You might also like

- Sol. Man. - Chapter 8 Leases Part 2Document9 pagesSol. Man. - Chapter 8 Leases Part 2Miguel Amihan100% (1)

- Powers of The CorporationDocument7 pagesPowers of The CorporationMon RamNo ratings yet

- Sol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionDocument34 pagesSol. Man. Chapter 10 Investments in Debt Securities Ia Part 1a 2020 EditionMizza Moreno Cantila100% (1)

- Chapter 9 Financial Reporting in Hyperinflationary EconomiesDocument10 pagesChapter 9 Financial Reporting in Hyperinflationary EconomiesKathrina RoxasNo ratings yet

- Bill Hayton - Vietnam - Rising Dragon-Yale University Press (2010)Document273 pagesBill Hayton - Vietnam - Rising Dragon-Yale University Press (2010)Toan Tran100% (1)

- Principles, TooLs and TechniquesDocument13 pagesPrinciples, TooLs and TechniquesYen Yen77% (101)

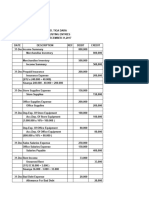

- Problem 10-1 Problem 10-2Document13 pagesProblem 10-1 Problem 10-2Yen YenNo ratings yet

- Chapter 19 20Document11 pagesChapter 19 20Kyle Francine BoloNo ratings yet

- Audience Theories NewDocument11 pagesAudience Theories NewYen YenNo ratings yet

- Chapter16 BuenaventuraDocument11 pagesChapter16 BuenaventuraAnonn100% (1)

- Chap14 ProblemsDocument8 pagesChap14 ProblemsYen YenNo ratings yet

- Chapter19 BuenaventuraIntermediate Accounting1Document13 pagesChapter19 BuenaventuraIntermediate Accounting1AnonnNo ratings yet

- Chapter 19Document9 pagesChapter 19GONZALES, MICA ANGEL A.No ratings yet

- Problem 14-1: Bonds As Trading 2005Document18 pagesProblem 14-1: Bonds As Trading 2005Yen YenNo ratings yet

- Ap1 02Document22 pagesAp1 02EricaNo ratings yet

- Steven Dave OñasDocument6 pagesSteven Dave OñasnenzzmariaNo ratings yet

- Solution:: Investments: Problem 6: For Classroom DiscussionDocument21 pagesSolution:: Investments: Problem 6: For Classroom DiscussionMarie Frances SaysonNo ratings yet

- Final F09 SolutionDocument5 pagesFinal F09 SolutionWyatt Niblett-wilsonNo ratings yet

- 18 PROBLEMS - AND - ANSWERS - FINANCIAL - ASSET - AT - AMORTIZED - COST - Bond - Investment - VERSION - 2.0Document21 pages18 PROBLEMS - AND - ANSWERS - FINANCIAL - ASSET - AT - AMORTIZED - COST - Bond - Investment - VERSION - 2.0Sheila Grace BajaNo ratings yet

- Problem 5-3 Requirement 1 2020Document7 pagesProblem 5-3 Requirement 1 2020Adyagila Ecarg NelehNo ratings yet

- Exercise 1.1: Downpayment Present Value of Note (200,000 X 3.17 Pvoa) Total CostDocument5 pagesExercise 1.1: Downpayment Present Value of Note (200,000 X 3.17 Pvoa) Total CostKailah CalinogNo ratings yet

- Laudit - 8 1,8 2Document3 pagesLaudit - 8 1,8 2Gilbert MoralesNo ratings yet

- Chapter15 BuenaventuraDocument10 pagesChapter15 BuenaventuraAnonnNo ratings yet

- ACC106 Notes Receivable IllustrationsDocument23 pagesACC106 Notes Receivable IllustrationsJohn MaynardNo ratings yet

- Chapter 8 - Notes Payable and Debt Restructuring: Problem 8-7Document3 pagesChapter 8 - Notes Payable and Debt Restructuring: Problem 8-7Pau LaguertaNo ratings yet

- Receivables SolutionDocument3 pagesReceivables SolutionkimberlyNo ratings yet

- Problem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalDocument23 pagesProblem 1 Summary 35 Problem 1 Solution 21 Problem 2 Jes 60 Problem 2 Worksheet 116 Grand TotalAngelica DizonNo ratings yet

- SHE Classroom DiscussionDocument3 pagesSHE Classroom DiscussionBrod Lee SantosNo ratings yet

- Homework SolutionsDocument5 pagesHomework SolutionsAnonymous CuUAaRSNNo ratings yet

- Solution Receivable FinancingDocument3 pagesSolution Receivable FinancingAnonymous CuUAaRSNNo ratings yet

- Frias Activity 6Document6 pagesFrias Activity 6Lars FriasNo ratings yet

- Sol. Man. - Chapter 10 - She (Part 1) - 2021Document18 pagesSol. Man. - Chapter 10 - She (Part 1) - 2021Ventilacion, Jayson M.No ratings yet

- Alcaide, Daiane L. - Activity 1Document10 pagesAlcaide, Daiane L. - Activity 1Daiane AlcaideNo ratings yet

- 2.tutorial Q - Equity Part 1&2Document4 pages2.tutorial Q - Equity Part 1&2LAVINNYA NAIR A P PARBAKARANNo ratings yet

- 01 Financial Investments Overview SolutionsDocument5 pages01 Financial Investments Overview Solutionscristinelarita18No ratings yet

- Abdirahman Assign 1Document8 pagesAbdirahman Assign 1Mazlax YareNo ratings yet

- Assignment On LiabilitiesDocument7 pagesAssignment On LiabilitiesVixen Aaron EnriquezNo ratings yet

- Intermediate Accounting Unit4 - Topic2Document12 pagesIntermediate Accounting Unit4 - Topic2Lea Polinar100% (1)

- CH 8 LiabilitiesDocument10 pagesCH 8 LiabilitiesKrizia Oliva100% (1)

- Acctg 4 Serdan Quiz 3Document7 pagesAcctg 4 Serdan Quiz 3Rica CatanguiNo ratings yet

- Intermediate Accounting Chapter 23 To 35Document101 pagesIntermediate Accounting Chapter 23 To 35Blue SkyNo ratings yet

- The Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyDocument5 pagesThe Following Information For CLH Company Is Available On June 30, 2018, The End of A MonthlyJel SanNo ratings yet

- Quiz IntAccDocument12 pagesQuiz IntAccTrixie HicaldeNo ratings yet

- Answers Part2Document1 pageAnswers Part2Jamaica DavidNo ratings yet

- 07 Receivable Financing 2 SolvingDocument3 pages07 Receivable Financing 2 Solvingkyle mandaresioNo ratings yet

- RecFin AnswerKeySolutionsDocument3 pagesRecFin AnswerKeySolutionsHannah Jane UmbayNo ratings yet

- Group FinancialDocument8 pagesGroup FinancialNever GonondoNo ratings yet

- 4 - Notes Receivable Problems With Solutions: From The TextbookDocument23 pages4 - Notes Receivable Problems With Solutions: From The TextbookKate BNo ratings yet

- Interim ReviewerDocument5 pagesInterim ReviewerDarlyn Dalida San PedroNo ratings yet

- Jawaban Mid Test Praktik Dagang 2022Document14 pagesJawaban Mid Test Praktik Dagang 2022Rahmal SimarangkirNo ratings yet

- Assignment 22 23 26 39Document4 pagesAssignment 22 23 26 39Georgina Francheska RamirezNo ratings yet

- Problem 6-1: Interest Expense Present ValueDocument3 pagesProblem 6-1: Interest Expense Present ValueAngieNo ratings yet

- Tayaban Lancer Company 1Document4 pagesTayaban Lancer Company 1Tayaban Van GihNo ratings yet

- Solution in Single Entry MethodDocument5 pagesSolution in Single Entry MethodYvonne MalingNo ratings yet

- Fin Acc 2 Chap 7Document10 pagesFin Acc 2 Chap 7MkaeDizonNo ratings yet

- Catibog, Marynissa M. (Intermediate Acctg Activity)Document9 pagesCatibog, Marynissa M. (Intermediate Acctg Activity)Marynissa CatibogNo ratings yet

- Note Receivable Problem 6 1 To 6 5Document11 pagesNote Receivable Problem 6 1 To 6 5Jewel Mercano PabalinasNo ratings yet

- Labyrinth Company Required1 Required2 2020Document2 pagesLabyrinth Company Required1 Required2 2020AnonnNo ratings yet

- Problem 16 18Document19 pagesProblem 16 18Shaira BugayongNo ratings yet

- AP 5904Q InvestmentsDocument6 pagesAP 5904Q InvestmentsRhea NograNo ratings yet

- Practice Comptency Exam 124Document3 pagesPractice Comptency Exam 124Ivan Pacificar BioreNo ratings yet

- Ia Forcadela Part IIIDocument5 pagesIa Forcadela Part IIIMary Joanne forcadelaNo ratings yet

- IA 1 - Chapter 6 Notes Receivable Problems Part 1Document6 pagesIA 1 - Chapter 6 Notes Receivable Problems Part 1John CentinoNo ratings yet

- Chapter 15Document8 pagesChapter 15Mychie Lynne MayugaNo ratings yet

- Lecture5 Y4 T1 Internatinal AccountingDocument15 pagesLecture5 Y4 T1 Internatinal AccountingTaha ShawkyNo ratings yet

- Week 1. Introduction and OverviewDocument6 pagesWeek 1. Introduction and OverviewYen YenNo ratings yet

- CHAP 29gDocument17 pagesCHAP 29gYen YenNo ratings yet

- Prefinals Exam in Income TaxationDocument3 pagesPrefinals Exam in Income TaxationYen YenNo ratings yet

- Problem 11-1 Problem 11-2 Answer A: MarketDocument8 pagesProblem 11-1 Problem 11-2 Answer A: MarketYen YenNo ratings yet

- 26 LPDocument18 pages26 LPYen YenNo ratings yet

- Group 5 - FinManDocument6 pagesGroup 5 - FinManYen YenNo ratings yet

- S01 Review On SFP, NFS and RPTDocument3 pagesS01 Review On SFP, NFS and RPTYen YenNo ratings yet

- Problem 3-1 Problem 3-2 Problem 3-3 Problem 3-4 Problem 3-5Document22 pagesProblem 3-1 Problem 3-2 Problem 3-3 Problem 3-4 Problem 3-5Yen YenNo ratings yet

- Chap16 ProblemsDocument20 pagesChap16 ProblemsYen YenNo ratings yet

- FInancial Accounting and Reporting1C6Document19 pagesFInancial Accounting and Reporting1C6Yen YenNo ratings yet

- 1915103-Accounting For ManagementDocument22 pages1915103-Accounting For Managementmercy santhiyaguNo ratings yet

- ProjectsDocument4 pagesProjectsMegha KochharNo ratings yet

- The Rationalization VS The Reduction of Real Costs Under The Modern AgricultureDocument11 pagesThe Rationalization VS The Reduction of Real Costs Under The Modern AgricultureIAEME PublicationNo ratings yet

- Meaning of WTO: WTO - World Trade OrganisationDocument13 pagesMeaning of WTO: WTO - World Trade OrganisationMehak joshiNo ratings yet

- Crown Cork and Seal Case StudyDocument7 pagesCrown Cork and Seal Case StudyManikho KaibiNo ratings yet

- PAMB Medical Revision-35376814 PDFDocument9 pagesPAMB Medical Revision-35376814 PDFSoon SoonNo ratings yet

- AlbertvilleBoazGuntersville - AL - 2023Document93 pagesAlbertvilleBoazGuntersville - AL - 2023ravee12No ratings yet

- College of Computing and Information Sciences: Midterm Assessment Spring 2021 SemesterDocument3 pagesCollege of Computing and Information Sciences: Midterm Assessment Spring 2021 SemesterSohaib RiazNo ratings yet

- Chapter 2 AssignmentDocument3 pagesChapter 2 AssignmentJasmin MarreroNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Praveen PujerNo ratings yet

- Measures of Leverage: Test Code: R37 MSOL Q-BankDocument8 pagesMeasures of Leverage: Test Code: R37 MSOL Q-BankMarwa Abd-ElmeguidNo ratings yet

- NVCA 2023 Yearbook - FINALFINALDocument77 pagesNVCA 2023 Yearbook - FINALFINALP KeatingNo ratings yet

- Hospital BenchmarkingDocument11 pagesHospital BenchmarkingDana ApostolNo ratings yet

- Inequality: Income and Wealth Distribution: ECN105 Contemporary Economic IssuesDocument42 pagesInequality: Income and Wealth Distribution: ECN105 Contemporary Economic IssuesHarry SinghNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 2Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 2Roshan RamkhalawonNo ratings yet

- Role of DFHI in Money MarketDocument13 pagesRole of DFHI in Money Marketmanishg_17100% (1)

- Chapter 02: Credit and Collection Operations: Lesson 02Document10 pagesChapter 02: Credit and Collection Operations: Lesson 02Llyod Daniel PauloNo ratings yet

- Agyapa Royalty Transaction Chart, Tables, NotesDocument5 pagesAgyapa Royalty Transaction Chart, Tables, NotesKweku ZurekNo ratings yet

- Acct Assign 8Document2 pagesAcct Assign 82K22DMBA48 himanshiNo ratings yet

- Analisis Hukum Terhadap Prinsip Most Favoured Nations Dalam Sengketa Dagang Impor Produk BesiDocument10 pagesAnalisis Hukum Terhadap Prinsip Most Favoured Nations Dalam Sengketa Dagang Impor Produk BesiAdriansyah PutraNo ratings yet

- Pso FinalDocument15 pagesPso FinalAdeel SajidNo ratings yet

- Analysis of GDP of India From 1990-2010Document21 pagesAnalysis of GDP of India From 1990-2010aditig2267% (6)

- MBA Final Project InterwoodDocument99 pagesMBA Final Project InterwoodabdurrafayhaiderNo ratings yet

- Permanent Transfer ClaimDocument2 pagesPermanent Transfer ClaimdpdohisarNo ratings yet

- Etisalat Group Capital Markets Day 2021Document144 pagesEtisalat Group Capital Markets Day 2021قحطان القحطانيNo ratings yet

- Shweta AggarwalDocument87 pagesShweta Aggarwalkomal vermaNo ratings yet

- Answer To The Question From The BookDocument11 pagesAnswer To The Question From The BookCindy KimNo ratings yet

- White Paper On Industries Dept PDFDocument47 pagesWhite Paper On Industries Dept PDFSunny Dara Rinnah SusanthNo ratings yet