You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Pearson LCCI Level 3 Certificate in Accounting (IAS) : Series 2 2013 (ASE3902)Document10 pagesPearson LCCI Level 3 Certificate in Accounting (IAS) : Series 2 2013 (ASE3902)Gloria WanNo ratings yet

- Book Keeping and Accounts Model Answer Series 3 2014Document13 pagesBook Keeping and Accounts Model Answer Series 3 2014cheah_chinNo ratings yet

- Accounting IAS Model Answers Series 3 2006 Old SyllabusDocument20 pagesAccounting IAS Model Answers Series 3 2006 Old SyllabusAung Zaw HtweNo ratings yet

- Accounting (IAS) Level 3/series 4-2009Document14 pagesAccounting (IAS) Level 3/series 4-2009Hein Linn KyawNo ratings yet

- 7-Fitch AssignmentDocument16 pages7-Fitch AssignmentUpal MahmudNo ratings yet

- Accounting IAS Model Answers Series 2 2010Document17 pagesAccounting IAS Model Answers Series 2 2010Aung Zaw HtweNo ratings yet

- 7110 Principles of Accounts: MARK SCHEME For The May/June 2010 Question Paper For The Guidance of TeachersDocument7 pages7110 Principles of Accounts: MARK SCHEME For The May/June 2010 Question Paper For The Guidance of TeachersArumugam ManickamNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDocument6 pages9706 Accounting: MARK SCHEME For The May/June 2014 SeriesAhnaf AhadNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2006 Question PaperDocument7 pages9706 Accounting: MARK SCHEME For The October/November 2006 Question Paperashley chairukaNo ratings yet

- Confidential 1 AC/TEST MAY 2021/FAR270Document5 pagesConfidential 1 AC/TEST MAY 2021/FAR270Lampard AimanNo ratings yet

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2007 Question PaperDocument7 pages9706 Accounting: MARK SCHEME For The May/June 2007 Question Paperroukaiya_peerkhanNo ratings yet

- Requirement Nos. 1 To 4: PROBLEM NO. 1 - Conviction CorporationDocument8 pagesRequirement Nos. 1 To 4: PROBLEM NO. 1 - Conviction CorporationMaeNo ratings yet

- Exercise Chapter 3Document7 pagesExercise Chapter 3nguyễnthùy dươngNo ratings yet

- 9 BBDocument5 pages9 BBIlesh DinyaNo ratings yet

- Problem 7 AlkDocument8 pagesProblem 7 AlkAldi HerialdiNo ratings yet

- Accounting Level 3/series 2 2008 (Code 3012)Document16 pagesAccounting Level 3/series 2 2008 (Code 3012)Hein Linn Kyaw100% (2)

- EY Cash Flow ForecastingDocument27 pagesEY Cash Flow ForecastingAsbNo ratings yet

- Suggested SolutionsDocument7 pagesSuggested SolutionsManda simzNo ratings yet

- Date Account Titles Unadjusted Trial Balance DebitDocument4 pagesDate Account Titles Unadjusted Trial Balance DebitJasminNo ratings yet

- 2006 LCCI Level 3 (IAS) Series 2Document15 pages2006 LCCI Level 3 (IAS) Series 2rachelmakiyo100% (2)

- LixingcunDocument10 pagesLixingcunMeghna JhupseeNo ratings yet

- Financial Management Mock 2Document7 pagesFinancial Management Mock 2sadathamid03No ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2013 SeriesDocument6 pages9706 Accounting: MARK SCHEME For The October/November 2013 SeriesKelvin DenhereNo ratings yet

- 25 Question PaperDocument4 pages25 Question PaperPacific Tiger0% (1)

- 9706 w10 Ms 41Document5 pages9706 w10 Ms 41kanz_h118No ratings yet

- Financial Statement Anaysis-Cat1 - 2Document16 pagesFinancial Statement Anaysis-Cat1 - 2cyrusNo ratings yet

- Berk/Demarzo, Corporate Finance Chapter 8 Tables and ExamplesDocument4 pagesBerk/Demarzo, Corporate Finance Chapter 8 Tables and ExamplesThu Thủy ĐỗNo ratings yet

- Assignment# 3 Magic TimberDocument5 pagesAssignment# 3 Magic TimberASAD ULLAH0% (2)

- Accounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusDocument20 pagesAccounting IAS (Malaysia) Model Answers Series 2 2005 Old SyllabusAung Zaw HtweNo ratings yet

- 2013 Dse Bafs 2a MS 1Document8 pages2013 Dse Bafs 2a MS 1ryanNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2013 SeriesDocument5 pages9706 Accounting: MARK SCHEME For The October/November 2013 SeriestarunyadavfutureNo ratings yet

- Afr Q4fy20Document8 pagesAfr Q4fy20Abhilash ABNo ratings yet

- Accounting IAS Series 4 2007Document14 pagesAccounting IAS Series 4 2007Sergiu BoldurescuNo ratings yet

- 4ac1 02 Rms 20240125Document9 pages4ac1 02 Rms 20240125Nang Phyu Sin Yadanar KyawNo ratings yet

- Instructions:: Question Paper Booklet CodeDocument20 pagesInstructions:: Question Paper Booklet Codenashmiabaangi3No ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperDocument5 pages9706 Accounting: MARK SCHEME For The May/June 2008 Question PaperRoukaiya PeerkhanNo ratings yet

- 9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDocument6 pages9706 Accounting: MARK SCHEME For The May/June 2014 SeriesDanny DrinkwaterNo ratings yet

- 9706 Accounting: MARK SCHEME For The October/November 2008 Question PaperDocument5 pages9706 Accounting: MARK SCHEME For The October/November 2008 Question PapercheekybuoiNo ratings yet

- Advance Ias 7Document20 pagesAdvance Ias 7Ngân Lê Trần BảoNo ratings yet

- Chapter 3 Suggested Solutions: Input Output + - + - + ProcessDocument11 pagesChapter 3 Suggested Solutions: Input Output + - + - + Processapi-3824657No ratings yet

- 2019 May MS 4ac0 2R PDFDocument9 pages2019 May MS 4ac0 2R PDFmahdiarahman10No ratings yet

- Business Book o LevelDocument7 pagesBusiness Book o LevelaviiishiiNo ratings yet

- Solution To P 9-8Document8 pagesSolution To P 9-8Muhammad Iqbal PerwaizNo ratings yet

- Accounting Level 3/series 4 2008 (3012)Document13 pagesAccounting Level 3/series 4 2008 (3012)Hein Linn Kyaw100% (1)

- Zimbabwe School Examinations Council: Accounting 9197/3Document8 pagesZimbabwe School Examinations Council: Accounting 9197/3nyashamagutsa93No ratings yet

- Name: Ticker: Industry: Jurisdiction of Incorporation: Number of Shares of Common Stock OutstandingDocument6 pagesName: Ticker: Industry: Jurisdiction of Incorporation: Number of Shares of Common Stock OutstandingTahreem BalochNo ratings yet

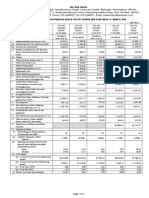

- UCrest Bhd-Q4 Financial Result Ended 31.5.2022Document8 pagesUCrest Bhd-Q4 Financial Result Ended 31.5.2022Jeff WongNo ratings yet

- Lab 3 - Stock Investment: FATA 2015Document3 pagesLab 3 - Stock Investment: FATA 2015Firda ZhafirahNo ratings yet

- FOIA No. 20-158 - Redacted PDFDocument42 pagesFOIA No. 20-158 - Redacted PDFElyssa KaufmanNo ratings yet

- Jawaban Soal UTS Akuntansi Keu - MenengahDocument4 pagesJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNo ratings yet

- BUSI 353 S18 Assignment 6 SOLUTIONDocument4 pagesBUSI 353 S18 Assignment 6 SOLUTIONTanNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Let's Practise: Maths Workbook Coursebook 7From EverandLet's Practise: Maths Workbook Coursebook 7No ratings yet

- List of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosFrom EverandList of Key Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Profitability Ratios and the Other Most Important Financial RatiosNo ratings yet

- Let's Practise: Maths Workbook Coursebook 8From EverandLet's Practise: Maths Workbook Coursebook 8No ratings yet

- Work 3000Document105 pagesWork 3000Aung Zaw HtweNo ratings yet

- J-AP-2 - Long-Term Deposits and PrepaymentsDocument3 pagesJ-AP-2 - Long-Term Deposits and PrepaymentsAung Zaw HtweNo ratings yet

- E-AP-1 - Short Term Deposits Prepayments and Other ReceivablesDocument6 pagesE-AP-1 - Short Term Deposits Prepayments and Other ReceivablesAung Zaw HtweNo ratings yet

- J-AP-1 - Long-Term Loans and AdvancesDocument13 pagesJ-AP-1 - Long-Term Loans and AdvancesAung Zaw HtweNo ratings yet

- F-Ap-3 - Inventory Held For Capital ExpenditureDocument5 pagesF-Ap-3 - Inventory Held For Capital ExpenditureAung Zaw HtweNo ratings yet

- Sample Audit ProgramDocument119 pagesSample Audit ProgramEcyojEiramMarapaoNo ratings yet

- ASE20102 - Examiner Report - November 2018Document13 pagesASE20102 - Examiner Report - November 2018Aung Zaw HtweNo ratings yet

- IFM - Lecture NotesDocument256 pagesIFM - Lecture NotesGAJALNo ratings yet

- E-AP-2 - Short-Term Loans and AdvanceDocument10 pagesE-AP-2 - Short-Term Loans and AdvanceAung Zaw HtweNo ratings yet

- N-AP-1 - Accrued MarkupDocument2 pagesN-AP-1 - Accrued MarkupAung Zaw HtweNo ratings yet

- F-AP-2 - Stores Spares and Loose ToolsDocument7 pagesF-AP-2 - Stores Spares and Loose ToolsAung Zaw HtweNo ratings yet

- E-AP-5 - Due To From Central BankDocument3 pagesE-AP-5 - Due To From Central BankAung Zaw HtweNo ratings yet

- D AP InvestmentDocument8 pagesD AP InvestmentAung Zaw HtweNo ratings yet

- C-AP - Cash and Bank BalancesDocument7 pagesC-AP - Cash and Bank BalancesAung Zaw HtweNo ratings yet

- F AP 1 Stock in TradeDocument10 pagesF AP 1 Stock in TradeAung Zaw HtweNo ratings yet

- Bank Confirmation LetterDocument4 pagesBank Confirmation Lettermarmah_hadi100% (2)

- E-AP-2 - Short-Term Loans and AdvancesDocument7 pagesE-AP-2 - Short-Term Loans and AdvancesAung Zaw HtweNo ratings yet

- D AP InvestmentDocument8 pagesD AP InvestmentAung Zaw HtweNo ratings yet

- C-AP - Cash and Bank BalancesDocument7 pagesC-AP - Cash and Bank BalancesAung Zaw HtweNo ratings yet

- E-AP-6 - Bills Discounted and PurchasedDocument3 pagesE-AP-6 - Bills Discounted and PurchasedAung Zaw HtweNo ratings yet

- E-AP-4 - Head Office and BranchDocument3 pagesE-AP-4 - Head Office and BranchAung Zaw HtweNo ratings yet

- E-AP-1 - Short Term Deposits Prepayments and Other ReceivablesDocument6 pagesE-AP-1 - Short Term Deposits Prepayments and Other ReceivablesAung Zaw HtweNo ratings yet

- E-AP-2 - Short-Term Loans and AdvanceDocument10 pagesE-AP-2 - Short-Term Loans and AdvanceAung Zaw HtweNo ratings yet

- General Balance Confirmation FormatDocument1 pageGeneral Balance Confirmation FormatZeeshan Ahmad Kahloon100% (1)

- Cash and Bank BalancesDocument4 pagesCash and Bank BalancesAung Zaw HtweNo ratings yet

- General Balance Confirmation FormatDocument1 pageGeneral Balance Confirmation FormatZeeshan Ahmad Kahloon100% (1)

- Tax Advisor Confirmation LetterDocument1 pageTax Advisor Confirmation LetterAung Zaw Htwe100% (1)

- N-AP-1 - Accrued MarkupDocument2 pagesN-AP-1 - Accrued MarkupAung Zaw HtweNo ratings yet

- Last Documents NotingDocument1 pageLast Documents NotingSonieta Deguit LabasanNo ratings yet

- Last Documents NotingDocument1 pageLast Documents NotingSonieta Deguit LabasanNo ratings yet

- Noble 8 CPlan N8 V 9Document7 pagesNoble 8 CPlan N8 V 9Kofi DanielNo ratings yet

- 3 Kinds of Taxes For Pinoy FreelancersDocument28 pages3 Kinds of Taxes For Pinoy Freelancersjedcee21No ratings yet

- Different Kinds of SkirtDocument15 pagesDifferent Kinds of SkirtKenneth MoralesNo ratings yet

- Option Floor and Caps Collars MFI FINALDocument20 pagesOption Floor and Caps Collars MFI FINALamit_harry100% (2)

- Hailey College of Commerce: Guidelines For Test Entry Test (Mphil Commerce 2019)Document4 pagesHailey College of Commerce: Guidelines For Test Entry Test (Mphil Commerce 2019)Tehreem AtharNo ratings yet

- BISIDocument3 pagesBISIDjohan HarijonoNo ratings yet

- Percentages: Multiple-Choice QuestionsDocument4 pagesPercentages: Multiple-Choice QuestionsJason Lam LamNo ratings yet

- Skema Pemarkahan Pengaturcaraan Linear SMK Agama Tun JuharDocument19 pagesSkema Pemarkahan Pengaturcaraan Linear SMK Agama Tun JuharYONGRENYIENo ratings yet

- BS 7Document5 pagesBS 7Prudhvinadh KopparapuNo ratings yet

- F3 Financial Accounting Int Revision Kit BPP PDFDocument2 pagesF3 Financial Accounting Int Revision Kit BPP PDFJeremy100% (1)

- Futureadpro Marketingplan enDocument10 pagesFutureadpro Marketingplan enapi-384421752No ratings yet

- Ac Phase Control of TriacDocument4 pagesAc Phase Control of Triacjassisc0% (1)

- Course Books Financial ManagementDocument2 pagesCourse Books Financial ManagementaluiscgNo ratings yet

- Certified Licensing Professional Examination ReferencesDocument2 pagesCertified Licensing Professional Examination ReferencesJim WolfeNo ratings yet

- Principles of Bookkeeping and Farm Accounts 1913Document188 pagesPrinciples of Bookkeeping and Farm Accounts 1913q3rNo ratings yet

- 1 191202 BS Experts See 25 Bps Rate Cut by RBI in December, FY20 GDP Forecast at 6%Document2 pages1 191202 BS Experts See 25 Bps Rate Cut by RBI in December, FY20 GDP Forecast at 6%VaibhavNo ratings yet

- Knit Sock Workshop MeasurementsDocument9 pagesKnit Sock Workshop MeasurementsJacob Miranda100% (2)

- Determination of Forward and FuturesDocument46 pagesDetermination of Forward and FuturesVaidyanathan RavichandranNo ratings yet

- Jafza Chennai BrochureDocument6 pagesJafza Chennai BrochureAman Khanna100% (1)

- Financial Accounting Past Paper 2019Document3 pagesFinancial Accounting Past Paper 2019Rana Hanzila TahirNo ratings yet

- Official ReceiptsDocument1 pageOfficial ReceiptsCharlie HansNo ratings yet

- Tatkal TicketDocument1 pageTatkal TicketSai Kiran ChandrasekharuniNo ratings yet

- RM Case 01Document3 pagesRM Case 01Milin NagarNo ratings yet

- 5-15 Resolution For Stock Issuance To Certain PersonsDocument2 pages5-15 Resolution For Stock Issuance To Certain PersonsDaniel100% (3)

- Irregular Verbs: Base Form Past Form Past Participle TranslationDocument5 pagesIrregular Verbs: Base Form Past Form Past Participle TranslationLaura TicoiuNo ratings yet

- A Dream Takes FlightDocument3 pagesA Dream Takes FlightHafiq AmsyarNo ratings yet

- Mgeh14 PS4Document3 pagesMgeh14 PS4Haley HopperNo ratings yet

- Fixed and Floating Exchange Rate.Document31 pagesFixed and Floating Exchange Rate.vikas0100% (1)

- Chapter 8 SolutionsDocument11 pagesChapter 8 Solutionsbellohales67% (3)

- Risk Over Reward: Betting Size: Kelly Criterion and Portfolio VarianceDocument4 pagesRisk Over Reward: Betting Size: Kelly Criterion and Portfolio VarianceAri David PaulNo ratings yet