You might also like

- Real Estate Taxation - 12.11.15Document8 pagesReal Estate Taxation - 12.11.15Juan Frivaldo100% (2)

- Calculate Capital Gains Tax on Real Property Sales and Principal ResidencesDocument20 pagesCalculate Capital Gains Tax on Real Property Sales and Principal ResidencesClang SantiagoNo ratings yet

- SolutionsDocument2 pagesSolutionsRejesh MeladNo ratings yet

- Real Estate Finance Economics Quiz SummaryDocument4 pagesReal Estate Finance Economics Quiz Summaryharriet daleNo ratings yet

- Understanding Taxes and Estate TaxesDocument56 pagesUnderstanding Taxes and Estate TaxesJewel Mae MercadoNo ratings yet

- Legal Aspects of Sales, Mortgages and LeasesDocument15 pagesLegal Aspects of Sales, Mortgages and LeasesErika Lusterio100% (1)

- Real Estate Service Act of The Philippines PDFDocument15 pagesReal Estate Service Act of The Philippines PDFVener Angelo MargalloNo ratings yet

- Finals ElectiveDocument126 pagesFinals ElectiveCristine TabilismaNo ratings yet

- Back-Up AgriculturalDocument32 pagesBack-Up AgriculturalMarkein Dael VirtudazoNo ratings yet

- 015 June 10, 2023 Problem Solving PRCDocument20 pages015 June 10, 2023 Problem Solving PRCPrince EG DltgNo ratings yet

- REB SAMPLE ONLY 10 Items Mock Exam 1 General and FundamentalsDocument2 pagesREB SAMPLE ONLY 10 Items Mock Exam 1 General and FundamentalsYen055No ratings yet

- Answer - Hidden Ep Quiz 15Document13 pagesAnswer - Hidden Ep Quiz 15Reymond IgayaNo ratings yet

- Rem 110 Term 3 QuizDocument6 pagesRem 110 Term 3 QuizJayson Cerias100% (1)

- Simulation 1 With Answer KeyDocument9 pagesSimulation 1 With Answer KeyREB2020100% (2)

- Broker Reviewer 2022Document8 pagesBroker Reviewer 2022Janzel SantillanNo ratings yet

- 2WK1 - Objectives and Purposes of Property ManagementDocument9 pages2WK1 - Objectives and Purposes of Property ManagementAnna SalinoNo ratings yet

- Real Estate Brokerage Practice ExamDocument67 pagesReal Estate Brokerage Practice ExamLeslie Anne De JesusNo ratings yet

- Reb NotesDocument39 pagesReb NotesART SORONGONNo ratings yet

- 3 REB Practice QuestionsDocument27 pages3 REB Practice QuestionsPrince EG DltgNo ratings yet

- 1.4 Real-Estate-Taxation With Problems and Answers - REBDocument82 pages1.4 Real-Estate-Taxation With Problems and Answers - REBgore.solivenNo ratings yet

- Real Estate Brokerage PrinciplesDocument3 pagesReal Estate Brokerage PrinciplesMarisseAnne Coquilla100% (1)

- Philippine real estate appraisal seminar conceptsDocument9 pagesPhilippine real estate appraisal seminar conceptsDiwaNo ratings yet

- SOREV Income Approach DiagnosticDocument4 pagesSOREV Income Approach DiagnosticReyn شكرا100% (1)

- Real Estate Appraiser or Review Appraiser or Commercial PropertyDocument2 pagesReal Estate Appraiser or Review Appraiser or Commercial Propertyapi-121671216No ratings yet

- MCQ Re EconomicsDocument4 pagesMCQ Re EconomicsAB AgostoNo ratings yet

- Mock. Exam-Code-of-Ethics-RA-9646Document10 pagesMock. Exam-Code-of-Ethics-RA-9646Carl Uy OngchocoNo ratings yet

- Real Estate Economics Set Nine MCQDocument19 pagesReal Estate Economics Set Nine MCQChristopher Gutierrez CalamiongNo ratings yet

- Module 2 ExamDocument12 pagesModule 2 ExamRoger ChivasNo ratings yet

- BP 220 PD 957 QuestionnaireDocument5 pagesBP 220 PD 957 QuestionnaireJan WickNo ratings yet

- Amended Guidelines Abot-Kamay Pabahay Program'Document30 pagesAmended Guidelines Abot-Kamay Pabahay Program'Ge-An Moiseah Salud AlmueteNo ratings yet

- Practice SetDocument39 pagesPractice SetDionico O. Payo Jr.No ratings yet

- Case Study - Ethical Standard For Real Estate PracticeDocument2 pagesCase Study - Ethical Standard For Real Estate PracticeATRIU NASH CADALINNo ratings yet

- Appraisal Steps: Determining Market Value of PropertyDocument9 pagesAppraisal Steps: Determining Market Value of PropertyAttyGalva22No ratings yet

- Real Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemDocument4 pagesReal Estate Mathematics Sample Problems (Ref: 0505) : I. Perimeter Fencing ProblemGeorge Poligratis RicoNo ratings yet

- Baap ReaDocument17 pagesBaap ReaJasielle Leigh UlangkayaNo ratings yet

- 3.1n Theories & Principles - UnlockedDocument11 pages3.1n Theories & Principles - Unlockedccc100% (1)

- Appraiser Exam Mock SetDocument10 pagesAppraiser Exam Mock SetJosue Sandigan Biolon SecorinNo ratings yet

- 3.6 Basic REA For REBDocument107 pages3.6 Basic REA For REBgore.solivenNo ratings yet

- Real Estate EconomicsDocument7 pagesReal Estate EconomicsDiana Alexandra Comaromi0% (1)

- Quick Notes Real Estate TaxationDocument3 pagesQuick Notes Real Estate TaxationJoshelle B. Bancilo100% (1)

- 3.09 Set 3 Mock Exam ReaDocument5 pages3.09 Set 3 Mock Exam Reabhobot riveraNo ratings yet

- A.2 Usprcp Rec CodeDocument25 pagesA.2 Usprcp Rec Codebhobot riveraNo ratings yet

- Fundamentals of Property Ownership - Philippine Real Estate Broker ReviewerDocument5 pagesFundamentals of Property Ownership - Philippine Real Estate Broker ReviewerRhea SunshineNo ratings yet

- Day 9 Fundamentals of REA ExamDocument10 pagesDay 9 Fundamentals of REA ExamKijiNo ratings yet

- Real Estate Broker Board ExamDocument2 pagesReal Estate Broker Board ExamTheSummitExpressNo ratings yet

- Legal Aspects of Sales, Mortgages & LeasesDocument3 pagesLegal Aspects of Sales, Mortgages & LeasesJoshua Armesto100% (2)

- 3.1 Theories & Principles of AppraisalDocument10 pages3.1 Theories & Principles of AppraisalWilliam L. Floresta100% (1)

- Toaz - Info Exam Final Coaching 2014 Mock Board Part I Answers PRDocument5 pagesToaz - Info Exam Final Coaching 2014 Mock Board Part I Answers PRLouie CoNo ratings yet

- Real Estate Taxation - Transfer of PropertyDocument9 pagesReal Estate Taxation - Transfer of PropertyJuan FrivaldoNo ratings yet

- Real Estate Finance and Economics - Quiz - 10feb2023 - PrintedDocument8 pagesReal Estate Finance and Economics - Quiz - 10feb2023 - Printedivy jane estrella100% (2)

- Alawa Cresar 2015 Basic Appraisal For RebDocument52 pagesAlawa Cresar 2015 Basic Appraisal For RebRheneir MoraNo ratings yet

- Special & Technical Knowledge for Real EstateDocument6 pagesSpecial & Technical Knowledge for Real EstateJuan Carlos NocedalNo ratings yet

- PARA SeminarDocument2 pagesPARA SeminarShielaMarie MalanoNo ratings yet

- Fundamental of Property OwnershipDocument5 pagesFundamental of Property OwnershipJosue Sandigan Biolon SecorinNo ratings yet

- Output Tax and Input TaxDocument12 pagesOutput Tax and Input TaxKiro ParafrostNo ratings yet

- Real Estate Appraisal BasicsDocument4 pagesReal Estate Appraisal Basicsbea100% (1)

- A Guide for Commercial Real Estate AgentsFrom EverandA Guide for Commercial Real Estate AgentsRating: 2 out of 5 stars2/5 (2)

- Comprehensive Reviewer for Real Estate TaxationDocument7 pagesComprehensive Reviewer for Real Estate TaxationJuan Frivaldo33% (3)

- Pre-Test & Post-TestDocument2 pagesPre-Test & Post-TestJuan FrivaldoNo ratings yet

- Answers - Accounting For MaterialsDocument6 pagesAnswers - Accounting For MaterialsJuan FrivaldoNo ratings yet

- Full Absorption & Variable Costing Methods (Answers)Document3 pagesFull Absorption & Variable Costing Methods (Answers)Juan FrivaldoNo ratings yet

- Answers - Accounting For MaterialsDocument6 pagesAnswers - Accounting For MaterialsJuan FrivaldoNo ratings yet

- Practice 2 - MGT008Document9 pagesPractice 2 - MGT008Juan FrivaldoNo ratings yet

- Practice 1 - Mgt008Document17 pagesPractice 1 - Mgt008Juan FrivaldoNo ratings yet

- Module 1 Financial PlanningDocument12 pagesModule 1 Financial PlanningJuan FrivaldoNo ratings yet

- Module 5 Fraud - ScamDocument40 pagesModule 5 Fraud - ScamJuan FrivaldoNo ratings yet

- Labor Code of The PhilippinesDocument141 pagesLabor Code of The PhilippinesJuan FrivaldoNo ratings yet

- Module 3 Debt ManagementDocument33 pagesModule 3 Debt ManagementJuan FrivaldoNo ratings yet

- Module 6 Consumer ProtectionDocument16 pagesModule 6 Consumer ProtectionJuan FrivaldoNo ratings yet

- Financial Planning CalculatorDocument8 pagesFinancial Planning CalculatorJuan FrivaldoNo ratings yet

- 6.1 Closing Entries: Name of CompanyDocument2 pages6.1 Closing Entries: Name of CompanyJuan FrivaldoNo ratings yet

- Module 2 Saving BudgetingDocument31 pagesModule 2 Saving BudgetingJuan FrivaldoNo ratings yet

- Cda - Social Audit ReportDocument58 pagesCda - Social Audit ReportJuan FrivaldoNo ratings yet

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- Module Program For BEST Webinar Workshop v2Document5 pagesModule Program For BEST Webinar Workshop v2Juan FrivaldoNo ratings yet

- K-12 Financial Literacy Guide Helps Students Make Smart Money ChoicesDocument55 pagesK-12 Financial Literacy Guide Helps Students Make Smart Money ChoicesJuan Frivaldo100% (1)

- ACT121 - Topic 3Document4 pagesACT121 - Topic 3Juan FrivaldoNo ratings yet

- ACT121 - Topic 2Document2 pagesACT121 - Topic 2Juan FrivaldoNo ratings yet

- 6.1 Closing Entries: Name of CompanyDocument2 pages6.1 Closing Entries: Name of CompanyJuan FrivaldoNo ratings yet

- Chapter 2 Multiple Choice Computational Cost Acc Guerrero 2018 EdDocument14 pagesChapter 2 Multiple Choice Computational Cost Acc Guerrero 2018 EdJuan FrivaldoNo ratings yet

- Acc 35 Managerial Accounting Course Syllabus: Finance & Accounting Department, J. Gokongwei School of ManagementDocument4 pagesAcc 35 Managerial Accounting Course Syllabus: Finance & Accounting Department, J. Gokongwei School of ManagementyaneeNo ratings yet

- Reviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborDocument3 pagesReviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborJuan FrivaldoNo ratings yet

- Schedule and Procedure For The Filing of Annual Financial Statements, General Information Sheet and Other Covered ReportsDocument11 pagesSchedule and Procedure For The Filing of Annual Financial Statements, General Information Sheet and Other Covered ReportsRoderick RiveraNo ratings yet

- Acc 204 Accounting For Overhead by GuererroDocument9 pagesAcc 204 Accounting For Overhead by GuererroJuan FrivaldoNo ratings yet

- 1.1 Definition of Cost Accounting: Alfonso T. Yuchengco College of BusinessDocument3 pages1.1 Definition of Cost Accounting: Alfonso T. Yuchengco College of BusinessJuan FrivaldoNo ratings yet

- Annex D - Sec MC 28-2020Document1 pageAnnex D - Sec MC 28-2020Juan Frivaldo100% (2)

- 2021notice BOTDFDocument1 page2021notice BOTDFvanessa_3No ratings yet

- Registration of Domestic Corporation - SecDocument6 pagesRegistration of Domestic Corporation - SecJuan FrivaldoNo ratings yet

- Applying accounting for income tax on income tax article 21Document11 pagesApplying accounting for income tax on income tax article 21one lismanNo ratings yet

- Paper 6 C Case Studies PDFDocument219 pagesPaper 6 C Case Studies PDFSarvesh SinghNo ratings yet

- This Is To Certify That The Following Payments Have Been Made Under Life Insurance Policies Held byDocument1 pageThis Is To Certify That The Following Payments Have Been Made Under Life Insurance Policies Held byDeepak ShrigadiNo ratings yet

- Reliance Retail LimitedDocument3 pagesReliance Retail LimitedSaiPraneethNo ratings yet

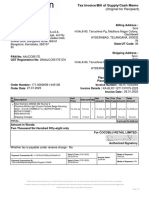

- InvoiceDocument1 pageInvoiceVeerappan MuthuramanNo ratings yet

- Malaysian tax rates and reliefsDocument4 pagesMalaysian tax rates and reliefsJasne OczyNo ratings yet

- Shoes InvoiceDocument1 pageShoes InvoiceSoni PinjalaNo ratings yet

- ERD.2.F.001 - Application For Income Tax HolidayDocument3 pagesERD.2.F.001 - Application For Income Tax Holidayprinces100% (1)

- What Is TCS ?: Transactions Comes Under TCSDocument15 pagesWhat Is TCS ?: Transactions Comes Under TCSMichael WellsNo ratings yet

- Broadband Bill Feb-24Document2 pagesBroadband Bill Feb-24shuja147No ratings yet

- Accounting and Payroll Specialist Study TestDocument1 pageAccounting and Payroll Specialist Study TestSherlyana GunawanNo ratings yet

- CPA Reviewer in Taxation (2022) - Tabag Searchable - CopyDocument628 pagesCPA Reviewer in Taxation (2022) - Tabag Searchable - CopyTOBIT JEHAZIEL SILVESTRENo ratings yet

- Mogli Labs (India) PVT LTD: Tax InvoiceDocument4 pagesMogli Labs (India) PVT LTD: Tax Invoicelucky sharmaNo ratings yet

- Appendix 26 - RCD FormDocument1 pageAppendix 26 - RCD FormRogie Apolo0% (1)

- Tax Invoice for Medical SuppliesDocument1 pageTax Invoice for Medical SuppliesPintu ShahNo ratings yet

- CIR vs. Aichi Forging Company of AsiaDocument27 pagesCIR vs. Aichi Forging Company of AsiaChristle CorpuzNo ratings yet

- CIR vs. British Overseas Airways (BOAC)Document4 pagesCIR vs. British Overseas Airways (BOAC)Arthur John GarratonNo ratings yet

- Answer Key (IDT Model Paper)Document12 pagesAnswer Key (IDT Model Paper)RKSiranjeeviRamanNo ratings yet

- Premium paid certificateDocument1 pagePremium paid certificateBinu Kumar SNo ratings yet

- BL04 - Chapter 9 ModuleDocument8 pagesBL04 - Chapter 9 ModuleAriel A. YusonNo ratings yet

- Godawari Sikshya Bikash Morang PVT LTDDocument1 pageGodawari Sikshya Bikash Morang PVT LTDsarojdawadiNo ratings yet

- Payslip For The Month of Jul 2019: Sterling and Wilson Pvt. LTD 13th Floor, P L Lokhande Marg, Chembur (W)Document1 pagePayslip For The Month of Jul 2019: Sterling and Wilson Pvt. LTD 13th Floor, P L Lokhande Marg, Chembur (W)praveen kumarNo ratings yet

- Week 6 - Introduction To Optimal TaxationDocument26 pagesWeek 6 - Introduction To Optimal TaxationZyra Angela BlasNo ratings yet

- Apply Single Person Council Tax DiscountDocument2 pagesApply Single Person Council Tax DiscountTerry SaundersNo ratings yet

- Residential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inDocument4 pagesResidential Status of Individuals Under Income Tax Act, 1961 - Taxguru - inSimran SinghNo ratings yet

- Lecture On Percentage TaxesDocument4 pagesLecture On Percentage TaxesGlenn AquinoNo ratings yet

- Tax Fraud Session with Eminent SpeakersDocument2 pagesTax Fraud Session with Eminent SpeakersSavyasachiNo ratings yet

- Simple Tax Invoice With Billing and ShippingDocument1 pageSimple Tax Invoice With Billing and ShippingAkbar ShariefNo ratings yet

- CostDocument39 pagesCostJames De Torres CarilloNo ratings yet

- P 58Document1 pageP 58penelopegerhardNo ratings yet