You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Expert Committee On Micro, Small and Medium PDFDocument142 pagesExpert Committee On Micro, Small and Medium PDFpls2019No ratings yet

- Monetary Policy Statement April 2020Document92 pagesMonetary Policy Statement April 2020pls2019No ratings yet

- Msme Report PDFDocument142 pagesMsme Report PDFpls2019No ratings yet

- Payment Gateways and Payment AggregatorsDocument1 pagePayment Gateways and Payment Aggregatorspls2019No ratings yet

- State Budgets StudyDocument2 pagesState Budgets Studypls2019No ratings yet

- Digital PaymentsDocument2 pagesDigital Paymentspls2019No ratings yet

- Monthly Bulletin PDFDocument1 pageMonthly Bulletin PDFpls2019No ratings yet

- Select Economic IndicatorsDocument1 pageSelect Economic Indicatorspls2019No ratings yet

- Rbi ReportDocument83 pagesRbi Reportpls2019No ratings yet

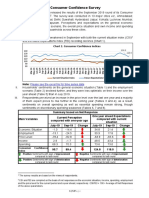

- Consumer Confidence SurveyDocument4 pagesConsumer Confidence Surveypls2019No ratings yet

- Monetary Policy ReportDocument75 pagesMonetary Policy Reportpls2019No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- FSA Midterm Exam FormattedDocument8 pagesFSA Midterm Exam Formattedkarthikmaddula007_66No ratings yet

- Assignment 4 - Sec JDocument9 pagesAssignment 4 - Sec JRafayGhafoorNo ratings yet

- Meet Your Strawman by David E RobinsonDocument83 pagesMeet Your Strawman by David E RobinsonTheOfficialBeZiiNo ratings yet

- Home First Finance Company India Limited: Issue HighlightsDocument16 pagesHome First Finance Company India Limited: Issue HighlightstempvjNo ratings yet

- Dela Cruz Randy BombioDocument7 pagesDela Cruz Randy Bombiojaice tobit tabuenaNo ratings yet

- History of Philippine BankingDocument6 pagesHistory of Philippine BankingJohn Kenneth BoholNo ratings yet

- PT Terus JayaDocument16 pagesPT Terus JayaLinda Wati PriwotoNo ratings yet

- Universal BankingDocument25 pagesUniversal BankingRahul SethNo ratings yet

- The Institution of Engineers (India) : (For Member Technologist Applicants)Document8 pagesThe Institution of Engineers (India) : (For Member Technologist Applicants)dipinnediyaparambathNo ratings yet

- How To Contact Chase - Servicing & Mortgage Files - Chase Home Finance LLCDocument4 pagesHow To Contact Chase - Servicing & Mortgage Files - Chase Home Finance LLC83jjmackNo ratings yet

- Arnold Van Den Berg Power Point Jan 29 2020Document60 pagesArnold Van Den Berg Power Point Jan 29 2020Gonzalo Vera MirandaNo ratings yet

- Sales: Date Party Ch. No. Particulars Rate Sub Total 18%GST Amount Type Date AmountDocument14 pagesSales: Date Party Ch. No. Particulars Rate Sub Total 18%GST Amount Type Date Amountjivan pawarNo ratings yet

- Commerce - Bcom Banking and Insurance - Semester 5 - 2023 - April - Financial Reporting Analysis CbcgsDocument6 pagesCommerce - Bcom Banking and Insurance - Semester 5 - 2023 - April - Financial Reporting Analysis CbcgsVishakha VishwakarmaNo ratings yet

- Placement Training Centre Bank Interview Questions and AnswersDocument20 pagesPlacement Training Centre Bank Interview Questions and AnswershariNo ratings yet

- Prasun Patel - Banking & FinanceDocument3 pagesPrasun Patel - Banking & FinanceGhanshyam NfsNo ratings yet

- Mechanics of Futures Markets: Daily Settlement or Marking-To-MarketDocument42 pagesMechanics of Futures Markets: Daily Settlement or Marking-To-MarketRafaat ShaeerNo ratings yet

- Custodial ServicesDocument6 pagesCustodial ServicesKARISHMAATA2No ratings yet

- Collection ReceiptDocument1 pageCollection Receiptcmd.rnsmNo ratings yet

- 62 - 71 Lecture Notes SOCF (1-10)Document5 pages62 - 71 Lecture Notes SOCF (1-10)manadish nawazNo ratings yet

- NTPC Limited - Balance Sheet (In Rs. Crores)Document21 pagesNTPC Limited - Balance Sheet (In Rs. Crores)krishbalu172164No ratings yet

- The Legend of Situ BagenditDocument3 pagesThe Legend of Situ BagenditVisby NNo ratings yet

- Advantages and Disadvantages of Different Methods of Payment-2Document21 pagesAdvantages and Disadvantages of Different Methods of Payment-2api-549594574No ratings yet

- Working Capital Management Sample ProblemsDocument4 pagesWorking Capital Management Sample ProblemsJames InferidoNo ratings yet

- Midterm Exam With Key Ia3 PcuDocument6 pagesMidterm Exam With Key Ia3 PcuLyka CataynaNo ratings yet

- Navy Comptroller ManualDocument701 pagesNavy Comptroller ManualThe MajorNo ratings yet

- Bir Ruling - Exemption of Donation From DSTDocument10 pagesBir Ruling - Exemption of Donation From DSTDenise Capacio LirioNo ratings yet

- QP - Project FinanceDocument2 pagesQP - Project FinancePuneet GargNo ratings yet

- Venture Capital BankDocument15 pagesVenture Capital BankMeemo GhulamNo ratings yet

- Daily Fund Report-PCSO Daily ReportDocument2 pagesDaily Fund Report-PCSO Daily ReportFranz Thelen Lozano CariñoNo ratings yet

- EC4177/BA4177 Test 2 Study Guide CH 12 Exchange Rate DeterminationDocument2 pagesEC4177/BA4177 Test 2 Study Guide CH 12 Exchange Rate DeterminationSandip AgarwalNo ratings yet