You might also like

- Indonesia Digital Transformation Outlook Briefing 2016Document13 pagesIndonesia Digital Transformation Outlook Briefing 2016Ken KurniaNo ratings yet

- Thesis On Baidu IncDocument15 pagesThesis On Baidu IncCheka 110No ratings yet

- Together We Can- Transsion MI Game Intermodal Cooperation Program20231008EN-FinalDocument30 pagesTogether We Can- Transsion MI Game Intermodal Cooperation Program20231008EN-FinalTaskir's viewNo ratings yet

- KH 2016 June Investing in Cambodia PDFDocument40 pagesKH 2016 June Investing in Cambodia PDFToan LuongkimNo ratings yet

- Thesis On Alibaba GroupDocument16 pagesThesis On Alibaba GroupCheka 110No ratings yet

- Client: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDocument8 pagesClient: Taiwan Semiconductor Manufacturing Co., Ltd. (NYSE: TSM / TSE: 2330) Auditor: Deloitte (1) Understanding of The ClientDuong Trinh MinhNo ratings yet

- TSMC Audit RisksDocument5 pagesTSMC Audit RisksDuong Trinh MinhNo ratings yet

- Session 1 Embracing The Ecommerce Revolution Jong Woo KangDocument25 pagesSession 1 Embracing The Ecommerce Revolution Jong Woo KangNaazir jemaNo ratings yet

- 2C2P-IDC-InfoBrief AP241267IB Final SmallDocument17 pages2C2P-IDC-InfoBrief AP241267IB Final Smalljefcheung19No ratings yet

- Case Study: Season 2Document5 pagesCase Study: Season 2Manjit KalgutkarNo ratings yet

- E-Commerce: 27% CAGR and Expected To ReachDocument12 pagesE-Commerce: 27% CAGR and Expected To ReachNAMIT GADGENo ratings yet

- Banking: CHAPTER A: Brief About The Indian Banking SectorDocument63 pagesBanking: CHAPTER A: Brief About The Indian Banking SectorDevang ParabNo ratings yet

- Food Services Industry Update June 2021Document4 pagesFood Services Industry Update June 2021Dipti RavariaNo ratings yet

- Block Chain Valley DeckDocument26 pagesBlock Chain Valley DeckBlockchain LandNo ratings yet

- E Retail Market Size To Rise 2dot5x in 3 YearsDocument7 pagesE Retail Market Size To Rise 2dot5x in 3 YearsChristopher RajNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- The Last Mile Logistics Whitepaper, 2018Document21 pagesThe Last Mile Logistics Whitepaper, 2018Hachem FartoutNo ratings yet

- Choice IntroductionDocument22 pagesChoice IntroductionMonu SinghNo ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Aid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentFrom EverandAid for Trade in Asia and the Pacific: Promoting Connectivity for Inclusive DevelopmentNo ratings yet

- BWR MicrofinanceReport FinalDocument13 pagesBWR MicrofinanceReport FinalHarsh KumarNo ratings yet

- BCG Ten Things You Should Know About e Commerce in India Jun 2022Document24 pagesBCG Ten Things You Should Know About e Commerce in India Jun 2022Shilpi MehrotraNo ratings yet

- GroupmecommerceforecastDocument7 pagesGroupmecommerceforecastDaria BNo ratings yet

- Executive Summary: Click To Add Text Click To Add TextDocument11 pagesExecutive Summary: Click To Add Text Click To Add Textteam5DTCMNo ratings yet

- Gestion-Ecommerce-Marketplaces OKDocument121 pagesGestion-Ecommerce-Marketplaces OKCarlos Samper BaidezNo ratings yet

- ROBOGlobalLogisticsAutomation FinalDocument18 pagesROBOGlobalLogisticsAutomation FinalRujan Mihnea MarianNo ratings yet

- Indian Beer Industry: Social Media &Document29 pagesIndian Beer Industry: Social Media &neelsterNo ratings yet

- Research Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedDocument16 pagesResearch Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedTanu SinghNo ratings yet

- Marketing 100 Days Plan: Indonesia Philippines Malaysia Thailand SingaporeDocument34 pagesMarketing 100 Days Plan: Indonesia Philippines Malaysia Thailand SingaporeLinh GT GTNo ratings yet

- Fin 4150 Week 8 LecturesDocument46 pagesFin 4150 Week 8 LecturesEric McLaughlinNo ratings yet

- IT Services - Analyst Presentation - Sep15Document15 pagesIT Services - Analyst Presentation - Sep15Nimish NamaNo ratings yet

- Insights Digital CurrencyDocument13 pagesInsights Digital CurrencyknwongabNo ratings yet

- Chinaperspectives 7423Document7 pagesChinaperspectives 7423Gebakken KibbelingNo ratings yet

- 2020.12 - MobilityDocument52 pages2020.12 - MobilityYannick Martineau GoupilNo ratings yet

- White Star Capital 2020 Global Mobility ReportDocument52 pagesWhite Star Capital 2020 Global Mobility ReportWhite Star CapitalNo ratings yet

- China E-Commerce Platforms Who Will Make Money in Lower-Tier CitiesDocument54 pagesChina E-Commerce Platforms Who Will Make Money in Lower-Tier CitiesBrandon TanNo ratings yet

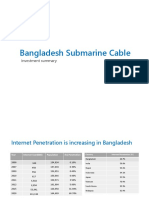

- Bangladesh Submarine Cable (Investment Summary)Document21 pagesBangladesh Submarine Cable (Investment Summary)hossainboxNo ratings yet

- Philippines As An Investment Destination For Infrastructure ProjectsDocument21 pagesPhilippines As An Investment Destination For Infrastructure ProjectsPTIC LondonNo ratings yet

- A Project Proposal From Bangladesh: Strengthening ICT and Telecom Sector in Bangladesh (STIB)Document21 pagesA Project Proposal From Bangladesh: Strengthening ICT and Telecom Sector in Bangladesh (STIB)Rabbir AhmedNo ratings yet

- Somalia Trade Statistics 2010-2018Document7 pagesSomalia Trade Statistics 2010-2018Abdullahi mohamed AbdirisakNo ratings yet

- Italy's Macroeconomic OverviewDocument19 pagesItaly's Macroeconomic OverviewSatvikNo ratings yet

- E-Commerce and Taobao Villages: News AnalysisDocument6 pagesE-Commerce and Taobao Villages: News AnalysisDiggerNo ratings yet

- Q1 2021 E Commerce ReportDocument6 pagesQ1 2021 E Commerce ReportEstefania HernandezNo ratings yet

- Strategic Report of United BreweriesDocument29 pagesStrategic Report of United BreweriesaashuchattNo ratings yet

- FAS Survey Marks a Decade of Tracking Global Financial AccessDocument8 pagesFAS Survey Marks a Decade of Tracking Global Financial AccessAndjenie RamautarNo ratings yet

- 1 - Decoding Digital Retail (India)Document36 pages1 - Decoding Digital Retail (India)Kaushal Shah100% (1)

- 2017 Budget-Country Presentation FormatDocument59 pages2017 Budget-Country Presentation FormatYhane Hermann BackNo ratings yet

- Aviation Connects and Unites Us!: Airbus Global Market Forecast 2021 - 2040Document23 pagesAviation Connects and Unites Us!: Airbus Global Market Forecast 2021 - 2040Samy P.GNo ratings yet

- E-Commerce y Sus DatosDocument3 pagesE-Commerce y Sus DatosAngie Camila Valladares FernandezNo ratings yet

- Digital Economy: Submitted By: Name: Justin Joy Kakashary Reg - No: 21MCMR105Document24 pagesDigital Economy: Submitted By: Name: Justin Joy Kakashary Reg - No: 21MCMR105justin joyNo ratings yet

- Manthan Report - Retail SectorDocument23 pagesManthan Report - Retail SectorAtul sharmaNo ratings yet

- TSMG Tata Review-June 2006Document5 pagesTSMG Tata Review-June 2006dipangshu12No ratings yet

- Session 8-4: Financial Education in The Digital Age Experience From Viet Nam by Dinh Thi Thanh VanDocument21 pagesSession 8-4: Financial Education in The Digital Age Experience From Viet Nam by Dinh Thi Thanh VanADBI EventsNo ratings yet

- Chiang Mai Hotel Market Update 2017 03Document4 pagesChiang Mai Hotel Market Update 2017 03Oon KooNo ratings yet

- Project5 - Vishnu Vamsi Koye-1Document5 pagesProject5 - Vishnu Vamsi Koye-1Vishnu VamsiNo ratings yet

- Revised Emerging Indian Mid-Market Hotel Opportunity 20-03-2007Document4 pagesRevised Emerging Indian Mid-Market Hotel Opportunity 20-03-2007Viraj MulkiNo ratings yet

- The Complete Guide to E-Commerce in the Online Food Delivery IndustryDocument9 pagesThe Complete Guide to E-Commerce in the Online Food Delivery IndustryHari HaranNo ratings yet

- CDI ASEAN-Retail May2015-EN PDFDocument4 pagesCDI ASEAN-Retail May2015-EN PDFMohd Farid Mohd NorNo ratings yet

- Indonesia's Booming Startup Ecosystem in 2018Document35 pagesIndonesia's Booming Startup Ecosystem in 2018benyhartoNo ratings yet

- Exporting Services: A Developing Country PerspectiveFrom EverandExporting Services: A Developing Country PerspectiveRating: 5 out of 5 stars5/5 (2)

- Training SeminarDocument8 pagesTraining SeminarMukul RaghavNo ratings yet

- Document Submission Requirements by Applicant TypeDocument5 pagesDocument Submission Requirements by Applicant TypeMukul RaghavNo ratings yet

- Statistical Process Control: SKF EdDocument21 pagesStatistical Process Control: SKF EdMukul RaghavNo ratings yet

- Your Own Group Discussion Handbook HRCREST Release 2012Document23 pagesYour Own Group Discussion Handbook HRCREST Release 2012vikasfincapNo ratings yet

- 300 Antonyms QuestionsDocument15 pages300 Antonyms QuestionsAditya RamNo ratings yet

- InTech-Poisson S Ratio and Mechanical Nonlinearity Under Tensile Deformation in Crystalline PolymersDocument21 pagesInTech-Poisson S Ratio and Mechanical Nonlinearity Under Tensile Deformation in Crystalline PolymersMukul RaghavNo ratings yet

- Tata Steel Cold Formed Sections Product RAngeDocument36 pagesTata Steel Cold Formed Sections Product RAngesudhansu_777No ratings yet

- Meshing 3DSolids CAEA 2Document16 pagesMeshing 3DSolids CAEA 2Mukul RaghavNo ratings yet

- 175Document31 pages175Mukul RaghavNo ratings yet

- GRE AntonymsDocument96 pagesGRE AntonymsmahamnadirminhasNo ratings yet

- Experimental Design, Response Surface Analysis, and OptimizationDocument24 pagesExperimental Design, Response Surface Analysis, and OptimizationMukul RaghavNo ratings yet

- Rau's IAS Study GuideDocument162 pagesRau's IAS Study Guideapi-3710029100% (1)

- Fenet d3602 Pso Doe and RsaDocument5 pagesFenet d3602 Pso Doe and RsaMukul RaghavNo ratings yet

- Cash2013 - Highly Scalable Searchable Symmetric Encryption With Support For Boolean QueriesDocument21 pagesCash2013 - Highly Scalable Searchable Symmetric Encryption With Support For Boolean QueriesYuang PengNo ratings yet

- Asterisk Installation On Centos 5Document3 pagesAsterisk Installation On Centos 5kumargupt117No ratings yet

- Lecture 4 - Process - CPU SchedulingDocument38 pagesLecture 4 - Process - CPU SchedulingtalentNo ratings yet

- MRx01B Power M0079a1aDocument81 pagesMRx01B Power M0079a1aLuis CarmoNo ratings yet

- Charles H. Cox III Analog Optical Links Theory and Practice Cambridge Studies in Modern OpDocument303 pagesCharles H. Cox III Analog Optical Links Theory and Practice Cambridge Studies in Modern OpAG Octavio100% (1)

- EasyEDA-Std-Tutorial - v6 5 22Document427 pagesEasyEDA-Std-Tutorial - v6 5 22Frédéric QuérinjeanNo ratings yet

- Dhaval Patel Ccna Rectify FaultsDocument12 pagesDhaval Patel Ccna Rectify FaultsDhaval PatelNo ratings yet

- The Impact of Technology-Enhanced Language Learning On English Proficiency: A Comparative Study of Digital Tools and Traditional MethodsDocument3 pagesThe Impact of Technology-Enhanced Language Learning On English Proficiency: A Comparative Study of Digital Tools and Traditional MethodsMamta AgarwalNo ratings yet

- 1 - ADITYA Project ReportDocument42 pages1 - ADITYA Project ReportMonty SharmaNo ratings yet

- Bosch Bulding Technologies Academy - Training Catalog 2024Document55 pagesBosch Bulding Technologies Academy - Training Catalog 2024erc001No ratings yet

- Application Software Installation - Lesson PlanDocument3 pagesApplication Software Installation - Lesson PlanLeo Loven Lumacang100% (9)

- Modern Work Plan Comparison EnterpriseDocument10 pagesModern Work Plan Comparison EnterpriseRicardo SilvaNo ratings yet

- OB Module 1Document5 pagesOB Module 1Pramod K LaxmanNo ratings yet

- Export To Excel PDFDocument2 pagesExport To Excel PDFFernando SandovalNo ratings yet

- TCLDocument13 pagesTCLYc ChenNo ratings yet

- Shortlist For Ericsson Cloud Technology Elective Online TestDocument14 pagesShortlist For Ericsson Cloud Technology Elective Online TestRounak Roy ChowdhuryNo ratings yet

- Admin Assistant - Job DescriptionDocument2 pagesAdmin Assistant - Job Descriptiontoffee capituloNo ratings yet

- 12th International Conference On Magnesium Alloys and Their Applications (MG 2021) Meyer StoneDocument10 pages12th International Conference On Magnesium Alloys and Their Applications (MG 2021) Meyer Stonea stoneNo ratings yet

- T2397489 RR - 139231029Document3 pagesT2397489 RR - 139231029Ikhtiander IkhtianderNo ratings yet

- 200watt Active Load UnitDocument14 pages200watt Active Load Unitagmnm1962No ratings yet

- AWP Unit 3Document21 pagesAWP Unit 3Darshana RavindraNo ratings yet

- EMAG Marketplace API Documentation v4.2.0Document43 pagesEMAG Marketplace API Documentation v4.2.0David AndreicaNo ratings yet

- Data Guard CheatsheetDocument8 pagesData Guard CheatsheetMohammad Mizanur RahmanNo ratings yet

- Taylor Fischer ResumeDocument2 pagesTaylor Fischer Resumeapi-272531081No ratings yet

- ChecklistDocument1 pageChecklistYahir andres Luna lopezNo ratings yet

- RMS - MVP PDFDocument17 pagesRMS - MVP PDFYOGESH A NNo ratings yet

- Satcon 500 KW Inverter SpecDocument4 pagesSatcon 500 KW Inverter SpecSagar SinghNo ratings yet

- Internet Protocol: DHCP: Dynamic Host Configuration Protocol (DHCP) Is A Protocol Used by NetworkedDocument3 pagesInternet Protocol: DHCP: Dynamic Host Configuration Protocol (DHCP) Is A Protocol Used by NetworkedsamirNo ratings yet

- Pragmatic Play Fun88Document2 pagesPragmatic Play Fun88webfun88th123zNo ratings yet

- DJSCE Placement Report 2014-15Document3 pagesDJSCE Placement Report 2014-15sujeet guptaNo ratings yet