You might also like

- Chapter 4 (Elasticity) - Week5Document40 pagesChapter 4 (Elasticity) - Week5Nency MosesNo ratings yet

- (3 Day) The 7 Steps To Becoming A Super AffiliateDocument15 pages(3 Day) The 7 Steps To Becoming A Super AffiliateGAMING AND TECH ZONE67% (3)

- India's Sectoral Valuation Study: Historical Absolute Levels Vs Normalized Levels January 25, 2018Document27 pagesIndia's Sectoral Valuation Study: Historical Absolute Levels Vs Normalized Levels January 25, 2018brijsingNo ratings yet

- MKT406 Assignment 1Document2 pagesMKT406 Assignment 1Neha ReddyNo ratings yet

- Is Management Compensation Rewarding The Right Behavior?Document4 pagesIs Management Compensation Rewarding The Right Behavior?/jncjdncjdnNo ratings yet

- M Strong Gets StongerDocument8 pagesM Strong Gets Stongerzchendc000518No ratings yet

- Mosaic Global PerspectivesDocument14 pagesMosaic Global PerspectivesKevin A. Lenox, CFANo ratings yet

- Management Meet Takeaways: Not RatedDocument8 pagesManagement Meet Takeaways: Not RatedAngel BrokingNo ratings yet

- Market Expectation Is Too HighDocument17 pagesMarket Expectation Is Too Highzchendc000518No ratings yet

- Nyse Hon 2018Document121 pagesNyse Hon 2018girish_patkiNo ratings yet

- Infosys (INFTEC) : Solid Beat Spoiled by Soft GuidanceDocument11 pagesInfosys (INFTEC) : Solid Beat Spoiled by Soft GuidanceumaganNo ratings yet

- Comptel Company Report 2016 Inderes OyDocument36 pagesComptel Company Report 2016 Inderes OySunil KumarNo ratings yet

- Modeling Peak ProfitabiliytDocument23 pagesModeling Peak ProfitabiliytBrentjaciow100% (1)

- Profits in Line With Estimates, Positives Begin To Sprout But Threats RemainDocument8 pagesProfits in Line With Estimates, Positives Begin To Sprout But Threats Remainherrewt rewterwNo ratings yet

- May 18, 2018 - Investor Day Slide PresentationDocument34 pagesMay 18, 2018 - Investor Day Slide Presentationbillroberts981No ratings yet

- Ronw Roce Fixed Assest T.ODocument45 pagesRonw Roce Fixed Assest T.Ofbk4sureNo ratings yet

- KPIT TechnologyDocument41 pagesKPIT Technologysanjayrathi457No ratings yet

- Dupont AnalysisDocument3 pagesDupont AnalysisKarthik RanganathanNo ratings yet

- BetterInvesting Weekly Stock Screen 4-9-18Document1 pageBetterInvesting Weekly Stock Screen 4-9-18BetterInvestingNo ratings yet

- Ings BHD RR 3Q FY2012Document6 pagesIngs BHD RR 3Q FY2012Lionel TanNo ratings yet

- Honeywell InternationalDocument121 pagesHoneywell InternationalDhroov SharmaNo ratings yet

- Elliotts Letter To ATT 09092019Document23 pagesElliotts Letter To ATT 09092019Zerohedge100% (3)

- BetterInvesting Weekly Stock Screen 1-22-18Document1 pageBetterInvesting Weekly Stock Screen 1-22-18BetterInvestingNo ratings yet

- Core Income Down 3.2% in 2Q18, Behind Both COL and Consensus EstimatesDocument8 pagesCore Income Down 3.2% in 2Q18, Behind Both COL and Consensus EstimatesheheheheNo ratings yet

- 2018 08 01 PH e Urc - 2 PDFDocument8 pages2018 08 01 PH e Urc - 2 PDFherrewt rewterwNo ratings yet

- Century Pacific Food: 1Q19: Tempered Opex Buoys MarginsDocument9 pagesCentury Pacific Food: 1Q19: Tempered Opex Buoys MarginsManjit Kour SinghNo ratings yet

- Apple Report by Jason Harris and Neel Munot 042616 PDFDocument11 pagesApple Report by Jason Harris and Neel Munot 042616 PDFusaid khanNo ratings yet

- Asian Paints: Performance HighlightsDocument10 pagesAsian Paints: Performance HighlightsAngel BrokingNo ratings yet

- Value DriversDocument28 pagesValue DriversAbhishek SachdevaNo ratings yet

- Financial Analysis Project FinishedDocument33 pagesFinancial Analysis Project Finishedapi-312209549No ratings yet

- Infosys (INFTEC) : Couldn't Ask For MoreDocument12 pagesInfosys (INFTEC) : Couldn't Ask For MoreumaganNo ratings yet

- France Telecom: Morgan Stanley TMT ConferenceDocument13 pagesFrance Telecom: Morgan Stanley TMT Conferenceshahid10No ratings yet

- 3Q18 Earnings Improve Sequentially But A Sustainable Recovery Is Still UnsureDocument8 pages3Q18 Earnings Improve Sequentially But A Sustainable Recovery Is Still Unsureherrewt rewterwNo ratings yet

- Infosys Ltd-Q2 FY12Document4 pagesInfosys Ltd-Q2 FY12Seema GusainNo ratings yet

- KeppelT&T - 2010 Annual ReportDocument144 pagesKeppelT&T - 2010 Annual ReportDaxx83No ratings yet

- Valuationtemplatev6 0Document47 pagesValuationtemplatev6 0Quofi SeliNo ratings yet

- Fortinet 01Document7 pagesFortinet 01Pedro PabloNo ratings yet

- Legacy Business: Flu 2008A 2009A 2010A 2011A 2012ADocument5 pagesLegacy Business: Flu 2008A 2009A 2010A 2011A 2012Amunger649No ratings yet

- Eclerx Research ReportDocument13 pagesEclerx Research ReportPragati ChaudharyNo ratings yet

- The Balance of Payments: Speech Given by DR Martin WealeDocument14 pagesThe Balance of Payments: Speech Given by DR Martin WealeImamjafar SiddiqNo ratings yet

- 3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina CorporationDocument8 pages3Q17 Net Income Down 39.2% Y/y, Outlook Remains Poor: Universal Robina Corporationherrewt rewterwNo ratings yet

- Britannia: Performance HighlightsDocument11 pagesBritannia: Performance HighlightsAngel BrokingNo ratings yet

- Finolex Cables-Initiating Coverage 22 Apr 2014Document9 pagesFinolex Cables-Initiating Coverage 22 Apr 2014sanjeevpandaNo ratings yet

- Asian Paints - ER ReportDocument11 pagesAsian Paints - ER Reportjainpratik092No ratings yet

- Financial Analysis (Detail)Document68 pagesFinancial Analysis (Detail)Paulo NascimentoNo ratings yet

- YHOO Q410EarningsPresentation FinalDocument25 pagesYHOO Q410EarningsPresentation FinalJay YarowNo ratings yet

- Valuationtemplatev6 0Document66 pagesValuationtemplatev6 0nschanderNo ratings yet

- Faze Three Initial (HDFC)Document11 pagesFaze Three Initial (HDFC)beza manojNo ratings yet

- HP Corp Overview 2010Document6 pagesHP Corp Overview 2010Paul BatesNo ratings yet

- BetterInvesting Weekly Stock Screen 2-10-14Document1 pageBetterInvesting Weekly Stock Screen 2-10-14BetterInvestingNo ratings yet

- Sharekhan Top PicksDocument7 pagesSharekhan Top PicksLaharii MerugumallaNo ratings yet

- Global Payments 2016Document44 pagesGlobal Payments 2016Sayali SinghiNo ratings yet

- TemenosDocument13 pagesTemenosthejerry11No ratings yet

- Delarue ErDocument98 pagesDelarue ErShawn PantophletNo ratings yet

- Tesco Corporation: Company ProfileDocument10 pagesTesco Corporation: Company Profileaaaaa53No ratings yet

- Vglu Ngine: Strong Buy BUYDocument5 pagesVglu Ngine: Strong Buy BUYValuEngine.comNo ratings yet

- Asian Paints Result UpdatedDocument10 pagesAsian Paints Result UpdatedAngel BrokingNo ratings yet

- My First Investment Note - Talwalkars 31 March 2014Document30 pagesMy First Investment Note - Talwalkars 31 March 2014Anonymous o3Z9JvNo ratings yet

- HCL Technologies Q3FY11 Result UpdateDocument4 pagesHCL Technologies Q3FY11 Result Updaterajarun85No ratings yet

- Telephone Answering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandTelephone Answering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Total Value Optimization: Transforming Your Global Supply Chain Into a Competitive WeaponFrom EverandTotal Value Optimization: Transforming Your Global Supply Chain Into a Competitive WeaponNo ratings yet

- Loose Coarse Pitch Worms & Worm Gearing World Summary: Market Sector Values & Financials by CountryFrom EverandLoose Coarse Pitch Worms & Worm Gearing World Summary: Market Sector Values & Financials by CountryNo ratings yet

- TIC Outlook 2018: Trends and Prospects in The Testing, Inspection and Certification SectorDocument11 pagesTIC Outlook 2018: Trends and Prospects in The Testing, Inspection and Certification SectorMohamed SalahNo ratings yet

- Revised Marketing PlanDocument33 pagesRevised Marketing PlanMohamed SalahNo ratings yet

- Novel Coronavirus (Sars-Cov-2) Antibody (Igm / Igg) TestDocument29 pagesNovel Coronavirus (Sars-Cov-2) Antibody (Igm / Igg) TestMohamed SalahNo ratings yet

- Compac MarbleDocument40 pagesCompac MarbleMohamed SalahNo ratings yet

- Published On 24 March 2020: Points 4, 6, 7 and 8 Were AmendedDocument5 pagesPublished On 24 March 2020: Points 4, 6, 7 and 8 Were AmendedMohamed SalahNo ratings yet

- Main CatalogueDocument10 pagesMain CatalogueMohamed SalahNo ratings yet

- 3 Anders SouzaMonteiro Rouviere FINALDocument26 pages3 Anders SouzaMonteiro Rouviere FINALMohamed SalahNo ratings yet

- InvestorDays Market VDEFDocument18 pagesInvestorDays Market VDEFMohamed SalahNo ratings yet

- Juthathip Thanatawee: ObjectiveDocument6 pagesJuthathip Thanatawee: ObjectiveMohamed SalahNo ratings yet

- LEDS Product SheetDocument4 pagesLEDS Product SheetMohamed SalahNo ratings yet

- 2010 Natural Stone EU Market SurveyDocument40 pages2010 Natural Stone EU Market SurveyMohamed SalahNo ratings yet

- Kigali Amendment To The Montreal Protocol: HFC Phase DownDocument2 pagesKigali Amendment To The Montreal Protocol: HFC Phase DownPaulin PahNo ratings yet

- FBL1N GuidelinesDocument29 pagesFBL1N GuidelinesvikramNo ratings yet

- Islamic Banking MidDocument24 pagesIslamic Banking MidRomeshaNo ratings yet

- Exercises Differential Cost Analysis Relevant CostingDocument5 pagesExercises Differential Cost Analysis Relevant CostingBSIT 1A Yancy CaliganNo ratings yet

- CC5051 Database Coursework GuidelinesDocument7 pagesCC5051 Database Coursework GuidelinesSonima SthaNo ratings yet

- What Is Organic Farming?: Govardhan Eco VillageDocument4 pagesWhat Is Organic Farming?: Govardhan Eco VillageprabhuasbNo ratings yet

- Compliance With Anti-Corruption Laws Sample ClausesDocument4 pagesCompliance With Anti-Corruption Laws Sample ClausesRAJARAJESHWARI M GNo ratings yet

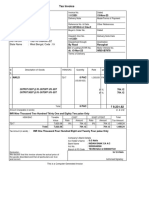

- Tax Invoice: 34 Rath Danga Road Ranaghat Gstin/Uin: 19BYRPS9845M1ZZ State Name: West Bengal, Code: 19Document1 pageTax Invoice: 34 Rath Danga Road Ranaghat Gstin/Uin: 19BYRPS9845M1ZZ State Name: West Bengal, Code: 19Online tally guideNo ratings yet

- Lme Daily Official and Settlement Prices: Lme Copper Grade A $Usd/Tonne Mar-11Document33 pagesLme Daily Official and Settlement Prices: Lme Copper Grade A $Usd/Tonne Mar-11Sakib DarNo ratings yet

- Project On Organisational Study at Leela Kempinski Kovalam Beach ResortDocument57 pagesProject On Organisational Study at Leela Kempinski Kovalam Beach Resortkareemkhan17067% (12)

- Rabia - Research Methods - BA60082O - A1Document13 pagesRabia - Research Methods - BA60082O - A1adhora.zebinNo ratings yet

- Capital Structure Decisions in Financial ManagementDocument52 pagesCapital Structure Decisions in Financial ManagementAnkit LakhaniNo ratings yet

- Marketing Strategy of Maruti Suzuki India Limited: Dr. Rahat KarimDocument6 pagesMarketing Strategy of Maruti Suzuki India Limited: Dr. Rahat KarimRithik Reddy KothwalNo ratings yet

- (1929) 42 CLR 384Document37 pages(1929) 42 CLR 384Joshua ChanNo ratings yet

- SAM Pillar 1: Requirements For Solo Insurers and Insurance GroupsDocument25 pagesSAM Pillar 1: Requirements For Solo Insurers and Insurance GroupsGrahamNo ratings yet

- 2024W MGAC01 CPA Handbook Exercise 2 Q OnlyDocument7 pages2024W MGAC01 CPA Handbook Exercise 2 Q OnlyselyanmakhloufNo ratings yet

- U74999ka2016plc095986 1692355741083Document17 pagesU74999ka2016plc095986 1692355741083jwalan MartinNo ratings yet

- Intellectual Property RightsDocument11 pagesIntellectual Property RightssridharchandrasekarNo ratings yet

- Formulation of Project ReportDocument4 pagesFormulation of Project Reportarmailgm100% (1)

- Chapter 01 - An Overview of Organizational Behavior: Answer: TrueDocument26 pagesChapter 01 - An Overview of Organizational Behavior: Answer: TrueRey Joyce AbuelNo ratings yet

- ICQEM Design Thinking and QFD - Journal ArticleDocument14 pagesICQEM Design Thinking and QFD - Journal Articlelavanya.channelingNo ratings yet

- BAJAJ (MA Presentation)Document25 pagesBAJAJ (MA Presentation)Priyanshu SharmaNo ratings yet

- BNM Takaful Operational Framework 2019Document29 pagesBNM Takaful Operational Framework 2019YEW OI THIMNo ratings yet

- Shaft or DeclineDocument10 pagesShaft or DeclineTamani MoyoNo ratings yet

- Asset ValuationDocument20 pagesAsset Valuationharley_quinn11No ratings yet

- VAT LetterDocument2 pagesVAT Letterrhea CabillanNo ratings yet

- PLI RPLI Questionair CPC SO BODocument10 pagesPLI RPLI Questionair CPC SO BONarayanaNo ratings yet