You might also like

- Ultimate Guide To SIP in Pakistan Ebook FinalDocument39 pagesUltimate Guide To SIP in Pakistan Ebook FinalbisaxNo ratings yet

- Sbi Read UpDocument19 pagesSbi Read Upperfection1No ratings yet

- OP Bhatt Interview With CNBCDocument4 pagesOP Bhatt Interview With CNBCAbhai Pratap SinghNo ratings yet

- Creditcard STPDocument13 pagesCreditcard STPapi-3701241No ratings yet

- These Are The Best Long-Term StocksDocument7 pagesThese Are The Best Long-Term StocksPGM5HNo ratings yet

- Literature Review of Sbi BankDocument6 pagesLiterature Review of Sbi Bankeowcnerke100% (1)

- Course Handouts For April 4stDocument5 pagesCourse Handouts For April 4stRama SubramanianNo ratings yet

- SBI PO Interview CapsuleDocument19 pagesSBI PO Interview CapsulevanajaNo ratings yet

- Gautam Baid Q&ADocument9 pagesGautam Baid Q&AFahad SiddiqueeNo ratings yet

- Big BazzarDocument3 pagesBig BazzarcadrjainNo ratings yet

- 12 - 16th September 2008 (160908)Document7 pages12 - 16th September 2008 (160908)Chaanakya_cuimNo ratings yet

- Thesis On Sbi BankDocument4 pagesThesis On Sbi BankSomeoneToWriteMyPaperForMeEvansville100% (2)

- Hidden Treasures and E-Commerce Play: Intrasoft Technologies LTDDocument10 pagesHidden Treasures and E-Commerce Play: Intrasoft Technologies LTDPankaj D. DaniNo ratings yet

- A Report ONDocument68 pagesA Report ONYenkee Adarsh AroraNo ratings yet

- September 2021 Edition: The Institute of Chartered Accountants of IndiaDocument19 pagesSeptember 2021 Edition: The Institute of Chartered Accountants of IndiaKundan ShahiNo ratings yet

- Stock InvestingDocument9 pagesStock InvestingAnant TiwariNo ratings yet

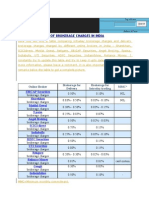

- Investo Blog: Comparison Table of Brokerage Charges in IndiaDocument16 pagesInvesto Blog: Comparison Table of Brokerage Charges in Indiajatin_ahuja03No ratings yet

- Raamdeo Agrawal Interviews (2013-Jun 2018)Document347 pagesRaamdeo Agrawal Interviews (2013-Jun 2018)Nishant JhaNo ratings yet

- Consumers Preference Towards Plastic MoneDocument22 pagesConsumers Preference Towards Plastic Monecharujagwani50% (2)

- 6 - 16th Novmber 2007 (161107)Document5 pages6 - 16th Novmber 2007 (161107)Chaanakya_cuimNo ratings yet

- We LikeDocument45 pagesWe LikeAnand Chavan0% (1)

- FinShiksha - Finance Interview Prep SeriesDocument18 pagesFinShiksha - Finance Interview Prep SeriesLionel MessiNo ratings yet

- Zero To Billions - The Zerodha StoryDocument45 pagesZero To Billions - The Zerodha StoryVacancies ProfessionalsNo ratings yet

- Plastic CardsDocument61 pagesPlastic Cardsritik9rNo ratings yet

- P & SBI C: Roduct Services OF Onsumer PerceptionDocument22 pagesP & SBI C: Roduct Services OF Onsumer PerceptionBoney KewlaniNo ratings yet

- The Tip of Indian Banking Part I To Part 26my ScribdDocument144 pagesThe Tip of Indian Banking Part I To Part 26my ScribdambujchinuNo ratings yet

- Art of Stock Investing Indian Stock MarketDocument10 pagesArt of Stock Investing Indian Stock MarketUmesh Kamath80% (5)

- Scenario of Indian Credit Card IndustryDocument11 pagesScenario of Indian Credit Card IndustryAshish SharmaNo ratings yet

- Vision: ValuesDocument8 pagesVision: ValuesBharatSeerviNo ratings yet

- Ibps Po Interview Capsule-1Document8 pagesIbps Po Interview Capsule-1atingoyal1No ratings yet

- Moneylife 2 October 2014Document68 pagesMoneylife 2 October 2014krishnakumarsistNo ratings yet

- DSIJ3209Document84 pagesDSIJ3209Navin ChandarNo ratings yet

- Mental Accounting: From The Desk of Editor in ChiefDocument4 pagesMental Accounting: From The Desk of Editor in ChiefSoobian AhmedNo ratings yet

- 8 Steps To Select A Stock To Invest in Indian Stock MarketDocument11 pages8 Steps To Select A Stock To Invest in Indian Stock MarketVenkatrao Varagani100% (1)

- Interview Capsule by Bankers AddaDocument38 pagesInterview Capsule by Bankers Addadevendra_tomarNo ratings yet

- GIFT Needs LRS, Rupee ECBDocument7 pagesGIFT Needs LRS, Rupee ECBvijaypal bishnoiNo ratings yet

- Saurabh MukherjeaDocument8 pagesSaurabh MukherjeaGurjeevNo ratings yet

- ICICIDocument2 pagesICICISACCHIDANAND TRIPATHINo ratings yet

- HDFC Bank Vs ICICI Bank - Stock ComparisonDocument43 pagesHDFC Bank Vs ICICI Bank - Stock ComparisonD.G.DNo ratings yet

- Irctc IpoDocument8 pagesIrctc IpoAbhishek PadhyeNo ratings yet

- Market Survey Report On: Study of Account Holders Towards Demat Account in Icici BankDocument20 pagesMarket Survey Report On: Study of Account Holders Towards Demat Account in Icici BankShubham-Theif Of-HeartsNo ratings yet

- How To Create Your BIN ListDocument3 pagesHow To Create Your BIN ListJohn SmithNo ratings yet

- Liquidity and Stock MarketDocument4 pagesLiquidity and Stock MarketIMaths PowaiNo ratings yet

- GD Topics & PI Questions - 2022Document44 pagesGD Topics & PI Questions - 2022Madhav MantriNo ratings yet

- ICICI's Chanda Kochhar: 'Whenever There's A Challenge, I See An Opportunity'Document3 pagesICICI's Chanda Kochhar: 'Whenever There's A Challenge, I See An Opportunity'Mayank GargNo ratings yet

- How To Apply For SBI Green Remit Card OnlineDocument3 pagesHow To Apply For SBI Green Remit Card OnlineThakur sahabNo ratings yet

- Winter Internship Report: Feedback AnalysisDocument49 pagesWinter Internship Report: Feedback AnalysisAnand KothaneNo ratings yet

- Ankur Sing TomarDocument70 pagesAnkur Sing TomarVivek KumarNo ratings yet

- Finance Mirror: A New Buzz in Banking-ImpsDocument3 pagesFinance Mirror: A New Buzz in Banking-Impsaman27jaiswalNo ratings yet

- Baking LeagueDocument5 pagesBaking LeagueJst PrashantNo ratings yet

- Analysis of Merger of SBIDocument5 pagesAnalysis of Merger of SBIAnuja AmiditNo ratings yet

- @@GK Tornado RRB Mains 2017-EnG - pdf-73Document80 pages@@GK Tornado RRB Mains 2017-EnG - pdf-73Shrey YaduNo ratings yet

- Home Loan Literature ReviewDocument8 pagesHome Loan Literature Reviewc5rf85jq100% (1)

- Can India Really Becomes CashlessDocument2 pagesCan India Really Becomes CashlessAnonymous lYNb08No ratings yet

- The Rabbit Hole - Book Summaries by Blas MorosDocument3,019 pagesThe Rabbit Hole - Book Summaries by Blas MorosSudhanshu100% (4)

- Arvind Sir Video 6 - Otter - AiDocument4 pagesArvind Sir Video 6 - Otter - AiGurjeevNo ratings yet

- Arvind Sir Video 5 - Otter - AiDocument6 pagesArvind Sir Video 5 - Otter - AiGurjeevNo ratings yet

- Note 4Document4 pagesNote 4GurjeevNo ratings yet

- Arvind Sir Video 6 - Otter - AiDocument4 pagesArvind Sir Video 6 - Otter - AiGurjeevNo ratings yet

- Note 5Document7 pagesNote 5GurjeevNo ratings yet

- Note 4Document4 pagesNote 4GurjeevNo ratings yet

- Notes (Masterclass With Super-Investors by Vishal Mittal and Saurabh Basrar)Document3 pagesNotes (Masterclass With Super-Investors by Vishal Mittal and Saurabh Basrar)Ajith KumarNo ratings yet

- Note 2Document6 pagesNote 2GurjeevNo ratings yet

- Note 3Document8 pagesNote 3GurjeevNo ratings yet

- Beyond NumbersDocument28 pagesBeyond NumbersGurjeevNo ratings yet

- Appendix A: Putting It All Together: Analysing A ShareDocument18 pagesAppendix A: Putting It All Together: Analysing A ShareGurjeevNo ratings yet

- Note 1Document6 pagesNote 1GurjeevNo ratings yet

- Calculating The Return On Incremental Capital InvestmentsDocument8 pagesCalculating The Return On Incremental Capital InvestmentsGurjeevNo ratings yet

- Scuttlebutt Investor: A Good Metric Is Hard To Find - Return On CapitalDocument20 pagesScuttlebutt Investor: A Good Metric Is Hard To Find - Return On CapitalGurjeevNo ratings yet

- Stock Selection ApproachDocument1 pageStock Selection ApproachGurjeevNo ratings yet

- Wonderla Holidays - Pattern Recognition and Concall Analysis (2Q2020)Document12 pagesWonderla Holidays - Pattern Recognition and Concall Analysis (2Q2020)GurjeevNo ratings yet

- Bajaj Electricals - HaitongDocument12 pagesBajaj Electricals - HaitongGurjeevNo ratings yet

- Importance of ROIC Part 1: Compounders and Cheap Stocks: Update: For Those Interested, I Wrote ADocument7 pagesImportance of ROIC Part 1: Compounders and Cheap Stocks: Update: For Those Interested, I Wrote AGurjeevNo ratings yet

- Investors Earn Handsome PaychecksDocument9 pagesInvestors Earn Handsome PaychecksGurjeevNo ratings yet

- The Great Depression of 1990 - Batra, Raveendra N PDFDocument230 pagesThe Great Depression of 1990 - Batra, Raveendra N PDFGurjeevNo ratings yet

- Equity NoteDocument1 pageEquity NoteGurjeevNo ratings yet

- 10 Years PAt Dorsy PDFDocument32 pages10 Years PAt Dorsy PDFGurjeevNo ratings yet

- IDirect EPCInds NanoNiveshDocument7 pagesIDirect EPCInds NanoNiveshGurjeevNo ratings yet

- File PDFDocument4 pagesFile PDFGurjeevNo ratings yet

- File PDFDocument4 pagesFile PDFGurjeevNo ratings yet

- 00000025-Are You A Learning Machine - FS PDFDocument5 pages00000025-Are You A Learning Machine - FS PDFGurjeevNo ratings yet

- 24th WCS 2019 - by Raamdeo Agrawal PDFDocument56 pages24th WCS 2019 - by Raamdeo Agrawal PDFSY Rshbh KapurNo ratings yet

- Form 10-K405: Duff & Phelps Credit Rating Co - DCRDocument18 pagesForm 10-K405: Duff & Phelps Credit Rating Co - DCRGurjeevNo ratings yet

- Form 10-K405: Duff & Phelps Credit Rating Co - DCRDocument18 pagesForm 10-K405: Duff & Phelps Credit Rating Co - DCRGurjeevNo ratings yet

- The Human and Environmental Cost of Land Business-The Case of Matopiba 030718Document96 pagesThe Human and Environmental Cost of Land Business-The Case of Matopiba 030718Fabricio TelóNo ratings yet

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Document6 pagesPhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)Seth Relian100% (1)

- PARCORDocument14 pagesPARCORChristine DaelNo ratings yet

- FIN 433 - Exam 1 SlidesDocument146 pagesFIN 433 - Exam 1 SlidesNayeem MahmudNo ratings yet

- ASUG - SAP Commodity ManagementDocument41 pagesASUG - SAP Commodity Managementanon_68509251680% (5)

- What Are The Functions, Attributes And, Kinds of MoneyDocument2 pagesWhat Are The Functions, Attributes And, Kinds of MoneyAngelie JalandoniNo ratings yet

- Capital Budgeting Decisions: Accepting Projects That Yields A Return Higher Than The Hurdle RateDocument19 pagesCapital Budgeting Decisions: Accepting Projects That Yields A Return Higher Than The Hurdle RateGaurav JainNo ratings yet

- Exercise in Manaco 2Document2 pagesExercise in Manaco 2Gracelle Mae Oraller100% (1)

- Chapter 13Document13 pagesChapter 13Haseeb Ahmed ShaikhNo ratings yet

- East Cameron Partners The Sukuk BondDocument9 pagesEast Cameron Partners The Sukuk BondAsadNo ratings yet

- Divestiture SDocument26 pagesDivestiture SJoshua JoelNo ratings yet

- The Intelligent Investor Chapter 7Document4 pagesThe Intelligent Investor Chapter 7Michael Pullman100% (1)

- 4.3. Example Scenario - Pro Forma ProblemsDocument6 pages4.3. Example Scenario - Pro Forma Problemskartik lakhotiyaNo ratings yet

- John Hussman Wine Country Conference 2014 VeryMeanReversionDocument36 pagesJohn Hussman Wine Country Conference 2014 VeryMeanReversionJames J Abodeely100% (1)

- Banks Finanl PresentationDocument31 pagesBanks Finanl PresentationADNANE OULKHAJNo ratings yet

- Fixed Vs Flexible Exchange RatesDocument63 pagesFixed Vs Flexible Exchange Ratesramya4smilesNo ratings yet

- Wiley Chapter 11 Depreciation Impairments and DepletionDocument43 pagesWiley Chapter 11 Depreciation Impairments and Depletion靳雪娇No ratings yet

- Meaning of LeasingDocument12 pagesMeaning of LeasingSidhant kumarNo ratings yet

- 2point2 Capital - Investor Update Q1 FY22Document6 pages2point2 Capital - Investor Update Q1 FY22Anil GowdaNo ratings yet

- 1 An Introduction Investing and ValuationDocument19 pages1 An Introduction Investing and ValuationEmmeline ASNo ratings yet

- Lecture 1A Introduction and Understanding Cash FlowsDocument20 pagesLecture 1A Introduction and Understanding Cash FlowsJohnNo ratings yet

- Hiroki Sato, JERA Co. Inc.Document9 pagesHiroki Sato, JERA Co. Inc.Irsyad Saiful M.No ratings yet

- 20-Rules IBDDocument22 pages20-Rules IBDOJ100% (6)

- Rpp04-Real Estate Investment and Appraisal 2018-3-1Document5 pagesRpp04-Real Estate Investment and Appraisal 2018-3-1jcobNo ratings yet

- Week 10 12. ULO B. Substantive Test of InvestmentsDocument13 pagesWeek 10 12. ULO B. Substantive Test of InvestmentskrizmyrelatadoNo ratings yet

- National University of Science and TechnologyDocument5 pagesNational University of Science and TechnologyPATIENCE MUSHONGANo ratings yet

- Phân Tích Tài Chính Pepsi Vs Coca-ColaDocument49 pagesPhân Tích Tài Chính Pepsi Vs Coca-ColaLập PhanNo ratings yet

- BNP Paribas CIB Investor DayDocument154 pagesBNP Paribas CIB Investor DayforabusingNo ratings yet

- Ventura ProjectDocument75 pagesVentura ProjectbasavarajNo ratings yet