You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Outline (LONG) Real Estate Trans. (Dewey, 2017 Spring)Document52 pagesOutline (LONG) Real Estate Trans. (Dewey, 2017 Spring)Larry Rogers100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- SOP - Purchase DeptDocument42 pagesSOP - Purchase DeptJayant Kumar Jha100% (2)

- Oracle EBS AIM Documents PDFDocument2 pagesOracle EBS AIM Documents PDFVKrishna KilaruNo ratings yet

- Test Bank Accounting For Governmental and Nonprofit Organizations 1st Edition by PattonDocument1 pageTest Bank Accounting For Governmental and Nonprofit Organizations 1st Edition by PattonBob43% (7)

- History of Banking in IndiaDocument15 pagesHistory of Banking in Indiaaccesstariq90% (29)

- Entrepreneurs in IndiaDocument3 pagesEntrepreneurs in IndiaMathangiNo ratings yet

- Unit 4Document44 pagesUnit 4MathangiNo ratings yet

- Top 20 Reasons Startups FailDocument43 pagesTop 20 Reasons Startups FailSaurav ShresthaNo ratings yet

- ManagementofinterestrateriskDocument19 pagesManagementofinterestrateriskMathangiNo ratings yet

- RiskmanagementinbanksDocument18 pagesRiskmanagementinbanksMathangiNo ratings yet

- Banking StructureDocument18 pagesBanking StructureMathangiNo ratings yet

- Banking 130730020756 Phpapp02Document69 pagesBanking 130730020756 Phpapp02shweta shuklaNo ratings yet

- Banking HistoryDocument11 pagesBanking HistoryMathangiNo ratings yet

- Unit 1Document22 pagesUnit 1MathangiNo ratings yet

- Banking Sector ReformsDocument22 pagesBanking Sector ReformsMathangiNo ratings yet

- Group Dynamics Concepts, Formation, and Impact on OrganizationsDocument26 pagesGroup Dynamics Concepts, Formation, and Impact on OrganizationsMathangiNo ratings yet

- Breaking Away The Secrets To Scaling AnalyticsDocument11 pagesBreaking Away The Secrets To Scaling AnalyticsMathangiNo ratings yet

- Kaspersky Business Space Security antivirus software license price offerDocument3 pagesKaspersky Business Space Security antivirus software license price offerShafiqul Islam LilyNo ratings yet

- Ece TrainingDocument95 pagesEce TrainingAyush MittalNo ratings yet

- Balance SheetDocument1 pageBalance Sheetdhuvad.2004No ratings yet

- PC1 JozaraDocument40 pagesPC1 JozaraFarhat Durrani0% (1)

- Managment Project On Warid Telecom by Usman PirzadaDocument46 pagesManagment Project On Warid Telecom by Usman PirzadaUsman100% (2)

- AprilDocument15 pagesAprilanil khannaNo ratings yet

- Technology & Innovation Centre: Closing The Gap Between Concept and CommercialisationDocument22 pagesTechnology & Innovation Centre: Closing The Gap Between Concept and CommercialisationCreativeFrontNo ratings yet

- Supra Case StudyDocument26 pagesSupra Case StudyZubair Nawaz0% (1)

- Business Planning OverviewDocument16 pagesBusiness Planning OverviewAgun GunawanNo ratings yet

- Service Crew- Dining Crew- CashierDocument22 pagesService Crew- Dining Crew- CashierThatha CabatoNo ratings yet

- Strategic Analysis of NEXT PLCDocument13 pagesStrategic Analysis of NEXT PLCcoursehero1218No ratings yet

- Name: Kuna Satya Srinivasa Raju ROLL NO:200914006 (CEM) Project Management Lab-2 Assignment No - 6Document14 pagesName: Kuna Satya Srinivasa Raju ROLL NO:200914006 (CEM) Project Management Lab-2 Assignment No - 6Srinivasa RajuNo ratings yet

- 2011 Sept26 No491 Ca TheedgesporeDocument20 pages2011 Sept26 No491 Ca TheedgesporeThe Edge SingaporeNo ratings yet

- Starbucks Corporation - Situational AnalysisDocument16 pagesStarbucks Corporation - Situational AnalysisRasmus BenderNo ratings yet

- Lit ReviewDocument15 pagesLit Reviewapi-385119016No ratings yet

- Swot AnalysisDocument4 pagesSwot AnalysisMariel TinolNo ratings yet

- Hong Leong Bank Performance A ReviewDocument16 pagesHong Leong Bank Performance A ReviewMohd Helmi100% (2)

- PT Prima Elektronik Journal Entries December 2015Document1 pagePT Prima Elektronik Journal Entries December 2015Syoheh PamujiNo ratings yet

- Isthara Co-Living Facilities in Madhapur & Hi-Tech CityDocument25 pagesIsthara Co-Living Facilities in Madhapur & Hi-Tech CityMainak TarafdarNo ratings yet

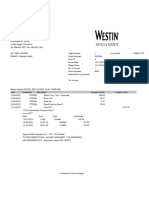

- Westin Hotels & Resorts - 2023-12-10 - 257.78Document2 pagesWestin Hotels & Resorts - 2023-12-10 - 257.78rahul.transcountsNo ratings yet

- Tech MahindraDocument11 pagesTech MahindraLUKESH ankamwar0% (1)

- Pre Placement Talk - HDFC AMC 2011Document18 pagesPre Placement Talk - HDFC AMC 2011Karan_Singh_Ba_6141No ratings yet

- Petition for review of CA decision reversing CTA ruling on tax assessmentsDocument16 pagesPetition for review of CA decision reversing CTA ruling on tax assessmentscarl dianneNo ratings yet

- KeyInitiativeOverview CloudComputingDocument5 pagesKeyInitiativeOverview CloudComputingajay_khandelwalNo ratings yet

- Atswa Cost AccountingDocument504 pagesAtswa Cost AccountingIbrahim MuyeNo ratings yet