You might also like

- Give Yourself Credit: Financial Goals and Organizing Your RecordsDocument43 pagesGive Yourself Credit: Financial Goals and Organizing Your RecordsFadhel GhribiNo ratings yet

- Citibank Bank StatementDocument7 pagesCitibank Bank StatementJOHNNo ratings yet

- Commercial Bank of Ethiopia: Account StatementDocument27 pagesCommercial Bank of Ethiopia: Account StatementSamuel Abebe60% (5)

- Used Car BusinessDocument32 pagesUsed Car BusinessashismechNo ratings yet

- DIP20 Assignment 4 Submission 1 Arun KannathDocument42 pagesDIP20 Assignment 4 Submission 1 Arun Kannathmonika_s1976100% (9)

- Debit cards overtake credit cards in IndiaDocument62 pagesDebit cards overtake credit cards in Indiafaik100% (1)

- Contestable Markets and the Rise of CompetitionDocument8 pagesContestable Markets and the Rise of Competitionman downNo ratings yet

- Bank statement summary for September 2016Document1 pageBank statement summary for September 2016Imran7878No ratings yet

- Supermarket Industry PorterDocument5 pagesSupermarket Industry PorterMiklós BarnabásNo ratings yet

- 447096602-Preview-Falix-Pdf - EkhaguereDocument5 pages447096602-Preview-Falix-Pdf - Ekhaguere13KARATNo ratings yet

- Your monthly bank statement summaryDocument4 pagesYour monthly bank statement summaryShakir MujtabaNo ratings yet

- Statement 30-DEC-22 AC 50882755 01045142 PDFDocument5 pagesStatement 30-DEC-22 AC 50882755 01045142 PDFferuzbekNo ratings yet

- European Automotive After Market LandscapeDocument21 pagesEuropean Automotive After Market LandscapeSohom KarmakarNo ratings yet

- Case Study Risk ManagementDocument3 pagesCase Study Risk ManagementFerl Diane Siño50% (2)

- Data CaptureDocument14 pagesData CaptureJaime BasabeNo ratings yet

- Intermediate AccountingDocument6 pagesIntermediate AccountingMary Angeline LopezNo ratings yet

- Porter 5 Forces I.EDocument4 pagesPorter 5 Forces I.Eazza_j50% (2)

- Ocado CaseDocument18 pagesOcado CasePedro Surish Zepeda0% (1)

- Dhanalaxmi Bank Final Project Report by YkartheekgupthaDocument75 pagesDhanalaxmi Bank Final Project Report by YkartheekgupthaYkartheek GupthaNo ratings yet

- Itep Onlıne Grocery - Reading TestDocument5 pagesItep Onlıne Grocery - Reading TestCihan ÖztürkNo ratings yet

- Quality Enhancement in Voluntary Carbon Markets: Opening up for MainstreamFrom EverandQuality Enhancement in Voluntary Carbon Markets: Opening up for MainstreamNo ratings yet

- Introduction To Audit of CashDocument16 pagesIntroduction To Audit of CashDummy GoogleNo ratings yet

- Oligopoly - Collusion Case StudyDocument5 pagesOligopoly - Collusion Case StudyBenLemmonNo ratings yet

- A2 Markets MergersDocument8 pagesA2 Markets MergersTamani MoyoNo ratings yet

- EC Competition & Consumer 2004Document30 pagesEC Competition & Consumer 2004padebritoNo ratings yet

- A2 Contestable Markets Economics Unit 3Document6 pagesA2 Contestable Markets Economics Unit 3MohamedNazaalNo ratings yet

- Car Price Differentials in The European UnionDocument8 pagesCar Price Differentials in The European UnionDavis Nadakkavukaran SanthoshNo ratings yet

- B2B MarketingDocument4 pagesB2B Marketingmms a19No ratings yet

- The Retail Market Review - Findings and Initial Proposals: ConsultationDocument81 pagesThe Retail Market Review - Findings and Initial Proposals: ConsultationjacksonpenNo ratings yet

- EU car market price differentials and 2005 regulationsDocument3 pagesEU car market price differentials and 2005 regulationsDinesh Raghavendra100% (2)

- More Innovation Needed in Home Buying and Selling Market, Oft FindsDocument4 pagesMore Innovation Needed in Home Buying and Selling Market, Oft Findsapi-26654951No ratings yet

- Supermarket dominance scrutinized: Competition concerns riseDocument5 pagesSupermarket dominance scrutinized: Competition concerns riseLingesh KumarNo ratings yet

- European Car Industry CO2 LegislationDocument10 pagesEuropean Car Industry CO2 LegislationCharlene WilsonNo ratings yet

- Pricing in Separable Channels (Various)Document8 pagesPricing in Separable Channels (Various)Μιχάλης ΘεοχαρόπουλοςNo ratings yet

- Review On Market StructureDocument5 pagesReview On Market StructureSukhdeep Kaur MannNo ratings yet

- IAS - Business - Student - Book - Answers - Unit - 1Document81 pagesIAS - Business - Student - Book - Answers - Unit - 1temwaniNo ratings yet

- International A Level Business Student Book Answers Unit 1Document81 pagesInternational A Level Business Student Book Answers Unit 1俊名陈100% (1)

- Traditional Global Pricing Strategies: The Cannibalization DilemmaDocument3 pagesTraditional Global Pricing Strategies: The Cannibalization DilemmaSAMIA AKHTARNo ratings yet

- Why monopolies create deadweight lossDocument4 pagesWhy monopolies create deadweight lossGeorgie HancockNo ratings yet

- Luxury Pricing ArticleDocument7 pagesLuxury Pricing ArticledesigneducationNo ratings yet

- CompetitionWithExclusiveCon PreviewDocument30 pagesCompetitionWithExclusiveCon PreviewJinwoo KimNo ratings yet

- Business To Business Marketplaces and Canadian Competition LawDocument17 pagesBusiness To Business Marketplaces and Canadian Competition Lawskumar_p7No ratings yet

- Effects of Competitive MarketsDocument7 pagesEffects of Competitive MarketsTina VicNo ratings yet

- How Many Grocery Stores Are in The UK Marketing EssayDocument13 pagesHow Many Grocery Stores Are in The UK Marketing EssayHND Assignment HelpNo ratings yet

- EC Retail Food StudyDocument3 pagesEC Retail Food StudyTomşa AndreiNo ratings yet

- Hem SirDocument10 pagesHem SirSaim KhanNo ratings yet

- Dobson2001 Article BuyerPowerAndItsImpactOnCompetDocument35 pagesDobson2001 Article BuyerPowerAndItsImpactOnCompetConstanța TiuhtiiNo ratings yet

- Analysis of the Growing Online Grocery Home Delivery SectorDocument14 pagesAnalysis of the Growing Online Grocery Home Delivery SectorLekan AkinolaNo ratings yet

- Car Price DifferentialsDocument6 pagesCar Price Differentialspity100% (1)

- European Car IndustryDocument43 pagesEuropean Car IndustryMario Zambrano CéspedesNo ratings yet

- Collusive and Non-Collusive OligopolyDocument7 pagesCollusive and Non-Collusive Oligopolymohanraokp2279No ratings yet

- European Commission - PRESS RELEASES - Press Release - Questions and Answers - Digital Single Market StrategyDocument6 pagesEuropean Commission - PRESS RELEASES - Press Release - Questions and Answers - Digital Single Market StrategyMonika PerezNo ratings yet

- CASE 1: Predatory RoamingDocument4 pagesCASE 1: Predatory RoamingBen HiranNo ratings yet

- Ass#3 Industry Analysis The FundamentalsDocument6 pagesAss#3 Industry Analysis The Fundamentalsgian kaye aglagadanNo ratings yet

- Market Structure Analysis: Monopoly and Price DiscriminationDocument5 pagesMarket Structure Analysis: Monopoly and Price DiscriminationvjpopinesNo ratings yet

- Business EnvironDocument8 pagesBusiness EnvironRuth GhaleyNo ratings yet

- UK Supermarket Industry Performance and Future OutlookDocument10 pagesUK Supermarket Industry Performance and Future OutlookSaim KhanNo ratings yet

- Ass#3 Industry Analysis The FundamentalsDocument6 pagesAss#3 Industry Analysis The Fundamentalsgian kaye aglagadanNo ratings yet

- Opportunities in Chemical DistributionDocument16 pagesOpportunities in Chemical DistributionVishal KanojiyaNo ratings yet

- Economics Exam Notes - MonopolyDocument5 pagesEconomics Exam Notes - MonopolyDistingNo ratings yet

- Porter's Five Forces Analysis of the UK Beer IndustryDocument4 pagesPorter's Five Forces Analysis of the UK Beer IndustrySanam AdvaniNo ratings yet

- oligopolyDocument3 pagesoligopolyRokaia MortadaNo ratings yet

- Price Comparison and Pricing Strategies A Case Study: The Italian Motorway Refuelling MarketDocument39 pagesPrice Comparison and Pricing Strategies A Case Study: The Italian Motorway Refuelling MarketZehra KHanNo ratings yet

- To What Extent Is The Retail Fuel Market in Houston's Energy Corridor Operating As A Monopolistically Competitive Market?Document25 pagesTo What Extent Is The Retail Fuel Market in Houston's Energy Corridor Operating As A Monopolistically Competitive Market?DevikaNo ratings yet

- CarTrade - White PaperDocument20 pagesCarTrade - White Paperaman3125No ratings yet

- Competition and Antitrust LawDocument2 pagesCompetition and Antitrust LawEmeka NkemNo ratings yet

- A Quantitative Analysis of The Used-Car MarketDocument36 pagesA Quantitative Analysis of The Used-Car MarketLuana MottaNo ratings yet

- Ebook Economics For Today Asia Pacific 5Th Edition Layton Solutions Manual Full Chapter PDFDocument29 pagesEbook Economics For Today Asia Pacific 5Th Edition Layton Solutions Manual Full Chapter PDFenstatequatrain1jahl100% (9)

- Task 12, 13, 14Document7 pagesTask 12, 13, 14bendermacherrickNo ratings yet

- The Task EnvironmentDocument8 pagesThe Task EnvironmentStoryKingNo ratings yet

- Value Creation StrategiesDocument13 pagesValue Creation StrategiesFarooq AzamNo ratings yet

- Sainsbury and Asda ResearchDocument9 pagesSainsbury and Asda Researchtayyab0% (1)

- The Regulatory Environment: Part Two of The Investors' Guide to the United Kingdom 2015/16From EverandThe Regulatory Environment: Part Two of The Investors' Guide to the United Kingdom 2015/16No ratings yet

- Evidence of Oligopolistic CollusionDocument5 pagesEvidence of Oligopolistic CollusionCatalinaNo ratings yet

- A Products Life CycleDocument2 pagesA Products Life CycleCatalinaNo ratings yet

- Klassenzimmer Flash Bilder PDFDocument5 pagesKlassenzimmer Flash Bilder PDFCatalinaNo ratings yet

- Klassenzimmer Pairs Bild Bild PDFDocument2 pagesKlassenzimmer Pairs Bild Bild PDFCatalinaNo ratings yet

- Oligopolistic and small bakers competitionDocument2 pagesOligopolistic and small bakers competitionCatalinaNo ratings yet

- BA's Low-Cost Airline Go Faces Predatory Pricing ClaimsDocument3 pagesBA's Low-Cost Airline Go Faces Predatory Pricing ClaimsCatalinaNo ratings yet

- Mothers Day Vocabulary Esl Missing Letters in Words Worksheet For KidsDocument2 pagesMothers Day Vocabulary Esl Missing Letters in Words Worksheet For KidsCatalinaNo ratings yet

- Mothers Day Vocabulary Esl Word Search Puzzle Worksheet For KidsDocument2 pagesMothers Day Vocabulary Esl Word Search Puzzle Worksheet For KidsCatalina100% (1)

- Standard English and Its DialectsDocument3 pagesStandard English and Its DialectsCatalinaNo ratings yet

- Mothers Day Vocabulary Esl Unscramble The Words Worksheet For KidsDocument2 pagesMothers Day Vocabulary Esl Unscramble The Words Worksheet For KidsCatalinaNo ratings yet

- Loan Disbursement and Recovery System of a State-Owned BankDocument46 pagesLoan Disbursement and Recovery System of a State-Owned BankNil PoriNo ratings yet

- Banking FacilitiesDocument3 pagesBanking FacilitiesOsama AhmedNo ratings yet

- Table of Interest Rates-En-2015Document24 pagesTable of Interest Rates-En-2015Doge IronyNo ratings yet

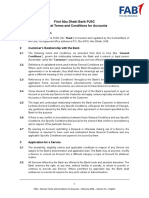

- FAB General Terms and Conditions For AccountsDocument31 pagesFAB General Terms and Conditions For AccountsWaqas BarikNo ratings yet

- FI Account Opening Form 1Document3 pagesFI Account Opening Form 1gopal_psbNo ratings yet

- Chapter-01 Accounting For Banking CompanyDocument26 pagesChapter-01 Accounting For Banking CompanyRabbi Ul Apon100% (1)

- Services Covered by The Consumer Protection Act, 2019Document9 pagesServices Covered by The Consumer Protection Act, 2019MorrisNo ratings yet

- Chapter One Introduction of The Study BackgroundDocument55 pagesChapter One Introduction of The Study BackgroundPrince SomuahNo ratings yet

- Sole Proprietor Letter for Banking ServicesDocument2 pagesSole Proprietor Letter for Banking ServicestamilmaranNo ratings yet

- YES BANK Digi Pro League ContestDocument5 pagesYES BANK Digi Pro League ContestNaveenKumarReddyNo ratings yet

- Statements 8151Document2 pagesStatements 8151Cathy CastyNo ratings yet

- Brs Practise SheetDocument1 pageBrs Practise Sheetapi-252642432No ratings yet

- Screenshot 2023-11-16 at 11.45.49 PMDocument27 pagesScreenshot 2023-11-16 at 11.45.49 PMmimienordin4No ratings yet

- Vijaya Bank Loans and Advances PerformanceDocument80 pagesVijaya Bank Loans and Advances Performanceram801100% (1)

- Vaishu Final ProjectDocument96 pagesVaishu Final ProjectShravan SinghNo ratings yet

- NEXA-Resolution and Letter For Mobile Banking FacilityDocument3 pagesNEXA-Resolution and Letter For Mobile Banking Facilitywebstar TechnologyNo ratings yet