You might also like

- Module 3 Investment ManagementDocument17 pagesModule 3 Investment ManagementJennica CruzadoNo ratings yet

- Lesson 1 Cash and Cash EquivalentsDocument10 pagesLesson 1 Cash and Cash EquivalentsRica Lei N. DomingoNo ratings yet

- Intermediate Accounting 1a Cash and Cash EquivalentsDocument8 pagesIntermediate Accounting 1a Cash and Cash EquivalentsGinalyn FormentosNo ratings yet

- Definition of 'Short-Term Investments': Cash and Cash Equivalents Are The Most LiquidDocument3 pagesDefinition of 'Short-Term Investments': Cash and Cash Equivalents Are The Most LiquidHazel San JuanNo ratings yet

- CashDocument26 pagesCashLj SzeNo ratings yet

- Nature of Cash AccountDocument10 pagesNature of Cash AccountLorena PernatoNo ratings yet

- Cash and Cash EquivalentsDocument5 pagesCash and Cash EquivalentsJladySilhoutte100% (3)

- Money Market Instruments in PakistanDocument3 pagesMoney Market Instruments in PakistanAsif PharmacistNo ratings yet

- Manajemen 28-3Document8 pagesManajemen 28-3Theresiana DeboraNo ratings yet

- Intermediate Accounting NOTESDocument5 pagesIntermediate Accounting NOTESIanne Kristie QuiderNo ratings yet

- Cash PDFDocument10 pagesCash PDFGabriel JonNo ratings yet

- Financial Reporting Standards Council: A Committee of TheDocument15 pagesFinancial Reporting Standards Council: A Committee of TheYtb AccntNo ratings yet

- Assessment Task 1 (IA)Document4 pagesAssessment Task 1 (IA)Jonalyn BañegaNo ratings yet

- Investment Decisions - Chapter - 1 UpdatedDocument15 pagesInvestment Decisions - Chapter - 1 UpdatedAvinash RajeshNo ratings yet

- C and CE NotesDocument4 pagesC and CE NotesFrancine PimentelNo ratings yet

- Compiled by Birhanu M (MBA-Finance) Page 1Document9 pagesCompiled by Birhanu M (MBA-Finance) Page 1Nigussie BerhanuNo ratings yet

- Module 004 Accounting For Cash: Definition, Nature and Composition of Cash and Cash Equivalents CashDocument12 pagesModule 004 Accounting For Cash: Definition, Nature and Composition of Cash and Cash Equivalents CashLee-chard EboeboNo ratings yet

- 05 Cash Cash EquivalentsDocument54 pages05 Cash Cash EquivalentsFordan Antolino83% (12)

- ReviewerDocument67 pagesReviewerKyungsoo DohNo ratings yet

- UntitledDocument6 pagesUntitledThelma DancelNo ratings yet

- Part One: Money and Capital Market: Chapter Four Financial Markets in The Financial SystemDocument22 pagesPart One: Money and Capital Market: Chapter Four Financial Markets in The Financial SystemSeid KassawNo ratings yet

- Chapter Four FinalDocument18 pagesChapter Four FinalSeid KassawNo ratings yet

- Quiz 3 MidtermDocument4 pagesQuiz 3 MidtermAlicia Dawn A. OlimbaNo ratings yet

- Quiz 3 MidtermDocument4 pagesQuiz 3 MidtermAlicia Dawn A. OlimbaNo ratings yet

- Working Capital ManagementDocument10 pagesWorking Capital Managementsincere sincereNo ratings yet

- FIN AC 1 - Module 3Document4 pagesFIN AC 1 - Module 3Ashley ManaliliNo ratings yet

- TUESDAYDocument13 pagesTUESDAYBryan Red AngaraNo ratings yet

- Cash & Cash EquivalentsDocument34 pagesCash & Cash EquivalentsStudent Core GroupNo ratings yet

- Chapter 6 - Cash Management: Learning ObjectivesDocument5 pagesChapter 6 - Cash Management: Learning Objectives132345usdfghjNo ratings yet

- Week 02 - 01 - Module 04 - Accounting For CashDocument12 pagesWeek 02 - 01 - Module 04 - Accounting For Cash지마리No ratings yet

- 05 Cash Cash EquivalentsDocument25 pages05 Cash Cash Equivalentscherylsujede4No ratings yet

- Chapter 2 Cash and Cash EquivalentsDocument12 pagesChapter 2 Cash and Cash EquivalentslorieferpaloganNo ratings yet

- (Lecture 6 & 7) - Sources of FinanceDocument21 pages(Lecture 6 & 7) - Sources of FinanceAjay Kumar TakiarNo ratings yet

- Chapter Three Financial Markets in The Financial System: 3.1 Organization and Structure of MarketsDocument7 pagesChapter Three Financial Markets in The Financial System: 3.1 Organization and Structure of MarketsSeid KassawNo ratings yet

- Working Capital ManagementDocument9 pagesWorking Capital ManagementEmmanuelNo ratings yet

- Topic 5 - Cash and Cash Equivalent - Rev (Students)Document31 pagesTopic 5 - Cash and Cash Equivalent - Rev (Students)Novian Dwi Ramadana0% (1)

- Reviewer 5Document8 pagesReviewer 5Kindred Wolfe100% (1)

- Reviewer Accounting - CrisaDocument12 pagesReviewer Accounting - Crisamiracle123No ratings yet

- 222WC2Document10 pages222WC2Cattyyy Delos ReyesNo ratings yet

- Financial Accounting and Reporting - Cash and Cash EquivalentsDocument6 pagesFinancial Accounting and Reporting - Cash and Cash EquivalentsLuisitoNo ratings yet

- Money MarketDocument4 pagesMoney MarketHaris HussainNo ratings yet

- Cashand Cash Equivalents101Document38 pagesCashand Cash Equivalents101Wynphap podiotanNo ratings yet

- Topic 2 Bank Accounts and Credit SecuritiesDocument37 pagesTopic 2 Bank Accounts and Credit SecuritiescontactitsshunNo ratings yet

- Investment and Portfolio Mngt. Learning Module 2Document6 pagesInvestment and Portfolio Mngt. Learning Module 2Aira AbigailNo ratings yet

- Money Market Securities - : Certificates of Deposit (CDS)Document4 pagesMoney Market Securities - : Certificates of Deposit (CDS)Crisha-mae JavillonarNo ratings yet

- 1.accounting Concepts and ConventionDocument6 pages1.accounting Concepts and ConventionAkhil ManojNo ratings yet

- Chapter 6 - Money MarketsDocument47 pagesChapter 6 - Money MarketsBeah Toni PacundoNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document15 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Asset-V1 - VIT BMT1005 2020 Type@asset block@Week-11-Annuity-MaterialDocument7 pagesAsset-V1 - VIT BMT1005 2020 Type@asset block@Week-11-Annuity-MaterialAYUSH GURTU 17BEC0185No ratings yet

- Cash and Marketable SecuritiesDocument4 pagesCash and Marketable SecuritiesIrish NicolasNo ratings yet

- Module 1.1Document13 pagesModule 1.1Althea mary kate MorenoNo ratings yet

- Cash and Cash EquivalentsDocument15 pagesCash and Cash EquivalentsVon Rother Celoso DiazNo ratings yet

- Working Capital Management: Answers To End-Of-Chapter QuestionsDocument27 pagesWorking Capital Management: Answers To End-Of-Chapter QuestionsMiftahul FirdausNo ratings yet

- Ae 18 Financial MarketsDocument4 pagesAe 18 Financial Marketsnglc srzNo ratings yet

- Working Capital CashDocument6 pagesWorking Capital CashNiña Rhocel YangcoNo ratings yet

- Chapter 3Document8 pagesChapter 3yosef mechalNo ratings yet

- Cash - NotesDocument2 pagesCash - NotesAdri SampangNo ratings yet

- FM11 CH 22 Instructors ManualDocument6 pagesFM11 CH 22 Instructors ManualFahad AliNo ratings yet

- Topic 5 - Cash and Cash Equivalent - Rev (Students)Document31 pagesTopic 5 - Cash and Cash Equivalent - Rev (Students)RomziNo ratings yet

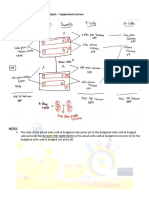

- 10 Gross Profit Variance Analysis - Supplement LectureDocument3 pages10 Gross Profit Variance Analysis - Supplement LectureXander MerzaNo ratings yet

- Winning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessDocument23 pagesWinning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessXander MerzaNo ratings yet

- Environmental GovernanceDocument68 pagesEnvironmental GovernanceXander MerzaNo ratings yet

- Operating Lease - Lessee: Problem 1Document2 pagesOperating Lease - Lessee: Problem 1Xander MerzaNo ratings yet

- BASTRCSX - Module 1Document67 pagesBASTRCSX - Module 1Xander MerzaNo ratings yet

- CFAS Soln Man 2020 Edition 3Document3 pagesCFAS Soln Man 2020 Edition 3Xander MerzaNo ratings yet

- Debt Investments - Answers - Ac&fvociDocument9 pagesDebt Investments - Answers - Ac&fvociXander MerzaNo ratings yet

- Collateral For Loan Applications.: Receivable FinancingDocument3 pagesCollateral For Loan Applications.: Receivable FinancingXander MerzaNo ratings yet

- Research Problem & Its Objectives: Elements of Chapter 1Document22 pagesResearch Problem & Its Objectives: Elements of Chapter 1Xander MerzaNo ratings yet

- Review of Related LiteratureDocument13 pagesReview of Related LiteratureXander MerzaNo ratings yet

- Corporation 1Document110 pagesCorporation 1Xander MerzaNo ratings yet

- Human RightsDocument37 pagesHuman RightsXander MerzaNo ratings yet