagesEstimating Working Capital Requirements for TATA CompanyLAXMI KANTA GIRINo ratings yet

- NALCO's Marketing Strategy ReportDocument73 pagesNALCO's Marketing Strategy ReportLAXMI KANTA GIRI100% (2)

- Chapter - I: Market Indexes Market RegulationDocument29 pagesChapter - I: Market Indexes Market RegulationLAXMI KANTA GIRINo ratings yet

- Commerce Project 3rd YearDocument28 pagesCommerce Project 3rd YearRanjeet Devgan100% (3)

- Chapter-1: Page - 1Document91 pagesChapter-1: Page - 1LAXMI KANTA GIRINo ratings yet

- Chapter - I: Market Indexes Market RegulationDocument29 pagesChapter - I: Market Indexes Market RegulationLAXMI KANTA GIRINo ratings yet

- IAG's Keys to Success in Life InsuranceDocument15 pagesIAG's Keys to Success in Life InsuranceEverson BoyDayz PetersNo ratings yet

- Economic Value AddedDocument9 pagesEconomic Value AddedLimisha ViswanathanNo ratings yet

- Complete Freedom: Statement of AccountDocument5 pagesComplete Freedom: Statement of AccountWenjie6567% (3)

- Cash and Liquidity Management - Topic 3Document47 pagesCash and Liquidity Management - Topic 3kodeNo ratings yet

- Course Plan Banking Activities IssuesDocument5 pagesCourse Plan Banking Activities IssuesRomzor ArecilNo ratings yet

- Condemnation BoardDocument10 pagesCondemnation BoardAnil GargNo ratings yet

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument2 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoRazor RRNo ratings yet

- Corporate Governance in Asia: Eight Case Studies: Robert W. Mcgee Florida International UniversityDocument38 pagesCorporate Governance in Asia: Eight Case Studies: Robert W. Mcgee Florida International UniversitySasboomNo ratings yet

- Literature Review of HDFC Home LoanDocument8 pagesLiterature Review of HDFC Home Loanafmzuiffugjdff100% (1)

- AMIS 525 Pop Quiz - Chapters 22 and 23Document5 pagesAMIS 525 Pop Quiz - Chapters 22 and 23ssregens82No ratings yet

- Bauxite Transfert PricingDocument21 pagesBauxite Transfert PricingEyock PierreNo ratings yet

- Demystifying Venture Capital Economics Part 1Document6 pagesDemystifying Venture Capital Economics Part 1Tarek FahimNo ratings yet

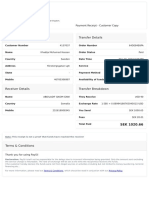

- Sender Details Transfer Details: Payment Receipt - CustomerDocument1 pageSender Details Transfer Details: Payment Receipt - CustomerAbshira Abdi AliNo ratings yet

- Global IME BankDocument29 pagesGlobal IME BankSujan Bajracharya100% (2)

- Common Stock ValuationDocument57 pagesCommon Stock ValuationNaeemNo ratings yet

- BADM 510 Global Business Strategic ManagementDocument71 pagesBADM 510 Global Business Strategic Managementclarknj100% (1)

- Management Consultancy Finals ReviewDocument20 pagesManagement Consultancy Finals ReviewGerlie89% (9)

- Impact of Interest Rate on Profitability of Nepalese Commercial BanksDocument11 pagesImpact of Interest Rate on Profitability of Nepalese Commercial Bankssangita KcNo ratings yet

- Treasury ManagementDocument9 pagesTreasury ManagementAkash BdNo ratings yet

- Insolvency and Bankruptcy Code RMDocument28 pagesInsolvency and Bankruptcy Code RMSarvy JosephNo ratings yet

- GO (P) N0.221-2014-Fin Dated 16-06-2014Document8 pagesGO (P) N0.221-2014-Fin Dated 16-06-2014T J AjitNo ratings yet

- Bond ValuationDocument13 pagesBond Valuationrahul_iiimNo ratings yet

- Punjab National BankDocument6 pagesPunjab National BankSai VasudevanNo ratings yet

- Senior 12 Business Finance - Q1 - M2 For PrintingDocument28 pagesSenior 12 Business Finance - Q1 - M2 For PrintingAngelica Paras100% (4)

- Golomt Bank Report - 2003 EnglishDocument43 pagesGolomt Bank Report - 2003 EnglishBarsbold100% (8)

- Concept of True & FairDocument7 pagesConcept of True & Fairyogiraj28No ratings yet

- Dearborn 2013 CatalogDocument51 pagesDearborn 2013 CatalogKristy Garvey Ketterman100% (1)

- Me443 CH5Document55 pagesMe443 CH5abhi9119No ratings yet

- Workers Participation in ManagementDocument18 pagesWorkers Participation in Managementakashhereakash100% (1)

- Lesson 9: Benefit/Cost Analysis and Public Sector Economics: Prof - Jessica Maria Paz S. Casimiro, Ce, Enp, DisdsDocument26 pagesLesson 9: Benefit/Cost Analysis and Public Sector Economics: Prof - Jessica Maria Paz S. Casimiro, Ce, Enp, DisdsAziezah PalintaNo ratings yet

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorFrom EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorNo ratings yet

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Streetsmart Financial Basics for Nonprofit Managers: 4th EditionFrom EverandStreetsmart Financial Basics for Nonprofit Managers: 4th EditionRating: 3.5 out of 5 stars3.5/5 (3)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)