You might also like

- Intermediate Accounting: Assignment 4: Exercise 4-6: Multiple-Step and Extraordinary ItemsDocument13 pagesIntermediate Accounting: Assignment 4: Exercise 4-6: Multiple-Step and Extraordinary ItemsMuhammad MalikNo ratings yet

- Latihan 3Document3 pagesLatihan 3Radit Ramdan NopriantoNo ratings yet

- 6-GL and FR CycleDocument6 pages6-GL and FR Cyclehangbg2k3No ratings yet

- CH 5Document2 pagesCH 5tigger5191No ratings yet

- CH 12Document2 pagesCH 12flrnciairn100% (1)

- P4-5 Consolidation Entries and Financial StatementsDocument3 pagesP4-5 Consolidation Entries and Financial StatementsErnike SariNo ratings yet

- 2014 CommentaryDocument46 pages2014 Commentaryduong duongNo ratings yet

- Tugas Chapter 6 - Sandra Hanania - 120110180024Document4 pagesTugas Chapter 6 - Sandra Hanania - 120110180024Sandra Hanania PasaribuNo ratings yet

- Consolidated Financial Statement Practice 3-2Document2 pagesConsolidated Financial Statement Practice 3-2Winnie TanNo ratings yet

- Diskusi Mid Test - Meeting 7Document26 pagesDiskusi Mid Test - Meeting 7Jimmy LimNo ratings yet

- Tutorial 6Document4 pagesTutorial 6Muntasir AhmmedNo ratings yet

- MIKROEKON.docx Pengantar Akuntansi II (Part 1Document38 pagesMIKROEKON.docx Pengantar Akuntansi II (Part 1Cok Angga PutraNo ratings yet

- CH 06Document48 pagesCH 06Fenny MarietzaNo ratings yet

- Chapter IAS 02 - Chapter 7 -QB only câu hỏiDocument7 pagesChapter IAS 02 - Chapter 7 -QB only câu hỏiMai LinhNo ratings yet

- IVplast Is Still Debating Whether It Should Introduce Y28Document2 pagesIVplast Is Still Debating Whether It Should Introduce Y28Elliot RichardNo ratings yet

- Acct 3533 Advanced Accounting Class Exercise Ch 3 Initial Value Cost MethodDocument3 pagesAcct 3533 Advanced Accounting Class Exercise Ch 3 Initial Value Cost MethodFiona TaNo ratings yet

- Financial accounting journal entriesDocument3 pagesFinancial accounting journal entriesAlfiyanNo ratings yet

- Earn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFDocument1 pageEarn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFAnbu jaromiaNo ratings yet

- CH08SOLSDocument23 pagesCH08SOLSMiki TiendaNo ratings yet

- Exercises Chapter1Document4 pagesExercises Chapter1Huyen Siu NhưnNo ratings yet

- FIN1161 - Introduction To Finance For Business - Report 2Document6 pagesFIN1161 - Introduction To Finance For Business - Report 2thunlagbd230128No ratings yet

- The Statement of Financial Position of Stancia Sa at DecemberDocument1 pageThe Statement of Financial Position of Stancia Sa at DecemberCharlotte100% (1)

- NRV vs Fair Value: Key DifferencesDocument5 pagesNRV vs Fair Value: Key DifferencesbinuNo ratings yet

- ch04 PDFDocument4 pagesch04 PDFMosharraf HussainNo ratings yet

- FINAL EXAM SOLUTIONDocument4 pagesFINAL EXAM SOLUTIONHaliza Nabila PutriNo ratings yet

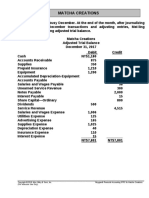

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Financial Planning - ForecastingDocument4 pagesFinancial Planning - ForecastingPrathamesh411No ratings yet

- ACC 557 Week 4 Chapter 6 E6 1 E6 10 E6 14 P6 3ADocument7 pagesACC 557 Week 4 Chapter 6 E6 1 E6 10 E6 14 P6 3Atswag2014No ratings yet

- Pullman Inc Manufactures Chain Hoists The Raw Materials Inventories OnDocument2 pagesPullman Inc Manufactures Chain Hoists The Raw Materials Inventories OnAmit Pandey0% (1)

- Animal Gear Company Makes Two Pet Carriers The Cat Allac andDocument2 pagesAnimal Gear Company Makes Two Pet Carriers The Cat Allac andAmit PandeyNo ratings yet

- Chapter 13 Homework Assignment #2 QuestionsDocument8 pagesChapter 13 Homework Assignment #2 QuestionsCole Doty0% (1)

- GDGDDocument14 pagesGDGDBen 10 YesNo ratings yet

- Decision Making dan PricingDocument4 pagesDecision Making dan PricingfauziyahNo ratings yet

- Financial Accounting and Reporting: RequirementsDocument4 pagesFinancial Accounting and Reporting: RequirementsebshuvoNo ratings yet

- Mac006 A T2 2021 FexDocument7 pagesMac006 A T2 2021 FexHaris MalikNo ratings yet

- Cost Allocation MethodsDocument2 pagesCost Allocation MethodsShahid NaseemNo ratings yet

- Bamfram PLC Is A Well Established Manufacturer of A SpecializedDocument2 pagesBamfram PLC Is A Well Established Manufacturer of A SpecializedAmit PandeyNo ratings yet

- Income Statement CH 4Document6 pagesIncome Statement CH 4Omar Hosny100% (1)

- Solutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your OwnDocument6 pagesSolutions Guide: Please Reword The Answers To Essay Type Parts So As To Guarantee That Your Answer Is An Original. Do Not Submit As Your OwnSkarlz ZyNo ratings yet

- Jawaban P5-6 Intermediate AccountingDocument3 pagesJawaban P5-6 Intermediate AccountingMutia WardaniNo ratings yet

- Problem 1: Organizing Categorical Variables: SolutionDocument34 pagesProblem 1: Organizing Categorical Variables: SolutionArgieshi GCNo ratings yet

- Taxation Questions on MinersDocument8 pagesTaxation Questions on MinersDanisa NdhlovuNo ratings yet

- Tutorial Laporan Arus KasDocument17 pagesTutorial Laporan Arus KasRatna DwiNo ratings yet

- Apple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Document1 pageApple Blossom Cologne Company Common Size Financial Statement Desember 31, 2003Lintang UtomoNo ratings yet

- Lease Problems Hw1Document6 pagesLease Problems Hw1Vi NguyenNo ratings yet

- Preliminary computations and consolidation of Piero SAADocument3 pagesPreliminary computations and consolidation of Piero SAAMuhammad SyukurNo ratings yet

- caCAF 01 Suggested Solution Autumn 2014Document8 pagescaCAF 01 Suggested Solution Autumn 2014shahroozkhanNo ratings yet

- Seminar 2-3Document8 pagesSeminar 2-3Nguyen Hien0% (1)

- 10 Exercises BE Solutions-1Document40 pages10 Exercises BE Solutions-1loveliangel0% (2)

- CH 03Document4 pagesCH 03flrnciairnNo ratings yet

- Advanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Document21 pagesAdvanced Cases For Cfs - Testbank Case 1: 905,410 Tax Paid (Cash Payment) Interest Paid (Cash Payments)Uyên Nguyễn Hoàng ThanhNo ratings yet

- WCPDocument6 pagesWCPkhanhleduy0% (1)

- CFAB - Accounting - QB - Chapter 9Document13 pagesCFAB - Accounting - QB - Chapter 9Nga Đào Thị Hằng100% (1)

- ACCT550 Homework Week 1Document6 pagesACCT550 Homework Week 1Natasha DeclanNo ratings yet

- P12 2aDocument4 pagesP12 2aMaria AngeliqueNo ratings yet

- Statement of CF - Dallas Ltd - Intermediate Level Exercise (1)Document4 pagesStatement of CF - Dallas Ltd - Intermediate Level Exercise (1)Như QuỳnhNo ratings yet

- Sb-Frs 7: Statutory Board Financial Reporting StandardDocument11 pagesSb-Frs 7: Statutory Board Financial Reporting StandardLuthfiWaeLaahNo ratings yet

- Illustrative Examples: A Statement of Cash Flows For An Entity Other Than A Financial InstitutionDocument9 pagesIllustrative Examples: A Statement of Cash Flows For An Entity Other Than A Financial InstitutionjohnNo ratings yet

- FRS 107 Ie 2016BBDocument10 pagesFRS 107 Ie 2016BBAmelia RahmawatiNo ratings yet

- Unit Test 6 PDFDocument2 pagesUnit Test 6 PDFMichał Zawiślak67% (3)

- Asia Risk QIS Special Report 2019 PDFDocument16 pagesAsia Risk QIS Special Report 2019 PDFStephane MysonaNo ratings yet

- Sa5 Pu 14 PDFDocument102 pagesSa5 Pu 14 PDFPolelarNo ratings yet

- Order by The Governor Notification: Government of Meghalay A Finance (Establishment) Department, ShillongDocument8 pagesOrder by The Governor Notification: Government of Meghalay A Finance (Establishment) Department, ShillongBadap SwerNo ratings yet

- INNOBIZ Presentation1-6Document13 pagesINNOBIZ Presentation1-6Juan Carlos ZamoraNo ratings yet

- Structured Trade Finance in Africa Rwanda Coffee and Tea Case StudiesDocument41 pagesStructured Trade Finance in Africa Rwanda Coffee and Tea Case StudiesmsidaNo ratings yet

- Liability AccountsDocument17 pagesLiability AccountsAsad ZaidiNo ratings yet

- Super Mandiwanzira Corruption Letter To President EDDocument12 pagesSuper Mandiwanzira Corruption Letter To President EDIcho ChariraNo ratings yet

- MCQ QuestionsDocument8 pagesMCQ Questionsvarma pranjalNo ratings yet

- Court Holds Preferred Shareholders Have No Right to Mortgaged Property Proceeds Until Debts PaidDocument2 pagesCourt Holds Preferred Shareholders Have No Right to Mortgaged Property Proceeds Until Debts PaidPaolo QuilalaNo ratings yet

- Bar Exam QuestionsDocument18 pagesBar Exam QuestionsAnonymous GMUQYq8No ratings yet

- M. M. Rahman Co.: Statement of Financial PositionDocument5 pagesM. M. Rahman Co.: Statement of Financial PositionAsiful IslamNo ratings yet

- Annual Report 2009 DNB Nor Bank AsaDocument114 pagesAnnual Report 2009 DNB Nor Bank AsaFrode HaukenesNo ratings yet

- Pest Analysis of MalaysiaDocument8 pagesPest Analysis of MalaysiaSai VasudevanNo ratings yet

- Chapter 4 TVM EditedDocument24 pagesChapter 4 TVM EditedWonde BiruNo ratings yet

- Basic Requirements For Registering Properties in The PhilippinesDocument2 pagesBasic Requirements For Registering Properties in The Philippinescrixzam100% (1)

- Cycles of Depressions: MacroeconomicsDocument17 pagesCycles of Depressions: MacroeconomicsCozma Alina DanielaNo ratings yet

- Instructions For Form 1120-L: U.S. Life Insurance Company Income Tax ReturnDocument18 pagesInstructions For Form 1120-L: U.S. Life Insurance Company Income Tax ReturnIRSNo ratings yet

- Essential guide to current liabilities and contingenciesDocument46 pagesEssential guide to current liabilities and contingenciesjdiaz_64624789% (9)

- Ship Economy: Lecture NotesDocument42 pagesShip Economy: Lecture NotesSDesigner1No ratings yet

- Gonzales V Yek TongDocument4 pagesGonzales V Yek TongHency TanbengcoNo ratings yet

- Working Capital Management Live Project Report by Pranay Jindal in Jindal Steel and PowerDocument83 pagesWorking Capital Management Live Project Report by Pranay Jindal in Jindal Steel and PowerPranay Jindal71% (7)

- Songambele SACCO Business Plan 2013-2017Document22 pagesSongambele SACCO Business Plan 2013-2017Andinet100% (1)

- Dib Banking Assignment 2023Document16 pagesDib Banking Assignment 2023zhekaiNo ratings yet

- HOW TO WIN IN COURT & Corruption ExposedDocument15 pagesHOW TO WIN IN COURT & Corruption ExposedArlie Taylor100% (22)

- Validation of sampling quality for feasibility studiesDocument11 pagesValidation of sampling quality for feasibility studiesAndrea GonzalezNo ratings yet

- Business Math Notes PDFDocument12 pagesBusiness Math Notes PDFCzareena Sulica DiamaNo ratings yet

- The Doctrine of Part PerformanceDocument13 pagesThe Doctrine of Part PerformanceishwarNo ratings yet

- Deloitte - 2024 Banking and Capital Markets Outlooks-TrangDocument28 pagesDeloitte - 2024 Banking and Capital Markets Outlooks-Trangthaovy08090499No ratings yet

- Cash Flow Analysis Itc LTD: Sayon Das 1421328 MbalDocument4 pagesCash Flow Analysis Itc LTD: Sayon Das 1421328 MbalSayon DasNo ratings yet

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)From EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Rating: 4.5 out of 5 stars4.5/5 (12)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindFrom EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindRating: 5 out of 5 stars5/5 (231)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Profit First for Therapists: A Simple Framework for Financial FreedomFrom EverandProfit First for Therapists: A Simple Framework for Financial FreedomNo ratings yet

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)From EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Rating: 4.5 out of 5 stars4.5/5 (5)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantFrom EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantRating: 4.5 out of 5 stars4.5/5 (146)

- Financial Accounting For Dummies: 2nd EditionFrom EverandFinancial Accounting For Dummies: 2nd EditionRating: 5 out of 5 stars5/5 (10)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Getting to Yes: How to Negotiate Agreement Without Giving InFrom EverandGetting to Yes: How to Negotiate Agreement Without Giving InRating: 4 out of 5 stars4/5 (652)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetFrom EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNo ratings yet

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!From EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Rating: 4.5 out of 5 stars4.5/5 (14)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)From EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Rating: 4 out of 5 stars4/5 (33)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyFrom EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)