You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Managing Manufacturing Performance (MMP) Code May 2014 PDFDocument102 pagesManaging Manufacturing Performance (MMP) Code May 2014 PDFMónica Prado LinceNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Asset Management AgreementDocument4 pagesAsset Management AgreementMarc BaronNo ratings yet

- UAL Reorganization Memo 5.29 FINALDocument2 pagesUAL Reorganization Memo 5.29 FINALAnn DwyerNo ratings yet

- Vikas CVDocument2 pagesVikas CVlegalitis.inNo ratings yet

- Company Profile: "Scales You Trust, Services You Can Depend On."Document1 pageCompany Profile: "Scales You Trust, Services You Can Depend On."Jonathan Ponce Santos QuizonNo ratings yet

- The Job Fair BookletDocument43 pagesThe Job Fair BookletjobcareerscNo ratings yet

- BIR NO DirectoryDocument48 pagesBIR NO DirectoryRB BalanayNo ratings yet

- Introduction To HRMDocument28 pagesIntroduction To HRMMd SalauddinNo ratings yet

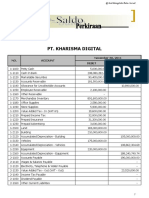

- Kunci Jawaban Pt. Kharisma DigitalDocument91 pagesKunci Jawaban Pt. Kharisma DigitalSanti Mulya100% (3)

- At 2515 Completing The Audit andDocument31 pagesAt 2515 Completing The Audit andawesome bloggersNo ratings yet

- TechnBidLT45 PDFDocument103 pagesTechnBidLT45 PDFMadhav PurohitNo ratings yet

- Create A Standard Memo LinesDocument10 pagesCreate A Standard Memo LinesSrinivasa Rao AsuruNo ratings yet

- A Study of Fanancial AnalysisDocument9 pagesA Study of Fanancial AnalysisRoshan KhadkaNo ratings yet

- Malaysia Comp PlanDocument6 pagesMalaysia Comp Planfusuke9No ratings yet

- 21 Finance Interview Questions and AnswersDocument17 pages21 Finance Interview Questions and Answersdaniel18ct100% (1)

- Restaurant Marketing Plan TemplateDocument15 pagesRestaurant Marketing Plan TemplateBridget Zanele NyabaNo ratings yet

- Social Enterprises and Their Ecosystems in Europe. Updated Country Report SpainDocument130 pagesSocial Enterprises and Their Ecosystems in Europe. Updated Country Report SpainPierre CamiloNo ratings yet

- HRMS Absence Management Process PDFDocument3 pagesHRMS Absence Management Process PDFMohammed Abdelfttah MustafaNo ratings yet

- Session 6. The Statement of Cash FlowsDocument22 pagesSession 6. The Statement of Cash FlowsAmrutaNo ratings yet

- Cold Chain 1Document36 pagesCold Chain 1Achal VenkateshNo ratings yet

- The Empathy EdgeDocument2 pagesThe Empathy EdgeNisha lakraNo ratings yet

- Project WefwffDocument31 pagesProject WefwffVivek KumarNo ratings yet

- Skills Matrix What It Is and Why Do You Need To Create OneDocument11 pagesSkills Matrix What It Is and Why Do You Need To Create OneKeith SpencerNo ratings yet

- Case SummaryDocument11 pagesCase SummaryAditya ChaudharyNo ratings yet

- Applications of Mathematics in BusinessDocument11 pagesApplications of Mathematics in Businessgursimar kaurNo ratings yet

- FLIPPING MARKETS and TRADING HUBDocument25 pagesFLIPPING MARKETS and TRADING HUBFaliq Hukma ANo ratings yet

- Challenge To World-Class ManufacturingDocument12 pagesChallenge To World-Class ManufacturingSantiago Javier Chimarro Torres100% (1)

- Basics of Performance AppraisalsDocument8 pagesBasics of Performance AppraisalsadityasageNo ratings yet

- Datasheet - AVEVA Manufacturing Execution System - 23-01Document9 pagesDatasheet - AVEVA Manufacturing Execution System - 23-01manpreetNo ratings yet

- Financial Institutional Support To Exporters: Sidbi EXIM Bank EcgcDocument10 pagesFinancial Institutional Support To Exporters: Sidbi EXIM Bank EcgcAshvin RavriyaNo ratings yet