You might also like

- G20/The Oecd Principles of Corporate GovernanceDocument35 pagesG20/The Oecd Principles of Corporate GovernanceNino MdinaradzeNo ratings yet

- G20-OECD Principles of CGDocument3 pagesG20-OECD Principles of CGSherry LaiNo ratings yet

- Assignment in GovernanceDocument10 pagesAssignment in GovernanceCyrus Joshua SargentoNo ratings yet

- Basel Committee Principles Guide Bank GovernanceDocument8 pagesBasel Committee Principles Guide Bank Governanceprajwal shresthaNo ratings yet

- Improving Corporate Governance in NepalDocument4 pagesImproving Corporate Governance in NepalAzula AzulaNo ratings yet

- Corporate Governance Principles IIMK Vidhu ShekharDocument26 pagesCorporate Governance Principles IIMK Vidhu ShekharBalachandra MallyaNo ratings yet

- CG AnalysisDocument5 pagesCG AnalysisCHETHAN KUMAR N 17BBLB012No ratings yet

- The Oecd Principles of Corporate GovernanceDocument8 pagesThe Oecd Principles of Corporate GovernanceNazifaNo ratings yet

- CG 1Document28 pagesCG 1saran muralidaranNo ratings yet

- Code of CG China EngDocument15 pagesCode of CG China EngbilalNo ratings yet

- OECD Corporate Governance Principles SummaryDocument2 pagesOECD Corporate Governance Principles Summarysetti100% (1)

- Sebi Frame WorkDocument3 pagesSebi Frame WorkdushyantNo ratings yet

- Introduction to Corporate Governance Principles and PillarsDocument11 pagesIntroduction to Corporate Governance Principles and Pillarsqari saib100% (3)

- Part 1 of Module I GBERMICDocument12 pagesPart 1 of Module I GBERMICjhie boterNo ratings yet

- Corporate Governance: Governance, Business Ethics, Risk Management, and Internal ControlDocument26 pagesCorporate Governance: Governance, Business Ethics, Risk Management, and Internal ControlPipz G. CastroNo ratings yet

- Corporate GovernanceDocument14 pagesCorporate Governanceeshu agNo ratings yet

- CorpGov SECDocument53 pagesCorpGov SECPipz G. CastroNo ratings yet

- Corporate Governance Principles and PracticesDocument180 pagesCorporate Governance Principles and PracticesPauline Rose AnnNo ratings yet

- Corporate Governance and Social ResponsibilityDocument7 pagesCorporate Governance and Social ResponsibilityMohitNo ratings yet

- CG PrinciplesDocument18 pagesCG PrinciplesManikant SinghaniaNo ratings yet

- OECD - 2015, Priciple 1Document3 pagesOECD - 2015, Priciple 1NataliaNo ratings yet

- Protection of Stakeholders' RightsDocument5 pagesProtection of Stakeholders' RightsJayveerose BorjaNo ratings yet

- OECD PrinciplesDocument1 pageOECD PrinciplesRebel X HamzaNo ratings yet

- Lecture 3Document4 pagesLecture 3ayamaher3323No ratings yet

- Ethics Module5Document17 pagesEthics Module5Krishna Chandran PallippuramNo ratings yet

- Cultivating A Synergic Relationship With ShareholdersDocument6 pagesCultivating A Synergic Relationship With ShareholdersJeric Lagyaban AstrologioNo ratings yet

- Corporate GovernanceDocument10 pagesCorporate GovernanceMarwah FaisalNo ratings yet

- Prinsip Corporate GovernanceDocument20 pagesPrinsip Corporate GovernanceMuhammad Vakollad WibowoNo ratings yet

- Shareholder RightsDocument4 pagesShareholder RightsJayveerose BorjaNo ratings yet

- Code of Corporate Governance For Publicly-Listed CompaniesDocument41 pagesCode of Corporate Governance For Publicly-Listed CompaniesTherese Janine HetutuaNo ratings yet

- Japan's Corporate Governance CodeDocument32 pagesJapan's Corporate Governance CodeCerio DuroNo ratings yet

- F - G20 OECD Principles of Corporate Governance (31-35)Document5 pagesF - G20 OECD Principles of Corporate Governance (31-35)Ivonie NursalimNo ratings yet

- Corporate Governance: Presented byDocument36 pagesCorporate Governance: Presented bymala singhNo ratings yet

- Ethics and Corporate GovernanaceDocument3 pagesEthics and Corporate GovernanaceAditya MishraNo ratings yet

- AE10 MidTerm ExamDocument3 pagesAE10 MidTerm ExamAnne SotalboNo ratings yet

- International Governance Is A Movement Towards Political Cooperation Among TransnationalDocument6 pagesInternational Governance Is A Movement Towards Political Cooperation Among TransnationalWenjun100% (4)

- Corporate Governance and Social Responsibility Assignment: Name: Ravneet Rehal 2 Year Section A Roll No. 36Document14 pagesCorporate Governance and Social Responsibility Assignment: Name: Ravneet Rehal 2 Year Section A Roll No. 36ravneetNo ratings yet

- G20/Oecd Principles of Corporate GovernanceDocument6 pagesG20/Oecd Principles of Corporate GovernancejuanNo ratings yet

- What Is Governance?Document8 pagesWhat Is Governance?Aaron Josua AboyNo ratings yet

- Governance Midterms PDFDocument71 pagesGovernance Midterms PDFRyan Canatuan100% (1)

- Corporate Governance EssentialsDocument16 pagesCorporate Governance EssentialsIqbal HanifNo ratings yet

- Ethics & Corporate GovernanceDocument2 pagesEthics & Corporate Governancecriss BasigaraNo ratings yet

- Governance Question and AnswersDocument14 pagesGovernance Question and AnswersCeline Joy PolicarpioNo ratings yet

- Corporate Governance BasicsDocument8 pagesCorporate Governance BasicsNicefebe Love SampanNo ratings yet

- Grup 4 - Etika - Tata KelolaDocument26 pagesGrup 4 - Etika - Tata KelolaAzami Indarabbi ZulfanNo ratings yet

- Corporate GovernanceDocument133 pagesCorporate GovernanceAman Dheer Kapoor100% (1)

- GovernanceDocument13 pagesGovernancePixie CanaveralNo ratings yet

- Corporate Governance PDFDocument6 pagesCorporate Governance PDFriyasacademicNo ratings yet

- CH10 Corporate GovernanceDocument2 pagesCH10 Corporate Governancemissalali3No ratings yet

- UK Stewardship Code 2012Document22 pagesUK Stewardship Code 2012Twinkle SinghNo ratings yet

- Business Ethics and Corporate Governance (Session-1)Document15 pagesBusiness Ethics and Corporate Governance (Session-1)Sharad TapasviNo ratings yet

- Overview of Governance Governance in GeneralDocument5 pagesOverview of Governance Governance in GeneralJohn Michael GeneralNo ratings yet

- Assignment On Code of Corporate Governance.Document6 pagesAssignment On Code of Corporate Governance.Md Al ArafatNo ratings yet

- Chapter 10Document8 pagesChapter 10Haroon RasheedNo ratings yet

- Lecture 1Document7 pagesLecture 1Marielle UyNo ratings yet

- HERMES International CG PrinciplesDocument2 pagesHERMES International CG PrinciplesEnnayojaravNo ratings yet

- Need of Corporate GovernanceDocument3 pagesNeed of Corporate GovernanceAmmy k100% (1)

- OECD GOVERNANCEDocument29 pagesOECD GOVERNANCEEvita RuslimNo ratings yet

- Corporate GovernanceDocument8 pagesCorporate GovernanceSanjay Kumar VaniyanNo ratings yet

- Insert Faculty Name Insert Your Name Insert School or Program NameDocument1 pageInsert Faculty Name Insert Your Name Insert School or Program NameAnkit SangwanNo ratings yet

- MAP Undergrad With Cover - 0Document27 pagesMAP Undergrad With Cover - 0Ankit SangwanNo ratings yet

- Lab Activity Report Submitted For Network Security (UCS610) : Thapar Institute of Engineering and TechnologyDocument1 pageLab Activity Report Submitted For Network Security (UCS610) : Thapar Institute of Engineering and TechnologyAnkit SangwanNo ratings yet

- Join Net Impact Chapter, Help Turn Passion Into Lifelong ActionDocument7 pagesJoin Net Impact Chapter, Help Turn Passion Into Lifelong ActionAnkit SangwanNo ratings yet

- Student Recruitment LetterDocument1 pageStudent Recruitment LetterAnkit SangwanNo ratings yet

- 1a PhotochemistryDocument8 pages1a PhotochemistryAnkit SangwanNo ratings yet

- Screw Friction PDFDocument6 pagesScrew Friction PDFAnkit SangwanNo ratings yet

- Mechanics Project - HandoutDocument2 pagesMechanics Project - HandoutAadi SharmaNo ratings yet

- Steps To Do Simulation in Mentor GraphicsDocument7 pagesSteps To Do Simulation in Mentor GraphicsAnkit SangwanNo ratings yet

- Components Required For Line Follower PDFDocument3 pagesComponents Required For Line Follower PDFAnkit SangwanNo ratings yet

- DESIGN OF A TRUSS BRIDGE (UES009 PROJECT - YOU TUBE LINKS) - UPDATED SachinDocument25 pagesDESIGN OF A TRUSS BRIDGE (UES009 PROJECT - YOU TUBE LINKS) - UPDATED SachinAnkit SangwanNo ratings yet

- Atomic Absorption Spectroscopy: Sodium atom absorb at a wavelength of 589 nm. What is the energy difference between (in J) between the ground and excited stateDocument28 pagesAtomic Absorption Spectroscopy: Sodium atom absorb at a wavelength of 589 nm. What is the energy difference between (in J) between the ground and excited statepulkit chughNo ratings yet

- Lecture 2 PDFDocument7 pagesLecture 2 PDFAnkit SangwanNo ratings yet

- Electrochemistry Lecture 1Document43 pagesElectrochemistry Lecture 1Ankit SangwanNo ratings yet

- Hall-Effect Sensor: 1,2,3 Are The Leg Numbers We See Protruding Out of The SensorDocument2 pagesHall-Effect Sensor: 1,2,3 Are The Leg Numbers We See Protruding Out of The SensorAnkit SangwanNo ratings yet

- Hall-Effect Sensor: 1,2,3 Are The Leg Numbers We See Protruding Out of The SensorDocument2 pagesHall-Effect Sensor: 1,2,3 Are The Leg Numbers We See Protruding Out of The SensorAnkit SangwanNo ratings yet

- Mechanics Notes PDFDocument51 pagesMechanics Notes PDFAnkit SangwanNo ratings yet

- Nitin - ProjectDocument19 pagesNitin - ProjectAnkit SangwanNo ratings yet

- Lecture 3 PDFDocument6 pagesLecture 3 PDFAnkit SangwanNo ratings yet

- Lecture 1 PDFDocument7 pagesLecture 1 PDFAnkit SangwanNo ratings yet

- Arduino and Microcontrollers PDFDocument33 pagesArduino and Microcontrollers PDFAnkit SangwanNo ratings yet

- Engineering Exams: S. No. Name Start Date End DateDocument2 pagesEngineering Exams: S. No. Name Start Date End DateAnkit SangwanNo ratings yet

- Lecture 4 PDFDocument6 pagesLecture 4 PDFAnkit SangwanNo ratings yet

- MP 29 Soldering PDFDocument19 pagesMP 29 Soldering PDFAnkit SangwanNo ratings yet

- Nitin - KFA, Satyam, Enron PDFDocument7 pagesNitin - KFA, Satyam, Enron PDFAnkit SangwanNo ratings yet

- Nitin - Harshad Mehta Scam PDFDocument12 pagesNitin - Harshad Mehta Scam PDFAnkit SangwanNo ratings yet

- UEC 404 Tutorial 4 Solutin PDFDocument11 pagesUEC 404 Tutorial 4 Solutin PDFAnkit SangwanNo ratings yet

- S. No. Exam Exam App Date Exam Date College & Counseling Result Date Counsellin G App Date Counselling DateDocument3 pagesS. No. Exam Exam App Date Exam Date College & Counseling Result Date Counsellin G App Date Counselling DateAnkit SangwanNo ratings yet

- Experiment: 6 ObjectiveDocument5 pagesExperiment: 6 ObjectiveAnkit SangwanNo ratings yet

- 5.-SIANEN Nego Case-DigestDocument53 pages5.-SIANEN Nego Case-DigestEarl Justine OcuamanNo ratings yet

- Technical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEDocument30 pagesTechnical Note On LBO Valuation and Modeling - 150309 - 4!10!2015 - SAMPLEJayant Sharma100% (1)

- PSE Guide: Investing in Philippine StocksDocument6 pagesPSE Guide: Investing in Philippine StocksDennisOlayresNocomoraNo ratings yet

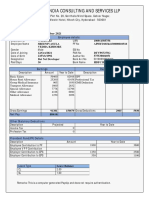

- Purview India Consulting and Services LLPDocument1 pagePurview India Consulting and Services LLPmamatha vemulaNo ratings yet

- Pettet, Lowry & Reisberg's Company Law '12Document657 pagesPettet, Lowry & Reisberg's Company Law '12mamahannatuadamu100% (1)

- 2018 Immunization Case - QuestionDocument2 pages2018 Immunization Case - QuestionSofia LimaNo ratings yet

- CAE 14 - RevalidaDocument4 pagesCAE 14 - RevalidaTifanny MallariNo ratings yet

- Benefit Illustration For HDFC Life Sanchay Par AdvantageDocument3 pagesBenefit Illustration For HDFC Life Sanchay Par Advantagekesk32No ratings yet

- CEO Compesation: Presentation OnDocument11 pagesCEO Compesation: Presentation OnEra ChaudharyNo ratings yet

- Tài liệu ôn thi TACN 2Document34 pagesTài liệu ôn thi TACN 2Trần Trung CườngNo ratings yet

- Internship Report On "Loan Disbursement Procedure of Grameen Bank "Document38 pagesInternship Report On "Loan Disbursement Procedure of Grameen Bank "Boby PodderNo ratings yet

- Chapter 5 - Health Insurance SchemesDocument0 pagesChapter 5 - Health Insurance SchemesJonathon CabreraNo ratings yet

- AttachmentDocument95 pagesAttachmentSyed InamNo ratings yet

- Assertions in The Audit of Financial StatementsDocument4 pagesAssertions in The Audit of Financial StatementsAselleNo ratings yet

- Wabwire Arnold ReportDocument29 pagesWabwire Arnold ReportFAITH WANYOIKENo ratings yet

- Branch and Unit BankingDocument1 pageBranch and Unit BankingSheetal Thomas100% (1)

- Republic Planters Bank v. Court of Appeals 216 SCRA 738 (1992) PDFDocument4 pagesRepublic Planters Bank v. Court of Appeals 216 SCRA 738 (1992) PDFJulie Rose FajardoNo ratings yet

- IIML Stratos Competition GuidelinesDocument12 pagesIIML Stratos Competition GuidelinessharadvasistaNo ratings yet

- Debt Management in IndiaDocument3 pagesDebt Management in IndiaSarbartho MukherjeeNo ratings yet

- Fixedline and Broadband Services: Your Account Summary This Month'S ChargesDocument2 pagesFixedline and Broadband Services: Your Account Summary This Month'S ChargesMaximuzNo ratings yet

- Capital and Revenue ExpenditureDocument87 pagesCapital and Revenue ExpenditurefatynssvNo ratings yet

- List of Courses OfferedDocument170 pagesList of Courses OfferedSam100% (1)

- General Principles & National Income Taxation Lecture Atty RizalinaDocument242 pagesGeneral Principles & National Income Taxation Lecture Atty RizalinaJoyce LapuzNo ratings yet

- Capital Structure Test QuestionsDocument28 pagesCapital Structure Test QuestionsSardonna FongNo ratings yet

- MHA Syllabus for Hospital Administration ProgrammeDocument29 pagesMHA Syllabus for Hospital Administration ProgrammeDrPoonam ValviNo ratings yet

- 2023 - FRM - PI - PE2 - 020223 - CleanDocument171 pages2023 - FRM - PI - PE2 - 020223 - CleanRaymond Kwong100% (1)

- Bank Winter BG MT760 - GuaranteeDocument2 pagesBank Winter BG MT760 - GuaranteeLaz Cozetat100% (2)

- Investor scheme transaction recordsDocument1,795 pagesInvestor scheme transaction recordsIndranilGhoshNo ratings yet

- Illustrative Problem On Acquisition of Net Assets: Entity XY Entity ABDocument2 pagesIllustrative Problem On Acquisition of Net Assets: Entity XY Entity ABjerald cerezaNo ratings yet

- Invoice 26Document2 pagesInvoice 26asim khanNo ratings yet

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsFrom EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsRating: 5 out of 5 stars5/5 (24)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- Legal Guide for Starting & Running a Small BusinessFrom EverandLegal Guide for Starting & Running a Small BusinessRating: 4.5 out of 5 stars4.5/5 (9)

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- Building Your Empire: Achieve Financial Freedom with Passive IncomeFrom EverandBuilding Your Empire: Achieve Financial Freedom with Passive IncomeNo ratings yet

- Competition and Antitrust Law: A Very Short IntroductionFrom EverandCompetition and Antitrust Law: A Very Short IntroductionRating: 5 out of 5 stars5/5 (3)

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)

- Indian Polity with Indian Constitution & Parliamentary AffairsFrom EverandIndian Polity with Indian Constitution & Parliamentary AffairsNo ratings yet

- The Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysFrom EverandThe Real Estate Investing Diet: Harnessing Health Strategies to Build Wealth in Ninety DaysNo ratings yet

- The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicFrom EverandThe Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicRating: 5 out of 5 stars5/5 (1)

- Economics and the Law: From Posner to Postmodernism and Beyond - Second EditionFrom EverandEconomics and the Law: From Posner to Postmodernism and Beyond - Second EditionRating: 1 out of 5 stars1/5 (1)