You might also like

- CFR-Charting The Future of Global DevelopmentDocument3 pagesCFR-Charting The Future of Global DevelopmentVishal PandeyNo ratings yet

- 2025 Global GovernanceDocument82 pages2025 Global GovernancePaco CapellaNo ratings yet

- Put Globalization To Work For Democracies: OpinionDocument5 pagesPut Globalization To Work For Democracies: OpinionKyla NiagaNo ratings yet

- Escaping The Fragility TrapDocument79 pagesEscaping The Fragility TrapJose Luis Bernal MantillaNo ratings yet

- Covid 19.editedDocument3 pagesCovid 19.editedUswork tobuzyNo ratings yet

- Angielica N. Rabago Ii-Bstm Activity No. 1Document4 pagesAngielica N. Rabago Ii-Bstm Activity No. 1Clerk Janly R FacunlaNo ratings yet

- Open Economies, Responsible Global Governance, Corporate LeadershipDocument4 pagesOpen Economies, Responsible Global Governance, Corporate LeadershippalestallarNo ratings yet

- The New World Order Great ResetDocument1 pageThe New World Order Great Resetjerry smithNo ratings yet

- Role of India in The Global World During & Post COVID19 Essay AmanDocument4 pagesRole of India in The Global World During & Post COVID19 Essay AmanVinayak kumbharNo ratings yet

- Drezner The Irony of Global Governance 2012Document25 pagesDrezner The Irony of Global Governance 2012Ivana SilvaNo ratings yet

- Tập Bài Đọc Global ReadingDocument40 pagesTập Bài Đọc Global ReadingLY PHẠM THỊ THẢONo ratings yet

- Does Globalization Help or Hurt (Sci Am 2006)Document3 pagesDoes Globalization Help or Hurt (Sci Am 2006)FRANCISCO JAVIER ESTRADA ORD��EZNo ratings yet

- IPE J Jan 25Document3 pagesIPE J Jan 25Paula AchimNo ratings yet

- Globalization Is FinishedDocument3 pagesGlobalization Is FinishedziaNo ratings yet

- Politics & The Nation: This GraphicDocument4 pagesPolitics & The Nation: This Graphicahcir2790No ratings yet

- Socsci 10Document4 pagesSocsci 10Celestine MambulaoNo ratings yet

- Article Martin Wolf GlobalisationDocument9 pagesArticle Martin Wolf GlobalisationmariaNo ratings yet

- Economics HardDocument18 pagesEconomics HardMohammad Redo AsgharNo ratings yet

- Reaping The Benefits of GlobalizationDocument8 pagesReaping The Benefits of GlobalizationFelis_Demulcta_MitisNo ratings yet

- On The Cusp of Change Reforming Bretton Woods Institutions and The WTODocument4 pagesOn The Cusp of Change Reforming Bretton Woods Institutions and The WTOMikhailNo ratings yet

- What Is Deglobalization and How It Impacts Global Value Chains?Document6 pagesWhat Is Deglobalization and How It Impacts Global Value Chains?Krishan FernandoNo ratings yet

- Covid-19 and GlobalizationDocument4 pagesCovid-19 and Globalizationmukul baijalNo ratings yet

- EITIFocus 2012Document30 pagesEITIFocus 2012Hanafi Aba HakkanNo ratings yet

- Ten Questions Posed by The Virus - The HinduDocument4 pagesTen Questions Posed by The Virus - The HinduVISHISHT BAISNo ratings yet

- 02 2011 HA JOON CHANG Institutions and Economic Development - En.ptDocument26 pages02 2011 HA JOON CHANG Institutions and Economic Development - En.ptDay Mika'sNo ratings yet

- Put Globalization To Work For Democracies: by Dani RodrikDocument3 pagesPut Globalization To Work For Democracies: by Dani RodrikGel MaangasNo ratings yet

- A Post-Coronavirus World: 7 Points of Discussion For A New Political EconomyDocument19 pagesA Post-Coronavirus World: 7 Points of Discussion For A New Political EconomyMiranda LarazNo ratings yet

- Session 2 - Soc Sci 3 Digitized ActivityDocument4 pagesSession 2 - Soc Sci 3 Digitized ActivityjovesrhonalyneNo ratings yet

- The Post Covid-19 World - BEDocument4 pagesThe Post Covid-19 World - BEManisha KumariNo ratings yet

- Innovation in Asia's Reinsurance Market - Anant Srivastva - IndiaDocument7 pagesInnovation in Asia's Reinsurance Market - Anant Srivastva - Indiaanant_srivastvaNo ratings yet

- Essay 1: National Sovereignty Alone Cannot Govern Global Flows of People, Goods and Services - Transnational Institutions Are Still NecessaryDocument3 pagesEssay 1: National Sovereignty Alone Cannot Govern Global Flows of People, Goods and Services - Transnational Institutions Are Still NecessaryLydiaNo ratings yet

- Political Economy Research Paper TopicsDocument4 pagesPolitical Economy Research Paper Topicsaflbskroi100% (1)

- GlobalizationDocument6 pagesGlobalizationSanskruti PathakNo ratings yet

- Globalization Trade and Commerce Allover The World by Creating A Border Less MarketDocument28 pagesGlobalization Trade and Commerce Allover The World by Creating A Border Less MarketMd.Najmul HasanNo ratings yet

- The Intent To Establish A Global GovernmentDocument3 pagesThe Intent To Establish A Global GovernmentoasdafNo ratings yet

- MIDTERM EXAMINATION SocioDocument4 pagesMIDTERM EXAMINATION SocioMahusay Neil DominicNo ratings yet

- FightingGlobPov PageDocument16 pagesFightingGlobPov PageJ. Félix Angulo RascoNo ratings yet

- Chang 2011 Institutions - and - Economic - Development - Theory - Policy - and - HistoryDocument26 pagesChang 2011 Institutions - and - Economic - Development - Theory - Policy - and - HistoryMarvin MirandaNo ratings yet

- Development EconomicsDocument6 pagesDevelopment EconomicsDonboss LaitonjamNo ratings yet

- How To Lead in Ambiguous Times: Leaves Little DoubtDocument10 pagesHow To Lead in Ambiguous Times: Leaves Little DoubtQueenie Marie Obial AlasNo ratings yet

- Stimulus PacakgaesDocument4 pagesStimulus PacakgaesrajoocyberNo ratings yet

- How To Reform Today's Rigged CapitalismDocument8 pagesHow To Reform Today's Rigged CapitalismLuanaBessaNo ratings yet

- RIS - Diary Covid 19 FinalDocument16 pagesRIS - Diary Covid 19 FinalSoumojit KumarNo ratings yet

- Development 6Document32 pagesDevelopment 6Awetahegn HagosNo ratings yet

- Presidential Address Does Finance Benefit SocietyDocument39 pagesPresidential Address Does Finance Benefit Societya lNo ratings yet

- Streeten Paul Pak Dev Rev 37 (4) 51-83Document47 pagesStreeten Paul Pak Dev Rev 37 (4) 51-83River RiverNo ratings yet

- Jurnal CorporateDocument16 pagesJurnal CorporateRatih Frayunita SariNo ratings yet

- From Poverty To Empowerment Executive Summary September 2023Document40 pagesFrom Poverty To Empowerment Executive Summary September 2023Suparna Aryabrata MozumdarNo ratings yet

- Chap 1Document7 pagesChap 1Vea Roanne GammadNo ratings yet

- Etude Fondapol Josef Konvitz Paradigm Shifts 2020-24-07Document44 pagesEtude Fondapol Josef Konvitz Paradigm Shifts 2020-24-07FondapolNo ratings yet

- Constructing A New Global Order: A Project Framing DocumentDocument22 pagesConstructing A New Global Order: A Project Framing DocumentPedro MoltedoNo ratings yet

- Md. Noor Alam - (3-20-44-021) - Asignment On - Is This The Future of Globalisation Look LikeDocument4 pagesMd. Noor Alam - (3-20-44-021) - Asignment On - Is This The Future of Globalisation Look LikeNoor AlamNo ratings yet

- China Economy DissertationDocument8 pagesChina Economy DissertationCustomizedWritingPaperNewark100% (1)

- Covid-19 and Trade Policy 29 April 2020 PDFDocument200 pagesCovid-19 and Trade Policy 29 April 2020 PDFemmanuel santoyo rioNo ratings yet

- Nonprofit Asset Management: Effective Investment Strategies and OversightFrom EverandNonprofit Asset Management: Effective Investment Strategies and OversightNo ratings yet

- Resonance Economy: How resonances arise, how we can identify them and use them to our benefit.From EverandResonance Economy: How resonances arise, how we can identify them and use them to our benefit.No ratings yet

- The Nucleus Impetus Role: Inspirational and Personal Views from COVID-19 ExperienceFrom EverandThe Nucleus Impetus Role: Inspirational and Personal Views from COVID-19 ExperienceNo ratings yet

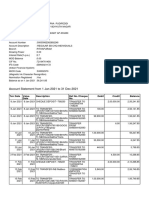

- Account Statement From 1 Jan 2021 To 31 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 1 Jan 2021 To 31 Dec 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAnnapurna PNo ratings yet

- Curbs Extended For 2 WKS, With Some EasingDocument15 pagesCurbs Extended For 2 WKS, With Some EasingAnnapurna PNo ratings yet

- Times of India 05 May 2020 DailyEpaper inDocument14 pagesTimes of India 05 May 2020 DailyEpaper inAnnapurna PNo ratings yet

- Curbs Extended For 2 WKS, With Some EasingDocument15 pagesCurbs Extended For 2 WKS, With Some EasingAnnapurna PNo ratings yet

- The Hindu Notes 09-05-2020 WWW - Job9.in PDFDocument11 pagesThe Hindu Notes 09-05-2020 WWW - Job9.in PDFSathyamoorthy VenkateshNo ratings yet

- The HINDU Notes 10-05-2020 PDFDocument10 pagesThe HINDU Notes 10-05-2020 PDFAnnapurna PNo ratings yet

- Dummy PDFDocument1 pageDummy PDFAnnapurna PNo ratings yet

- A Alys AL IS N: WWW - Job9.in WWW - Job9.inDocument15 pagesA Alys AL IS N: WWW - Job9.in WWW - Job9.inAnnapurna PNo ratings yet

- Roger A. Arnold: California State UniversityDocument15 pagesRoger A. Arnold: California State UniversityNajmul AhsanNo ratings yet

- Critical ReasoningDocument27 pagesCritical ReasoningMd parvezsharifNo ratings yet

- Reading 12 Monetary and Fiscal PolicyDocument31 pagesReading 12 Monetary and Fiscal PolicyAbhishek KundliaNo ratings yet

- CH 18 Saving, Investment, and The Financial System 9eDocument38 pagesCH 18 Saving, Investment, and The Financial System 9e민초율No ratings yet

- Economics of Money Banking and Financial Markets 9th Edition by Mishkin Test BankDocument27 pagesEconomics of Money Banking and Financial Markets 9th Edition by Mishkin Test BankĐỗ Ngọc Huyền Trang100% (1)

- Financial Markets - Nguyen Quang Anh - s3926813Document5 pagesFinancial Markets - Nguyen Quang Anh - s3926813Anthony NguyenNo ratings yet

- The Comeback Kid Comes Back AgainDocument40 pagesThe Comeback Kid Comes Back Againapi-26032005No ratings yet

- chính trị học so sánhDocument18 pageschính trị học so sánhTrần Bích Ngọc 5Q-20ACNNo ratings yet

- LtboDocument64 pagesLtboCongressman Zach NunnNo ratings yet

- Additional Practice Questions and AnswersDocument32 pagesAdditional Practice Questions and AnswersMonty Bansal100% (1)

- Understanding Economics and How It Affects BusinessDocument42 pagesUnderstanding Economics and How It Affects Businesselite writerNo ratings yet

- The Role of Financial System in DevelopmentDocument5 pagesThe Role of Financial System in DevelopmentCritical ThinkerNo ratings yet

- MCDocument127 pagesMCMadiha AshrafNo ratings yet

- The Plain Bagel Budgeting SpreadsheetDocument2 pagesThe Plain Bagel Budgeting Spreadsheetshunt18No ratings yet

- Manual March of The EaglesDocument108 pagesManual March of The EaglesSergio Díaz GuerreroNo ratings yet

- History of Indonesian Fiscal Policy 1945-1986 - The Battle For Resources (Kuntjoro-Jakti 1988)Document48 pagesHistory of Indonesian Fiscal Policy 1945-1986 - The Battle For Resources (Kuntjoro-Jakti 1988)dharendraNo ratings yet

- Bergsten & Williamson - Dollar Overvaluation and The World Economy (2003)Document331 pagesBergsten & Williamson - Dollar Overvaluation and The World Economy (2003)PatriotiKsNo ratings yet

- Business Standard - Delhi - English - 01-10-2022Document16 pagesBusiness Standard - Delhi - English - 01-10-2022Surath KrishnaNo ratings yet

- Essay Plans 1: Across The Economy and Thus Stimulate Lending, Borrowing, AD and Economic GrowthDocument24 pagesEssay Plans 1: Across The Economy and Thus Stimulate Lending, Borrowing, AD and Economic GrowthAbhishek JainNo ratings yet

- Sharpe (2014) A Modern Money Perspective On Financial Crowding OutDocument22 pagesSharpe (2014) A Modern Money Perspective On Financial Crowding OutEdwin MauricioNo ratings yet

- What Is The Role of Fiscal Policy in The EconomyDocument28 pagesWhat Is The Role of Fiscal Policy in The EconomyJackson BlackNo ratings yet

- Trend in Domestic Saving & Capital Formation in IndiaDocument43 pagesTrend in Domestic Saving & Capital Formation in IndiaYaadrahulkumar Moharana100% (3)

- Ecs2602 Tut.101.2013Document90 pagesEcs2602 Tut.101.2013YOLANDANo ratings yet

- WEC14 01 Rms UNUSEDDocument24 pagesWEC14 01 Rms UNUSEDAryan SatapathyNo ratings yet

- Monetary Policy Committee Meeting StatementDocument3 pagesMonetary Policy Committee Meeting StatementAnonymous FnM14a0No ratings yet

- The Wall Street Journal April 24 2020 PDFDocument49 pagesThe Wall Street Journal April 24 2020 PDFmuzeucojusnaNo ratings yet

- Chapter 1: Exploring The World of Business and EconomicsDocument7 pagesChapter 1: Exploring The World of Business and EconomicsDaniel WidjojoNo ratings yet

- Silicon Savannah: The Kenya ICT Services Cluster: Microeconomics of Competitiveness - Spring 2016 Prof. AlfaroDocument34 pagesSilicon Savannah: The Kenya ICT Services Cluster: Microeconomics of Competitiveness - Spring 2016 Prof. AlfaroAndres PereaNo ratings yet

- Assignment 2 COVID-19: The Global Shutdown: Case BackgroundDocument8 pagesAssignment 2 COVID-19: The Global Shutdown: Case BackgroundShubham TapadiyaNo ratings yet

- Chapter 16: Financing Government Section 1Document67 pagesChapter 16: Financing Government Section 1Aaron PaladinoNo ratings yet