You might also like

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 10Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 10Roshan RamkhalawonNo ratings yet

- Chapter 30 Costing Principles and Systems - Total (Or Absorption) Costing Q1 (A)Document2 pagesChapter 30 Costing Principles and Systems - Total (Or Absorption) Costing Q1 (A)Fegason FegyNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 21Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 21Roshan RamkhalawonNo ratings yet

- Assignment - OHD ACC116Document3 pagesAssignment - OHD ACC116Nurul NajihaNo ratings yet

- Particulars P1 P2Document4 pagesParticulars P1 P2sanket pareekNo ratings yet

- Cost & Management Accounting - MGT402 Power Point Slides Lecture 15Document22 pagesCost & Management Accounting - MGT402 Power Point Slides Lecture 15Mr. JalilNo ratings yet

- Acc116 Assignment Ahmad Irfan Bin Zakaria 2020836308Document7 pagesAcc116 Assignment Ahmad Irfan Bin Zakaria 2020836308Siti RuzanaNo ratings yet

- This Examples Are Adapted FROM Cost and Management Accounting (1996) Prentice Hall ISBN 0-13-205923-1Document10 pagesThis Examples Are Adapted FROM Cost and Management Accounting (1996) Prentice Hall ISBN 0-13-205923-1pandy1604No ratings yet

- Absorption (Total) Costing AnswersDocument7 pagesAbsorption (Total) Costing AnswersNalan TafanaNo ratings yet

- Aluko LTDDocument8 pagesAluko LTDhafsa.jamilNo ratings yet

- Tube Well Ar New Rate June 2019 1Document67 pagesTube Well Ar New Rate June 2019 1paduuNo ratings yet

- Week 4 - Seminar 3 Trimake Solution A) and B) OnlyDocument3 pagesWeek 4 - Seminar 3 Trimake Solution A) and B) Onlychina xiNo ratings yet

- Bacc232 .309 Management Accounting Assignment 1Document13 pagesBacc232 .309 Management Accounting Assignment 1TarusengaNo ratings yet

- 21st - OCTOBER - 2022-TODAY CLASS - DotDocument23 pages21st - OCTOBER - 2022-TODAY CLASS - DotPalesaNo ratings yet

- ACB 10203 Tutorial Cost Allocation With SolutionDocument5 pagesACB 10203 Tutorial Cost Allocation With SolutionainfarhanaNo ratings yet

- Emmppe Associates. Monthly Efficiency of PRODUCTION APRIL 2019-2020Document10 pagesEmmppe Associates. Monthly Efficiency of PRODUCTION APRIL 2019-2020dsivakumarNo ratings yet

- Tutorial 2 Traditional Overhead Q A STUDENT PDFDocument6 pagesTutorial 2 Traditional Overhead Q A STUDENT PDFN FrzanahNo ratings yet

- FINANCIAL MANAGEMENT Fonderia Di TorinoDocument14 pagesFINANCIAL MANAGEMENT Fonderia Di Torinomochammad rifaiNo ratings yet

- Lecture 14 POADocument7 pagesLecture 14 POALau Chun GuiNo ratings yet

- 4 2006 Dec ADocument5 pages4 2006 Dec Aapi-19836745No ratings yet

- Unit 2 - Question BankDocument34 pagesUnit 2 - Question BankTamaraNo ratings yet

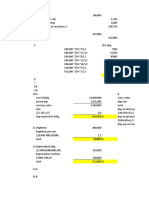

- Mechanical Drying Equipment FinalDocument8 pagesMechanical Drying Equipment Finalvijaypal2000100% (1)

- Overhead: Allocation & ApportionmentDocument10 pagesOverhead: Allocation & ApportionmentbiarrahsiaNo ratings yet

- AmountDocument3 pagesAmountJudy TotoNo ratings yet

- ABC - Process.Cost Allocation.Document21 pagesABC - Process.Cost Allocation.Keyt VintageNo ratings yet

- f5 Worksheet BPPDocument19 pagesf5 Worksheet BPPYashna SohawonNo ratings yet

- The Other: Cost AccowntingDocument7 pagesThe Other: Cost AccowntingLakshmi SNo ratings yet

- Unit One Process CostingDocument9 pagesUnit One Process CostingDzukanji SimfukweNo ratings yet

- 11 32 PDFDocument15 pages11 32 PDFNicNo ratings yet

- s15 16 (AutoRecovered)Document14 pagess15 16 (AutoRecovered)R GNo ratings yet

- Chapter 15 - Adv CostDocument8 pagesChapter 15 - Adv CostKIROJOHNo ratings yet

- Mystic SportsDocument34 pagesMystic SportshelloNo ratings yet

- Suggested Answers Certified Finance and Accounting Professional Examination - Summer 2021Document12 pagesSuggested Answers Certified Finance and Accounting Professional Examination - Summer 2021muhammad osamaNo ratings yet

- Acc 116 Group AssignmentDocument4 pagesAcc 116 Group AssignmentIzzaty AffrinaNo ratings yet

- Management and Financial Accounting Assessment-2Document6 pagesManagement and Financial Accounting Assessment-2saranyaNo ratings yet

- 2022 12 01 Answer Key Additional M6 M7Document15 pages2022 12 01 Answer Key Additional M6 M7Niger RomeNo ratings yet

- Cost Accounting - Author William K. Carter - 14ed-297-298Document2 pagesCost Accounting - Author William K. Carter - 14ed-297-298dindaNo ratings yet

- Final Exam Spring - 2020 Subject: Cost and Management Accounting Program: BBADocument21 pagesFinal Exam Spring - 2020 Subject: Cost and Management Accounting Program: BBAMadiha Baqai EntertainmentNo ratings yet

- Manac3 Supplementary June Memo 2023Document11 pagesManac3 Supplementary June Memo 2023LuciaNo ratings yet

- AS - Cost Accountting 3 - Past PaperDocument6 pagesAS - Cost Accountting 3 - Past PaperAvikamm AgrawalNo ratings yet

- Service Costs AllocationDocument13 pagesService Costs AllocationKim EllaNo ratings yet

- Cost Accounting AssignmentDocument6 pagesCost Accounting AssignmentRamalu Dinesh ReddyNo ratings yet

- Tutorial Chapter 1Document5 pagesTutorial Chapter 1LolAnonNo ratings yet

- Q-6 Spr-08 (Yahya Limited) Q ADocument2 pagesQ-6 Spr-08 (Yahya Limited) Q AiamneonkingNo ratings yet

- MILLICHEM FormatDocument2 pagesMILLICHEM FormatMuhammad JunaidNo ratings yet

- Manac3 Main Exam Memo June 2023Document9 pagesManac3 Main Exam Memo June 2023LuciaNo ratings yet

- Absorption Costing QuestionsDocument10 pagesAbsorption Costing QuestionsJean LeongNo ratings yet

- Tutorial Overhead StudentsDocument8 pagesTutorial Overhead Studentsnatasha thaiNo ratings yet

- Pre-Final Exam in Audit 2-3Document5 pagesPre-Final Exam in Audit 2-3Shr BnNo ratings yet

- Activity Based-WPS (Number 1 C)Document9 pagesActivity Based-WPS (Number 1 C)Takudzwa BenjaminNo ratings yet

- Millichem Solution XDocument6 pagesMillichem Solution XMuhammad JunaidNo ratings yet

- Tutorial 2 CH 3Document4 pagesTutorial 2 CH 3Codreanu AndaNo ratings yet

- AFAR First Preboard 93 - SolutionsDocument12 pagesAFAR First Preboard 93 - SolutionsEpfie SanchesNo ratings yet

- Harsh Electricals: Analyzing Cost in Search of ProfitDocument11 pagesHarsh Electricals: Analyzing Cost in Search of ProfitSanJana NahataNo ratings yet

- Tutorial 5Document7 pagesTutorial 5YANG YUN RUINo ratings yet

- These Overhead Are To Be Allocated and Apportioned To The Four Departements Using The Information BelowDocument13 pagesThese Overhead Are To Be Allocated and Apportioned To The Four Departements Using The Information BelowKos PaviliunNo ratings yet

- Chapter 8 Ed 18Document27 pagesChapter 8 Ed 18Audi WibisonoNo ratings yet

- Absorption Costing For StudentsDocument37 pagesAbsorption Costing For StudentsRaiqueNo ratings yet

- Tut 5 Overheads PDFDocument7 pagesTut 5 Overheads PDFYANG YUN RUINo ratings yet

- European Contract Electronics Assembly Industry - 1993-97: A Strategic Study of the European CEM IndustryFrom EverandEuropean Contract Electronics Assembly Industry - 1993-97: A Strategic Study of the European CEM IndustryNo ratings yet

- Manufacturing Accounts Notes and QuestionsDocument31 pagesManufacturing Accounts Notes and QuestionsRoshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 13Document6 pagesManufacturing Account Worked Example Question 13Roshan Ramkhalawon100% (1)

- Manufacturing Account Worked Example Question 4Document5 pagesManufacturing Account Worked Example Question 4Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 17Document6 pagesManufacturing Account Worked Example Question 17Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 8Document7 pagesManufacturing Account Worked Example Question 8Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 18Document5 pagesManufacturing Account Worked Example Question 18Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 12Document6 pagesManufacturing Account Worked Example Question 12Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 7Document4 pagesManufacturing Account Worked Example Question 7Roshan Ramkhalawon100% (1)

- Manufacturing Account Worked Example Question 16Document5 pagesManufacturing Account Worked Example Question 16Roshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 2Document4 pagesManufacturing Account Worked Example Question 2Roshan RamkhalawonNo ratings yet

- Joint Venture Worked Examples Question 6 - No Separate Books of AccountsDocument3 pagesJoint Venture Worked Examples Question 6 - No Separate Books of AccountsRoshan RamkhalawonNo ratings yet

- Joint Venture Worked Example Question 3 - Separte Books of AccountsDocument3 pagesJoint Venture Worked Example Question 3 - Separte Books of AccountsRoshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 3Document3 pagesManufacturing Account Worked Example Question 3Roshan RamkhalawonNo ratings yet

- Joint Venture Worked Example Question 4 - Separate Books of AccountsDocument4 pagesJoint Venture Worked Example Question 4 - Separate Books of AccountsRoshan RamkhalawonNo ratings yet

- Manufacturing Account Worked Example Question 9Document5 pagesManufacturing Account Worked Example Question 9Roshan RamkhalawonNo ratings yet

- Joint Venture Worked Example Question 8 - No Seperate Books of AccountsDocument4 pagesJoint Venture Worked Example Question 8 - No Seperate Books of AccountsRoshan RamkhalawonNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 5Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 5Roshan RamkhalawonNo ratings yet

- Joint Venture Worked Example Question 1 - Separate Books of AccountDocument2 pagesJoint Venture Worked Example Question 1 - Separate Books of AccountRoshan RamkhalawonNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 20Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 20Roshan RamkhalawonNo ratings yet

- Joint Venture Worked Example Question 5 - Separate Books of AccountsDocument3 pagesJoint Venture Worked Example Question 5 - Separate Books of AccountsRoshan RamkhalawonNo ratings yet

- PAPER-3 Worked SolutionsDocument401 pagesPAPER-3 Worked SolutionsRoshan Ramkhalawon100% (1)

- Grade Thresholds - June 2021: Cambridge International AS & A Level Accounting (9706)Document2 pagesGrade Thresholds - June 2021: Cambridge International AS & A Level Accounting (9706)Roshan RamkhalawonNo ratings yet

- O Level IGCSE Accounting Notes Final NauDocument14 pagesO Level IGCSE Accounting Notes Final NauRoshan RamkhalawonNo ratings yet

- Balancing of Accounts SolutionDocument3 pagesBalancing of Accounts SolutionRoshan RamkhalawonNo ratings yet

- Joint Venture AsdDocument15 pagesJoint Venture AsdRoshan RamkhalawonNo ratings yet

- Accounting As-Level Paper 2 Topical andDocument19 pagesAccounting As-Level Paper 2 Topical andRoshan Ramkhalawon33% (3)

- Accounting Concept or Principles PDFDocument3 pagesAccounting Concept or Principles PDFRoshan RamkhalawonNo ratings yet

- A Levels Accounting Notes PDFDocument207 pagesA Levels Accounting Notes PDFLeanne Teh100% (4)

- CAF 1 IA Autumn 2020Document5 pagesCAF 1 IA Autumn 2020Qasim Hafeez KhokharNo ratings yet

- Starbucks Equity StoryDocument28 pagesStarbucks Equity StoryBlueBookNo ratings yet

- Pas 10 - SummaryDocument1 pagePas 10 - SummaryBirdWin WinNo ratings yet

- Far Set2 A Basic Reviewer For Financial Accounting and Reporting 1Document6 pagesFar Set2 A Basic Reviewer For Financial Accounting and Reporting 1AShley NIcole0% (1)

- LGU-NGAS TableofContentsVol1Document6 pagesLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaNo ratings yet

- Activity-Based CostingDocument75 pagesActivity-Based CostingmrnttdpnchngNo ratings yet

- Ifrs 16 SimulationDocument7 pagesIfrs 16 SimulationSuryadi100% (1)

- أهمية التدقيق الداخلي في الرفع من جودة القوائم المالية في المؤسسات الجزائرية.Document17 pagesأهمية التدقيق الداخلي في الرفع من جودة القوائم المالية في المؤسسات الجزائرية.asmaatr44No ratings yet

- ATHE Level 5 Qualifications in AccountingDocument35 pagesATHE Level 5 Qualifications in AccountingPartho DhakaNo ratings yet

- QMS ProposalDocument22 pagesQMS Proposalflawlessy2kNo ratings yet

- MCQ With AnsDocument68 pagesMCQ With AnsRosemarie Cruz0% (2)

- Financial Accounting 4th Edition Spiceland Solutions Manual DownloadDocument45 pagesFinancial Accounting 4th Edition Spiceland Solutions Manual DownloadMark Arteaga100% (21)

- Control Accounts Topic 1 PDFDocument9 pagesControl Accounts Topic 1 PDFpaul nsalambaNo ratings yet

- Reviewer For AccountingDocument7 pagesReviewer For AccountingRoesell Anne EspeletaNo ratings yet

- User Guide MYOBDocument296 pagesUser Guide MYOBAdin Dian RatnawatiNo ratings yet

- Learning Activity Sheet in FABM I: III. Matching TypeDocument1 pageLearning Activity Sheet in FABM I: III. Matching Typeocampo mtbNo ratings yet

- Accounting 2&3 PretestDocument11 pagesAccounting 2&3 Pretestelumba michaelNo ratings yet

- Costing PDFDocument90 pagesCosting PDFAbhi Joshi100% (1)

- Foundations of Financial Management 17th Edition Block Test BankDocument43 pagesFoundations of Financial Management 17th Edition Block Test BankDeniseOsbornefpexj100% (14)

- Ipaper For Book NID#41987Document443 pagesIpaper For Book NID#41987bfelix100% (1)

- CFI Accounting FactsheetDocument1 pageCFI Accounting FactsheetPirvuNo ratings yet

- Executive Summary A.Introduction: Comparative Presentation of Total Assets, Liabilities, Equity, Income and ExpensesDocument8 pagesExecutive Summary A.Introduction: Comparative Presentation of Total Assets, Liabilities, Equity, Income and ExpensesArchAngel Grace Moreno BayangNo ratings yet

- The Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaDocument10 pagesThe Effect of International Public Sector Accounting Standard (IPSAS) Implementation and Public Financial Management in NigeriaaijbmNo ratings yet

- Journal Entries: Example 1: Whole-Period Depreciation in The Period of PurchaseDocument2 pagesJournal Entries: Example 1: Whole-Period Depreciation in The Period of PurchasemulualemNo ratings yet

- Accounting Principles: A Business Perspective, Financial Accounting (Chapters 9 - 18)Document604 pagesAccounting Principles: A Business Perspective, Financial Accounting (Chapters 9 - 18)textbookequity50% (4)

- Pastiland 5.0 SheetDocument6 pagesPastiland 5.0 SheetAngel De LeonNo ratings yet

- Water World Park Work Sheet For The Year Ended September 30, 2003 Unadjusted Trial Balance Adjustments Account Titles Dr. Cr. Dr. CRDocument6 pagesWater World Park Work Sheet For The Year Ended September 30, 2003 Unadjusted Trial Balance Adjustments Account Titles Dr. Cr. Dr. CRbabe447100% (1)

- University of Cambridge International Examinations General Certificate of Education Ordinary LevelDocument16 pagesUniversity of Cambridge International Examinations General Certificate of Education Ordinary Levelmeelas123No ratings yet

- S4 Hana Finance Full Implem Configuration DocumentDocument9 pagesS4 Hana Finance Full Implem Configuration DocumentMayankNo ratings yet

- MCQ'S Auditing Sem 4Document31 pagesMCQ'S Auditing Sem 4Siddharth VoraNo ratings yet