You might also like

- Wealth Management Business PlanDocument18 pagesWealth Management Business PlanVageesh Kumar100% (2)

- Advanced Portfolio Management: A Quant's Guide for Fundamental InvestorsFrom EverandAdvanced Portfolio Management: A Quant's Guide for Fundamental InvestorsNo ratings yet

- Article 5 - Advancing Financial Reporting in The Age of Technology An Interview With Robert H. HerzDocument9 pagesArticle 5 - Advancing Financial Reporting in The Age of Technology An Interview With Robert H. HerzFakhmol RisepdoNo ratings yet

- BFIN 300 SP 19 Final Guideline AnswersDocument9 pagesBFIN 300 SP 19 Final Guideline AnswersZafran AqilNo ratings yet

- AD1 - FIN 5001 ProjectDocument6 pagesAD1 - FIN 5001 ProjectVinay PandeyNo ratings yet

- Karur Vysya Bank Is A Scheduled Commercial BankDocument4 pagesKarur Vysya Bank Is A Scheduled Commercial BankMamtha KumarNo ratings yet

- Raroc NewDocument2 pagesRaroc NewAtiaTahiraNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Repeatability and Reproducibility: Add To CartDocument3 pagesRepeatability and Reproducibility: Add To CartBALAJINo ratings yet

- A Comparative Study Betwe Traditional and Esg Dimensions For Port ConstructionDocument26 pagesA Comparative Study Betwe Traditional and Esg Dimensions For Port ConstructionSiddhesh SheteNo ratings yet

- Problems-Chapter 2Document5 pagesProblems-Chapter 2An VyNo ratings yet

- Investment AvenueDocument6 pagesInvestment AvenueObaid KhanNo ratings yet

- Holdings - Us - Emerging Markets Small Cap Portfolio IDocument136 pagesHoldings - Us - Emerging Markets Small Cap Portfolio IRajanThree WaliaNo ratings yet

- DTA's Morning Cafe-04th Oct 2021Document1 pageDTA's Morning Cafe-04th Oct 2021aaryinfoNo ratings yet

- Risk Return ProblemsDocument5 pagesRisk Return ProblemsRanganathchowdaryNo ratings yet

- Template Warrant Screeening SA Ver.2Document15 pagesTemplate Warrant Screeening SA Ver.2Dieba AcousticNo ratings yet

- Chapter 3 Part 3Document30 pagesChapter 3 Part 3Aditya GhoshNo ratings yet

- Holdings - Us - World Ex Us Core Equity PortfolioDocument287 pagesHoldings - Us - World Ex Us Core Equity PortfolioWind AjhaNo ratings yet

- Group 11 CF-2 Assignment (24-3-23)Document6 pagesGroup 11 CF-2 Assignment (24-3-23)Ankit RajNo ratings yet

- Zuze FungaiDocument1 pageZuze FungaiLainoNo ratings yet

- Bobi CDocument4 pagesBobi Cwishy1516No ratings yet

- Analysis of The Banking SectorDocument19 pagesAnalysis of The Banking SectorAli ShaikhNo ratings yet

- Case 3Document6 pagesCase 3Dipali SinghNo ratings yet

- Airan RatioDocument2 pagesAiran RatiomilanNo ratings yet

- Canara Robeco Savings Fund: Monthly Portfolio Statement As On April 30, 2022Document6 pagesCanara Robeco Savings Fund: Monthly Portfolio Statement As On April 30, 2022Gunvi COTTON ANALYSIS (I) PRIVATE LIMITEDNo ratings yet

- Inventory Model. Weighted Average and Moving Average Calculation. Multiple SkusDocument1 pageInventory Model. Weighted Average and Moving Average Calculation. Multiple SkusNurul islamNo ratings yet

- Profitability On Sales and InvestmentDocument3 pagesProfitability On Sales and InvestmentKunal SharmaNo ratings yet

- Farha ProjectDocument18 pagesFarha ProjectBhavya PabbisettyNo ratings yet

- Economic Analysis: Company Name Suscok Jaya GemilangDocument1 pageEconomic Analysis: Company Name Suscok Jaya GemilangSamuel ArelianoNo ratings yet

- Revenue Budget 14041 2016-17Document1 pageRevenue Budget 14041 2016-17Vibhore Kumar SainiNo ratings yet

- Assignment 6 - Jaime LievanoDocument7 pagesAssignment 6 - Jaime LievanoJaime LievanoNo ratings yet

- Bond and Stock ValutionsDocument23 pagesBond and Stock ValutionsNikhil TurkarNo ratings yet

- CyientDLMAnchor Allocation IntimationDocument3 pagesCyientDLMAnchor Allocation IntimationSaurav Kumar SinghNo ratings yet

- Chapter 2 AnswerDocument11 pagesChapter 2 AnswerLogeswary VijayakumarNo ratings yet

- IN000426P016 5.63% GOI Strips (MD 12/04/2026) IN000426C030 GOI Strips (MD 12/04/2026)Document3 pagesIN000426P016 5.63% GOI Strips (MD 12/04/2026) IN000426C030 GOI Strips (MD 12/04/2026)vishwesheswaran1No ratings yet

- HILLAS AQUA FARMS - FinancialsDocument42 pagesHILLAS AQUA FARMS - FinancialsCA Pavan KumarNo ratings yet

- CF AssignmentDocument24 pagesCF AssignmentAditya Kumar SinghNo ratings yet

- BUS AssignmentDocument2 pagesBUS AssignmentN HNo ratings yet

- IGS Digital Center - Commission & SurchargeDocument23 pagesIGS Digital Center - Commission & SurchargeBikash KumarNo ratings yet

- Shankar Santhanam Beta Case SolDocument2 pagesShankar Santhanam Beta Case SolKrushna Omprakash MundadaNo ratings yet

- Balance Sheet of Hero Honda MotorsDocument2 pagesBalance Sheet of Hero Honda MotorsMehul ShuklaNo ratings yet

- KKJJHHHGGDocument47 pagesKKJJHHHGGJuan SanguinetiNo ratings yet

- Risk Hedging: Investment Analysis and Portfolio ManagementDocument16 pagesRisk Hedging: Investment Analysis and Portfolio ManagementPhuong Anh NguyenNo ratings yet

- Take Home AssignmentDocument2 pagesTake Home AssignmentPravanjan AumcapNo ratings yet

- Data Sampel PerusahaanDocument17 pagesData Sampel Perusahaandiananowo7No ratings yet

- CAPM Numerical - With FormulaDocument8 pagesCAPM Numerical - With FormulaJaya RoyNo ratings yet

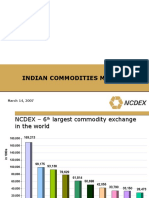

- Indian Commodities Market: March 14, 2007Document40 pagesIndian Commodities Market: March 14, 2007parishkaaNo ratings yet

- BE 3406 Answer 2016Document8 pagesBE 3406 Answer 2016PartheepanPartheeNo ratings yet

- Day 2 Formulas and FunctionsDocument8 pagesDay 2 Formulas and FunctionsShubham KulkarniNo ratings yet

- Daily Stock Market Report 26 November 2019 by Indira SecuritiesDocument10 pagesDaily Stock Market Report 26 November 2019 by Indira SecuritiesIndiaSecuritiesNo ratings yet

- FI Securities Market in India:: An OverviewDocument9 pagesFI Securities Market in India:: An OverviewlamlukerteNo ratings yet

- Stock Valuation SheetDocument6 pagesStock Valuation Sheetthouseef06No ratings yet

- Presented by Harichandana Y (2001MBA018) Sanskriti Bharti (2001MBA022) Pragati Upadhya (2001MBA110)Document23 pagesPresented by Harichandana Y (2001MBA018) Sanskriti Bharti (2001MBA022) Pragati Upadhya (2001MBA110)Harichandana YNo ratings yet

- LM 1753Document11 pagesLM 1753Jahangir ChohanNo ratings yet

- Airline Billing Statement by Area Code: BSP - United Arab EmirDocument76 pagesAirline Billing Statement by Area Code: BSP - United Arab Emiradnan altawilyNo ratings yet

- Strategy Research: Input ParametersDocument233 pagesStrategy Research: Input Parametersapi-26370089No ratings yet

- Financial Models - 2022Document9 pagesFinancial Models - 2022Hamza AsifNo ratings yet

- Daily Market Update 18.01Document1 pageDaily Market Update 18.01Inde Pendent LkNo ratings yet

- Portfolio Assignment 3Document3 pagesPortfolio Assignment 3Rashedul IslamNo ratings yet

- Gladys ShereniDocument1 pageGladys ShereniLainoNo ratings yet

- JSW Steel: (Jswste)Document8 pagesJSW Steel: (Jswste)XYZNo ratings yet

- Jaime F Vara de Rey Campuzano - Convertible Bonds Pricing Model - FVDocument593 pagesJaime F Vara de Rey Campuzano - Convertible Bonds Pricing Model - FVJaime Vara De ReyNo ratings yet

- INTERACTIVEDocument6 pagesINTERACTIVEdavid brentNo ratings yet

- Econf412 Finf313 Mids SDocument11 pagesEconf412 Finf313 Mids SArchita SrivastavaNo ratings yet

- Risq Vba JDDocument6 pagesRisq Vba JDabhijeetkaushalNo ratings yet

- Technical Analysis of Market Black BookDocument8 pagesTechnical Analysis of Market Black Bookakash mauryaNo ratings yet

- Class Notes: Set 1: Brief Overview of Finance BasicsDocument34 pagesClass Notes: Set 1: Brief Overview of Finance BasicsMuhammad Ikhlaq Ahmed KalrooNo ratings yet

- Sources of Finance (Mba Subject)Document37 pagesSources of Finance (Mba Subject)Riyas ParakkattilNo ratings yet

- Advanced Ratios in Mutual Fund Part1Document19 pagesAdvanced Ratios in Mutual Fund Part1Invest EasyNo ratings yet

- FourDocument26 pagesFouruppaliNo ratings yet

- Economicmodel of Roic Eva WaccDocument29 pagesEconomicmodel of Roic Eva Waccbernhardf100% (1)

- 08IMR (December2011)Document20 pages08IMR (December2011)Mofid Securities CompanyNo ratings yet

- Ross Corporate 13e PPT CH16 AccessibleDocument26 pagesRoss Corporate 13e PPT CH16 Accessiblemaigiangngoc2004No ratings yet

- 1 What Is The Expected Return and Standard Deviation ofDocument2 pages1 What Is The Expected Return and Standard Deviation ofAmit PandeyNo ratings yet

- How Sustainable Is Participatory Watershed Development in IndiaDocument10 pagesHow Sustainable Is Participatory Watershed Development in IndiaSirisha AdamalaNo ratings yet

- Equity: Learning ObjectivesDocument62 pagesEquity: Learning ObjectivesElaine Lingx100% (1)

- Dubai Islamic BankDocument3 pagesDubai Islamic Bankumair20062010100% (1)

- Investment Management - Lecture MaterialDocument16 pagesInvestment Management - Lecture MaterialMeyta AriantiNo ratings yet

- MLP FundsDocument19 pagesMLP FundsJosh DudumNo ratings yet

- Normal 5ff39c61763f8Document3 pagesNormal 5ff39c61763f8j2009jsNo ratings yet

- Stock Market Investment GuideDocument24 pagesStock Market Investment GuideHarlz Ranch100% (2)

- 2012 Annual Report AcerinoxDocument142 pages2012 Annual Report Acerinoxaniket_ghoseNo ratings yet

- Quizzes - Topic 2 - Xem L I Bài LàmDocument6 pagesQuizzes - Topic 2 - Xem L I Bài Làmnhunghuyen159No ratings yet

- SYNDICATE B - Primus Automation Division, 2002Document21 pagesSYNDICATE B - Primus Automation Division, 2002meidianizaNo ratings yet

- Cap. 5 The Statement of Cash FlowsDocument42 pagesCap. 5 The Statement of Cash FlowsJose Rafael Roman-NievesNo ratings yet

- Cheat Sheet FinanceDocument2 pagesCheat Sheet FinanceDenisNo ratings yet

- Truthofthe Stock Tape PDFDocument36 pagesTruthofthe Stock Tape PDFCardoso PenhaNo ratings yet

- Practice Questions Forward Rate CalculationDocument32 pagesPractice Questions Forward Rate CalculationUtkarsh GoradiaNo ratings yet

- 2020-21 Annual Report For South East WaterDocument171 pages2020-21 Annual Report For South East WaterChristopher Browne ValenzuelaNo ratings yet

- Mergers and Acquisitions Toolkit - Overview and ApproachDocument55 pagesMergers and Acquisitions Toolkit - Overview and ApproachMaria AngelNo ratings yet