You might also like

- Pensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemFrom EverandPensions in Italy: The guide to pensions in Italy, with the rules for accessing ordinary and early retirement in the public and private systemNo ratings yet

- Japan's Pension System: Challenges and ImplicationsDocument6 pagesJapan's Pension System: Challenges and ImplicationsMarco AbatNo ratings yet

- Public Private Partnership-: Lessons from Gujarat for Uttar PradeshFrom EverandPublic Private Partnership-: Lessons from Gujarat for Uttar PradeshNo ratings yet

- Research PaperDocument8 pagesResearch PaperdarshanNo ratings yet

- Ijmet 10 01 048Document8 pagesIjmet 10 01 048IAEME PUBLICATIONNo ratings yet

- A Study On Coping Strategy of Mega Pension Scheme: A Pension For Unorganised Sectors in IndiaDocument17 pagesA Study On Coping Strategy of Mega Pension Scheme: A Pension For Unorganised Sectors in Indiathega leesanNo ratings yet

- Pension Reform in India - A Social Security Need (D. Swarup, Chairman, PFRDA)Document16 pagesPension Reform in India - A Social Security Need (D. Swarup, Chairman, PFRDA)Andre NoortNo ratings yet

- Krishna Murari - Desempeño Ajustado Por Riesgo Pensio Fund India (2020)Document16 pagesKrishna Murari - Desempeño Ajustado Por Riesgo Pensio Fund India (2020)WilmerFlórezNo ratings yet

- GoswamiDocument38 pagesGoswamiMahendra SinghNo ratings yet

- National Rural Employment Guarantee Act: An Effective Safety Net?Document14 pagesNational Rural Employment Guarantee Act: An Effective Safety Net?ankitaNo ratings yet

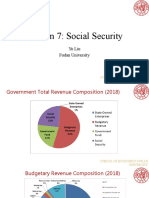

- Session 7: Social Security: Yu Liu Fudan UniversityDocument58 pagesSession 7: Social Security: Yu Liu Fudan UniversityWong HauyuNo ratings yet

- T T SeptemberDocument10 pagesT T SeptemberifhdNo ratings yet

- Dynamics of Population Ageing by Tarun DasDocument18 pagesDynamics of Population Ageing by Tarun DasProfessor Tarun DasNo ratings yet

- Liberalization of Pension Sector in India: Macro Economics and Global Business EnvironmentDocument21 pagesLiberalization of Pension Sector in India: Macro Economics and Global Business Environmentchaitu_88No ratings yet

- Indian Pension System: Problems and PrognosisDocument38 pagesIndian Pension System: Problems and PrognosisDennykumarNo ratings yet

- Employee Benefits in India: An Introduction: White PaperDocument4 pagesEmployee Benefits in India: An Introduction: White PaperHushNo ratings yet

- P1-Healthcare and RD Landscape in SingaporeDocument20 pagesP1-Healthcare and RD Landscape in Singaporedanielfetrick22No ratings yet

- Format+of+Summer+-Winter+TrgDocument6 pagesFormat+of+Summer+-Winter+TrgsandeepNo ratings yet

- Pension InsurnaceDocument85 pagesPension InsurnaceBhavika TheraniNo ratings yet

- The Emerging Pension Scenario in IndiaDocument93 pagesThe Emerging Pension Scenario in IndiaDipesh JainNo ratings yet

- A Study On Employee Perceptions On Employee Provident Fund in Amara Raja Infra Pvt. LTD., TirupatiDocument4 pagesA Study On Employee Perceptions On Employee Provident Fund in Amara Raja Infra Pvt. LTD., TirupatiEditor IJTSRDNo ratings yet

- Retirement Policy and Problem of Implementation in Nigerian Public Sector (A Case Study of Enugu State Civil ServiceDocument118 pagesRetirement Policy and Problem of Implementation in Nigerian Public Sector (A Case Study of Enugu State Civil ServiceNelson Highfliers100% (1)

- My Literature ReviewDocument10 pagesMy Literature ReviewAjNo ratings yet

- Keywords:: Pension Pension Reform Workers Well-Being Error Correction ModelDocument14 pagesKeywords:: Pension Pension Reform Workers Well-Being Error Correction ModelrevolutionguyNo ratings yet

- Pension in India ShodhgangaDocument44 pagesPension in India ShodhgangaNiharika Singh100% (1)

- White Paper On PensionDocument15 pagesWhite Paper On PensiontirthanpNo ratings yet

- Making Social Welfare UniversalDocument3 pagesMaking Social Welfare UniversalKamalNo ratings yet

- Tha Pension SystemDocument2 pagesTha Pension SystemNon OmNo ratings yet

- European Semester Thematic Factsheet Active Labour Market Policies en 0Document13 pagesEuropean Semester Thematic Factsheet Active Labour Market Policies en 0Vișan Rareș Vișan RareșNo ratings yet

- Broad-Based Growth VitalDocument3 pagesBroad-Based Growth VitalTithi jainNo ratings yet

- A Description of The Pension System in Uganda Blog Article 1Document7 pagesA Description of The Pension System in Uganda Blog Article 1mutaaweNo ratings yet

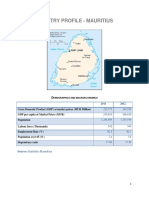

- Mauritius Pension System ProfileDocument9 pagesMauritius Pension System ProfileDarren OwenNo ratings yet

- A Project Report On Employee Benefit Scheme in PVT Sector: CtrlsoftDocument62 pagesA Project Report On Employee Benefit Scheme in PVT Sector: CtrlsoftArjunNo ratings yet

- The Influence of Training On Expected Retirees Life After Retirement at National Health Insurance Fund Dodoma HeadquarterDocument5 pagesThe Influence of Training On Expected Retirees Life After Retirement at National Health Insurance Fund Dodoma HeadquarterInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Informal Sector WorkersDocument16 pagesInformal Sector WorkersNawang WulanNo ratings yet

- IIM Shillong Group1LDocument4 pagesIIM Shillong Group1LVikas GoyalNo ratings yet

- List of Union Government Schemes in IndiaDocument10 pagesList of Union Government Schemes in IndiaRaya SahaNo ratings yet

- Apy BrochureDocument2 pagesApy BrochureBarun Kumar SinghNo ratings yet

- Lao Challenges Social ProtectionDocument3 pagesLao Challenges Social ProtectionRuby GarciaNo ratings yet

- Final Published PaperDocument3 pagesFinal Published PaperbhagatsupriyaNo ratings yet

- Dissertation of NPSDocument46 pagesDissertation of NPSDebasis BeheraNo ratings yet

- Pension Superannuation Allowance Indexation in Ghana: Reality or Myth?Document10 pagesPension Superannuation Allowance Indexation in Ghana: Reality or Myth?hayatudin jusufNo ratings yet

- An Analysis of The Reasons For Voluntary Retirement: R.K. Suri PoonamDocument6 pagesAn Analysis of The Reasons For Voluntary Retirement: R.K. Suri PoonamSagarika MazumderNo ratings yet

- TheSun 2009-07-24 Page13 CDRC Resumes Operations To Resolve Debt WoesDocument1 pageTheSun 2009-07-24 Page13 CDRC Resumes Operations To Resolve Debt WoesImpulsive collector100% (2)

- Review of Pension Schemes in IndiaDocument46 pagesReview of Pension Schemes in Indiashreya ahujaNo ratings yet

- New Pension Scheme (NPS) : - The Road Ahead and Future ChallengesDocument7 pagesNew Pension Scheme (NPS) : - The Road Ahead and Future ChallengesvikmateNo ratings yet

- (FIN) 2020552075 - FERYANDA UTAMI - Final DefenseDocument24 pages(FIN) 2020552075 - FERYANDA UTAMI - Final DefenseFeryanda UtamiNo ratings yet

- Giz2015 en Enabling Informal Workers To Access Social SecurityDocument14 pagesGiz2015 en Enabling Informal Workers To Access Social SecurityFlornats NatividadNo ratings yet

- Pension Topic One and TwoDocument7 pagesPension Topic One and Twonogarap767No ratings yet

- FINO Working ModelDocument11 pagesFINO Working ModelNeha ThakkarNo ratings yet

- Employee Provident Fund Scheme: Boon or BaneDocument8 pagesEmployee Provident Fund Scheme: Boon or BaneAkash PanigrahiNo ratings yet

- NSSF Amendment Bill Tweet Chat ReportDocument4 pagesNSSF Amendment Bill Tweet Chat ReportBrian R. NagangaNo ratings yet

- Ageing Workforce Singapore StrategiesDocument38 pagesAgeing Workforce Singapore StrategiesjoeyjocoleNo ratings yet

- IC 83 - Compressed-5Document50 pagesIC 83 - Compressed-5purnachandrashee1No ratings yet

- Evaluation of Existing Schemes of Provident Funds in India: Late R.S. KaushikDocument14 pagesEvaluation of Existing Schemes of Provident Funds in India: Late R.S. KaushikRajat GuptaNo ratings yet

- ABC - NPS ProductDocument20 pagesABC - NPS ProductdeepanadhiNo ratings yet

- 22721-Article Text-33589-1-10-20201001Document7 pages22721-Article Text-33589-1-10-20201001Tsani Aufa Wibowo putra S.SosNo ratings yet

- International DevelopmentDocument4 pagesInternational DevelopmentMalkit SinghNo ratings yet

- Retirement PlanningDocument33 pagesRetirement PlanningVISHAKHA SHUKLA 182922450% (2)

- L31 - The Instability of Commercial Microfinance in IndiaDocument27 pagesL31 - The Instability of Commercial Microfinance in IndiaYATHARTH AGARWALNo ratings yet

- CPT Syllabus For Mid SemesterDocument1 pageCPT Syllabus For Mid SemesterYATHARTH AGARWALNo ratings yet

- Birla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionDocument3 pagesBirla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionYATHARTH AGARWALNo ratings yet

- CPT Critical PathDocument72 pagesCPT Critical PathYATHARTH AGARWALNo ratings yet

- L21 - Grey Shades of Sugar Policies in IndiaDocument9 pagesL21 - Grey Shades of Sugar Policies in IndiaYATHARTH AGARWALNo ratings yet

- L24 - Some Concerns Regarding The Goods and Services TaxDocument11 pagesL24 - Some Concerns Regarding The Goods and Services TaxYATHARTH AGARWALNo ratings yet

- Topic 1Document9 pagesTopic 1YATHARTH AGARWALNo ratings yet

- Investmen T Memorandu M: Team IndusDocument44 pagesInvestmen T Memorandu M: Team IndusYATHARTH AGARWALNo ratings yet

- Himalayan BlunderDocument2 pagesHimalayan Blunderdhirajagarwal1989No ratings yet

- App Econ DataDocument3 pagesApp Econ DataYATHARTH AGARWALNo ratings yet

- CPT PROJECT REVIEW - GuidelinesDocument2 pagesCPT PROJECT REVIEW - GuidelinesYATHARTH AGARWALNo ratings yet

- App Econ DataDocument3 pagesApp Econ DataYATHARTH AGARWALNo ratings yet

- Outstanding Shares 4495 M 323 M: Closing Share PricesDocument1 pageOutstanding Shares 4495 M 323 M: Closing Share PricesYATHARTH AGARWALNo ratings yet

- DSR Horticulture 2018 PDFDocument436 pagesDSR Horticulture 2018 PDFB S Verma100% (1)

- Outstanding Shares 4495 M 323 M: Closing Share PricesDocument1 pageOutstanding Shares 4495 M 323 M: Closing Share PricesYATHARTH AGARWALNo ratings yet

- Ce F242 1192Document3 pagesCe F242 1192YATHARTH AGARWALNo ratings yet

- Ce F243 1193Document2 pagesCe F243 1193YATHARTH AGARWALNo ratings yet

- Birla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionDocument3 pagesBirla Institute of Technology and Science, Pilani: Pilani Campus AUGS/ AGSR DivisionYATHARTH AGARWALNo ratings yet

- Ce F243 1193Document2 pagesCe F243 1193YATHARTH AGARWALNo ratings yet

- ContractDocument3 pagesContracthamidu athumaniNo ratings yet

- Company Final Account FormatDocument3 pagesCompany Final Account FormatAli RangwalaNo ratings yet

- Exercises On Topic 1 (Answers)Document4 pagesExercises On Topic 1 (Answers)Anis NabilaNo ratings yet

- Social Security PDFDocument48 pagesSocial Security PDFARVIND SHARMANo ratings yet

- You Must Take Care of Your Responsibilities While Building Your WealthDocument8 pagesYou Must Take Care of Your Responsibilities While Building Your WealthAntonio C. CayetanoNo ratings yet

- Viking Catering AG: Fixed-Term (Seasonal) Contract of EmploymentDocument2 pagesViking Catering AG: Fixed-Term (Seasonal) Contract of EmploymentДимитров ЛюбомирNo ratings yet

- The Employees' Pension SchemeDocument2 pagesThe Employees' Pension SchemeSk SahilNo ratings yet

- Tenth Edition: Discretionary BenefitsDocument50 pagesTenth Edition: Discretionary BenefitsJanice YeohNo ratings yet

- International Student Application For Financial Assistance 2022 11.05.2021Document7 pagesInternational Student Application For Financial Assistance 2022 11.05.2021Samuel AduNo ratings yet

- Summary of Final Income TaxDocument7 pagesSummary of Final Income TaxeysiNo ratings yet

- NY CA 01-01-1953 9984 TXPRDocument98 pagesNY CA 01-01-1953 9984 TXPRAdmin OfficeNo ratings yet

- May Payslip JamesDocument1 pageMay Payslip JamesJames PuckeyNo ratings yet

- TAXATION 1 Transcripts - Atty. KMA - A.Y. 2020 - 2021Document52 pagesTAXATION 1 Transcripts - Atty. KMA - A.Y. 2020 - 2021Vincent John NacuaNo ratings yet

- Indian Income Tax Return: (Refer Instructions For Eligibility)Document6 pagesIndian Income Tax Return: (Refer Instructions For Eligibility)Chief Engineer Hydro Project & Quality ControlNo ratings yet

- Chapter 3Document12 pagesChapter 3geexellNo ratings yet

- Tds and Tcs Under Income TaxDocument60 pagesTds and Tcs Under Income TaxAbhishek MogaveeraNo ratings yet

- FTF 2022-03-23 1648079099327Document14 pagesFTF 2022-03-23 1648079099327Charles Goodwin100% (1)

- Mahatharsnedevi 202009Document1 pageMahatharsnedevi 202009Mahatharsnedevi RavindranNo ratings yet

- INCOME TAXATION Chap 5 PG (184-192) PDFDocument2 pagesINCOME TAXATION Chap 5 PG (184-192) PDFnazarene moralesNo ratings yet

- 2019 Tax Card PakistanDocument9 pages2019 Tax Card PakistanRaja Hamza rasgNo ratings yet

- Marie Aladin 2019 Tax PDFDocument60 pagesMarie Aladin 2019 Tax PDFPrint Copy100% (1)

- Free Project Budget FormDocument2 pagesFree Project Budget FormFEYIBUNMI RUTHNo ratings yet

- Name Course Date: Case Study For Individual PaperDocument11 pagesName Course Date: Case Study For Individual PaperajayNo ratings yet

- March 2023 CapgeminiDocument1 pageMarch 2023 CapgeminimanojkallemuchikkalNo ratings yet

- Delta Airlines Case StudyDocument4 pagesDelta Airlines Case Studynrmpz9b54dNo ratings yet

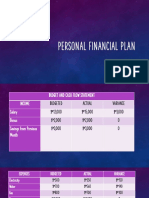

- Personal Financial PlanDocument6 pagesPersonal Financial PlanThomgie TilaNo ratings yet

- Declaration Form 12BB 2022 23Document4 pagesDeclaration Form 12BB 2022 23S S PradheepanNo ratings yet

- Uoi V Amrita Sinha 406131Document7 pagesUoi V Amrita Sinha 406131Manager PersonnelkptclNo ratings yet

- Life Insurance Corporation - LIC: Introduction To Insurance and Its Fundamental PrinciplesDocument40 pagesLife Insurance Corporation - LIC: Introduction To Insurance and Its Fundamental Principlesksaqib89No ratings yet

- Helpro Loan Application FormDocument2 pagesHelpro Loan Application FormKhiann AbaisNo ratings yet

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesFrom EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesRating: 4 out of 5 stars4/5 (9)

- How to get US Bank Account for Non US ResidentFrom EverandHow to get US Bank Account for Non US ResidentRating: 5 out of 5 stars5/5 (1)

- Lower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2019-2020: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderRating: 5 out of 5 stars5/5 (4)

- The Hidden Wealth of Nations: The Scourge of Tax HavensFrom EverandThe Hidden Wealth of Nations: The Scourge of Tax HavensRating: 4 out of 5 stars4/5 (11)

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderFrom EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderNo ratings yet

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesFrom EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNo ratings yet

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyFrom EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyNo ratings yet

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsFrom EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsNo ratings yet

- The Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsFrom EverandThe Tax and Legal Playbook: Game-Changing Solutions To Your Small Business QuestionsRating: 3.5 out of 5 stars3.5/5 (9)

- Invested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)From EverandInvested: How I Learned to Master My Mind, My Fears, and My Money to Achieve Financial Freedom and Live a More Authentic Life (with a Little Help from Warren Buffett, Charlie Munger, and My Dad)Rating: 4.5 out of 5 stars4.5/5 (43)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Bookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessFrom EverandBookkeeping: Step by Step Guide to Bookkeeping Principles & Basic Bookkeeping for Small BusinessRating: 5 out of 5 stars5/5 (5)

- Taxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipFrom EverandTaxes for Small Business: The Ultimate Guide to Small Business Taxes Including LLC Taxes, Payroll Taxes, and Self-Employed Taxes as a Sole ProprietorshipNo ratings yet

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCFrom EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCRating: 4 out of 5 stars4/5 (5)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Deduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesFrom EverandDeduct Everything!: Save Money with Hundreds of Legal Tax Breaks, Credits, Write-Offs, and LoopholesRating: 3 out of 5 stars3/5 (3)

- Founding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationFrom EverandFounding Finance: How Debt, Speculation, Foreclosures, Protests, and Crackdowns Made Us a NationNo ratings yet

- LLC Startup 2023: How to Create Financial Freedom Through Launching a Successful Small Business. From Creating a Business Plan for the Limited Liability Company to Turning the Vision into a Reality.From EverandLLC Startup 2023: How to Create Financial Freedom Through Launching a Successful Small Business. From Creating a Business Plan for the Limited Liability Company to Turning the Vision into a Reality.No ratings yet

- Tax Savvy for Small Business: A Complete Tax Strategy GuideFrom EverandTax Savvy for Small Business: A Complete Tax Strategy GuideRating: 5 out of 5 stars5/5 (1)

- Freight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesFrom EverandFreight Broker Business Startup: Step-by-Step Guide to Start, Grow and Run Your Own Freight Brokerage Company In in Less Than 4 Weeks. Includes Business Plan TemplatesRating: 5 out of 5 stars5/5 (1)