You might also like

- Review Capital BudgetingDocument22 pagesReview Capital BudgetingJamesno LumbNo ratings yet

- Definitions For Cape Economics Unit 1Document3 pagesDefinitions For Cape Economics Unit 1Rafena Mustapha100% (1)

- Cash Flow Estimation and Capital BudgetingDocument31 pagesCash Flow Estimation and Capital BudgetingjoanabudNo ratings yet

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Module 3 Income Tax On IndividualsDocument77 pagesModule 3 Income Tax On IndividualsAriza CastroverdeNo ratings yet

- ECH158A Lecture 4-HUMG 2019 PDFDocument60 pagesECH158A Lecture 4-HUMG 2019 PDFLe Anh QuânNo ratings yet

- Cost Estimation: (CHAPTER-3)Document43 pagesCost Estimation: (CHAPTER-3)fentaw melkieNo ratings yet

- Chapter 17. HouseholdsDocument53 pagesChapter 17. HouseholdsIbrahim Nafiu100% (1)

- Solman de Leon 2016 PDFDocument95 pagesSolman de Leon 2016 PDFZo Thelf0% (1)

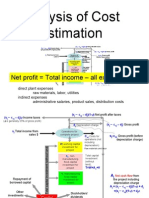

- Analysis of Cost EstimationDocument58 pagesAnalysis of Cost Estimationccsreddy100% (3)

- Sesi 12 - Analisa Potensi Bisnis Dan Praktek Urban Farming IIDocument10 pagesSesi 12 - Analisa Potensi Bisnis Dan Praktek Urban Farming IIlawakfessNo ratings yet

- Capítulo 6 Cálculo Del Costo de Fabricación PDFDocument25 pagesCapítulo 6 Cálculo Del Costo de Fabricación PDFFrancisco QuirogaNo ratings yet

- (Chapter 6) Gael D Ulrich - A Guide To Chemical Engineering Process Design and Economics (1984, Wiley)Document19 pages(Chapter 6) Gael D Ulrich - A Guide To Chemical Engineering Process Design and Economics (1984, Wiley)Rosa BrilianaNo ratings yet

- Capital Budgeting: MF 807 Corporate Finance Professor Thomas ChemmanurDocument19 pagesCapital Budgeting: MF 807 Corporate Finance Professor Thomas ChemmanurAntora HoqueNo ratings yet

- NPV and Capital Budgeting: A Short Note On Estimation of Project Cash FlowsDocument7 pagesNPV and Capital Budgeting: A Short Note On Estimation of Project Cash FlowsRobel AbebawNo ratings yet

- Measuring Effective Tax Rates For Oil and Gas in Canada: SPP Technical PapersDocument20 pagesMeasuring Effective Tax Rates For Oil and Gas in Canada: SPP Technical PapersSchoolofPublicPolicyNo ratings yet

- LecturePA EconIndicatorsDocument32 pagesLecturePA EconIndicatorsRahmat Ramadhan RahmatNo ratings yet

- Project Cash Flows and Cash ReturnDocument11 pagesProject Cash Flows and Cash ReturnBradley NelsonNo ratings yet

- LEK RapportDocument10 pagesLEK RapportAlternatievenVliegveldTwenteNo ratings yet

- International Financial Management PgapteDocument20 pagesInternational Financial Management Pgapterameshmba100% (1)

- Disclosure DR.2Document2 pagesDisclosure DR.2Zach EdwardsNo ratings yet

- Capital Budgeting: Should We Build This Plant?Document51 pagesCapital Budgeting: Should We Build This Plant?Amit VijayvargiyaNo ratings yet

- 6.1 Contract Cash FlowDocument26 pages6.1 Contract Cash FlowShroukAdelMohamedGaribNo ratings yet

- Ee Cash Flows and Capital BudgetingDocument33 pagesEe Cash Flows and Capital Budgetingdwi suhartantoNo ratings yet

- Chapter 2 108 131Document25 pagesChapter 2 108 131Arielle CabritoNo ratings yet

- C Effects QF Pernianent and Temporary Tax Policies: A Q Model of InvestmentDocument21 pagesC Effects QF Pernianent and Temporary Tax Policies: A Q Model of Investmentbiblioteca economicaNo ratings yet

- International Capital Budgeting and Cost of CapitalDocument50 pagesInternational Capital Budgeting and Cost of CapitalGaurav Kumar100% (2)

- Capital Budgeting PrimerDocument19 pagesCapital Budgeting PrimerZahid MahmoodNo ratings yet

- PDF 5 Income TaxDocument1 pagePDF 5 Income Taxmanishchd81No ratings yet

- Project Analysis Chapter FiveDocument20 pagesProject Analysis Chapter FivezewdieNo ratings yet

- WGC Guidance On Non-Gaap MetricsDocument2 pagesWGC Guidance On Non-Gaap MetricsMiguel SanchezNo ratings yet

- Chap 12 Problem SolutionsDocument36 pagesChap 12 Problem SolutionsSilvi SuryaNo ratings yet

- Cost Estimation BasisDocument58 pagesCost Estimation BasisFredy ZumbanaNo ratings yet

- Chapter Eight Advanced Investment AppraisalDocument18 pagesChapter Eight Advanced Investment Appraisalkuttan1000100% (1)

- Capital Theory and Investment Behavior : Dale W. JorgensonDocument13 pagesCapital Theory and Investment Behavior : Dale W. JorgensonstevenjstNo ratings yet

- (IE) Chapter 4 - Investment EfficiencyDocument88 pages(IE) Chapter 4 - Investment EfficiencyJane VickyNo ratings yet

- CMET401 Economic Evaluation of ProjectsDocument50 pagesCMET401 Economic Evaluation of ProjectsAHMED ALI S ALAHMADINo ratings yet

- Topic02 ValuationDocument62 pagesTopic02 ValuationGaukhar RyskulovaNo ratings yet

- Vis 9Document4 pagesVis 9mg_catanaNo ratings yet

- SABV Topic 1 QuestionsDocument3 pagesSABV Topic 1 QuestionsNgoc Hoang Ngan NgoNo ratings yet

- Working Papers: Bureau of Economics Federal Trade Commission Washington, DC 20580Document24 pagesWorking Papers: Bureau of Economics Federal Trade Commission Washington, DC 20580hadiNo ratings yet

- Basic Accounting TermsDocument22 pagesBasic Accounting TermsAastha SharmaNo ratings yet

- Fin311 Paper A All AnswersDocument17 pagesFin311 Paper A All Answerssuleman yousafzaiNo ratings yet

- 'Epiffi5hrri (T - T 4## U ,: "TR - O,,".-O.uDocument3 pages'Epiffi5hrri (T - T 4## U ,: "TR - O,,".-O.uZach EdwardsNo ratings yet

- PFM15e IM CH11Document28 pagesPFM15e IM CH11Daniel HakimNo ratings yet

- 6.2.economic Evaluation. Capital and COMDocument8 pages6.2.economic Evaluation. Capital and COMEstefanía Duarte SilvaNo ratings yet

- Exercises 270919Document3 pagesExercises 270919Kim AnhNo ratings yet

- UNIT - 2 - Final AccountsDocument57 pagesUNIT - 2 - Final AccountsRaju NagarNo ratings yet

- 2.edited FM Capital BudgetingDocument72 pages2.edited FM Capital BudgetingbelovedbijithNo ratings yet

- CH 4.7-Project Financial Analysis - CH 5Document41 pagesCH 4.7-Project Financial Analysis - CH 5yemsrachhailu8No ratings yet

- Chapter 12: Cash Flow Estimation and Risks AnalysisDocument45 pagesChapter 12: Cash Flow Estimation and Risks AnalysisElizabeth Espinosa ManilagNo ratings yet

- Chapter 12: Cash Flow Estimation and Risks AnalysisDocument45 pagesChapter 12: Cash Flow Estimation and Risks AnalysisElizabeth Espinosa ManilagNo ratings yet

- Review Real EstateDocument10 pagesReview Real EstateJune AlapaNo ratings yet

- Chapter FourDocument40 pagesChapter FourBikila DessalegnNo ratings yet

- 2-Discounted Cash Flow ApplicationsDocument33 pages2-Discounted Cash Flow ApplicationsBeatrice Sona mariaNo ratings yet

- Process Product Manufacturing Aace International: ContingenciesDocument1 pageProcess Product Manufacturing Aace International: ContingenciesSucher EolasNo ratings yet

- JEHT Foundation - 2001 Tax ReturnDocument17 pagesJEHT Foundation - 2001 Tax ReturnMain JusticeNo ratings yet

- Business Valuation (FCFF)Document5 pagesBusiness Valuation (FCFF)Akshat JainNo ratings yet

- Lec - 3Document7 pagesLec - 3Mostafa KaghaNo ratings yet

- Chapter 12 - Tax Depreciation, Amortisation - Pre-Commencement Expenditure PDFDocument24 pagesChapter 12 - Tax Depreciation, Amortisation - Pre-Commencement Expenditure PDFZain-ul- FaridNo ratings yet

- Chap 17Document22 pagesChap 17rajvindermomiNo ratings yet

- Reducing Business Jet Carbon Footprint: Using the Power of the Aircraft Electric Taxi SystemFrom EverandReducing Business Jet Carbon Footprint: Using the Power of the Aircraft Electric Taxi SystemNo ratings yet

- AyeshaDocument2 pagesAyeshaHa M ZaNo ratings yet

- Adobe Scan 22 Dec 2020Document1 pageAdobe Scan 22 Dec 2020Ha M ZaNo ratings yet

- Chemical Engg Plant Design LabDocument2 pagesChemical Engg Plant Design LabHa M ZaNo ratings yet

- Microsoft Power Point Lab ManualDocument8 pagesMicrosoft Power Point Lab ManualHa M ZaNo ratings yet

- Raw Materia Weighing Ball MillingDocument1 pageRaw Materia Weighing Ball MillingHa M ZaNo ratings yet

- CFTDocument25 pagesCFTHa M ZaNo ratings yet

- Exercise:3: English Submitted To: Samer AshiqDocument9 pagesExercise:3: English Submitted To: Samer AshiqHa M ZaNo ratings yet

- An Overview of Rice Husk Applications and Modification Techniques in Wastewater TreatmentDocument28 pagesAn Overview of Rice Husk Applications and Modification Techniques in Wastewater TreatmentHa M ZaNo ratings yet

- Assignment 3333Document8 pagesAssignment 3333Ha M ZaNo ratings yet

- Microbiology Submitted To: DR M.Hidayat Rasool: Semester 1Document2 pagesMicrobiology Submitted To: DR M.Hidayat Rasool: Semester 1Ha M ZaNo ratings yet

- Responses. Cambridge University PressDocument2 pagesResponses. Cambridge University PressHa M ZaNo ratings yet

- SaponificationDocument5 pagesSaponificationHa M ZaNo ratings yet

- University of Wah Wah Engineering College Assignment # 02Document1 pageUniversity of Wah Wah Engineering College Assignment # 02Ha M ZaNo ratings yet

- Literature CitedDocument2 pagesLiterature CitedHa M ZaNo ratings yet

- Sample Letter ZainDocument1 pageSample Letter ZainHa M ZaNo ratings yet

- Effective Preventive Maintenance Scheduling: A Case StudyDocument9 pagesEffective Preventive Maintenance Scheduling: A Case StudyHa M ZaNo ratings yet

- "Quantitative Research Approach Was Used by Conducting A Questionnaire Survey That Was Based UponDocument2 pages"Quantitative Research Approach Was Used by Conducting A Questionnaire Survey That Was Based UponHa M ZaNo ratings yet

- University of Wah Wah Engineering College Assignment # 01Document2 pagesUniversity of Wah Wah Engineering College Assignment # 01Ha M ZaNo ratings yet

- Stochastic Frontier Analysis and DEADocument3 pagesStochastic Frontier Analysis and DEAHa M ZaNo ratings yet

- Final-Yr-Thesis-Pdf Uet PeshawarDocument137 pagesFinal-Yr-Thesis-Pdf Uet PeshawarHa M ZaNo ratings yet

- The Measurement of Productive Efficiency and Productivity ChangeDocument4 pagesThe Measurement of Productive Efficiency and Productivity ChangeHa M ZaNo ratings yet

- Hydrogen Rich Syngas Production From Oxy-Steam Gasification of A Lignite Coal - A Design and Optimization Study Robert Mota, Gautham Krishnamoorthy, Oyebola Dada, Steven A BensonDocument31 pagesHydrogen Rich Syngas Production From Oxy-Steam Gasification of A Lignite Coal - A Design and Optimization Study Robert Mota, Gautham Krishnamoorthy, Oyebola Dada, Steven A BensonHa M ZaNo ratings yet

- REGRESSIONDocument2 pagesREGRESSIONHa M ZaNo ratings yet

- 1 s2.0 S2351978920301281 MainDocument10 pages1 s2.0 S2351978920301281 MainHa M ZaNo ratings yet

- Final SemifinalDocument86 pagesFinal SemifinalHa M ZaNo ratings yet

- Lesson Learned and Success Factors On Dried Banana Product Community Enterprise Management in Ratchaburi Province, ThailandDocument12 pagesLesson Learned and Success Factors On Dried Banana Product Community Enterprise Management in Ratchaburi Province, ThailandIjahss JournalNo ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment YearVivek SinghNo ratings yet

- Payroll WorksheetDocument2 pagesPayroll WorksheetGena Duresa100% (1)

- Itr Simpal Kumari 23 24Document1 pageItr Simpal Kumari 23 24prateek gangwaniNo ratings yet

- AEON - AR2021 (Part 4)Document66 pagesAEON - AR2021 (Part 4)SITI NAJIBAH BINTI MOHD NORNo ratings yet

- Sonali Bank Annual Report 2021 PDFDocument415 pagesSonali Bank Annual Report 2021 PDFPrantoNo ratings yet

- Entrep Lec MidtermsDocument8 pagesEntrep Lec MidtermsAdriane LustreNo ratings yet

- SSTNotes 6Document16 pagesSSTNotes 6UganNo ratings yet

- Lorenz Curve-Presentation1Document8 pagesLorenz Curve-Presentation1Leo SuingNo ratings yet

- Income From Other SourcesDocument10 pagesIncome From Other SourcesHarsha VardhanaNo ratings yet

- 104-B, STREET 4, EDEN CITY, LAHORE, Lahore Cantonement Muhammad Salman EjazDocument3 pages104-B, STREET 4, EDEN CITY, LAHORE, Lahore Cantonement Muhammad Salman EjazFaizi93No ratings yet

- Entrepreneurship12q2_Mod8_Computation-of-Gross-Profit_v3Document18 pagesEntrepreneurship12q2_Mod8_Computation-of-Gross-Profit_v3pauljulius.regioNo ratings yet

- Accounting For Income Taxes ExercisessDocument5 pagesAccounting For Income Taxes ExercisessdorothyannvillamoraaNo ratings yet

- SH Eq 2 - ProblemsDocument9 pagesSH Eq 2 - ProblemsLordcille AguilarNo ratings yet

- I. Introductory Page Name and Address of Business Bottle Brothers Glass Bottle Distributor, #69 Sipat, Plaridel, BulacanDocument51 pagesI. Introductory Page Name and Address of Business Bottle Brothers Glass Bottle Distributor, #69 Sipat, Plaridel, Bulacanmarichu apiladoNo ratings yet

- Aicpa Aag Con Exposure May 10 2021Document34 pagesAicpa Aag Con Exposure May 10 2021Jamilene PandanNo ratings yet

- Correction of Errors Theory ExerciseDocument2 pagesCorrection of Errors Theory ExerciseChristine Mae Fernandez MataNo ratings yet

- Module 1 - Review TestDocument2 pagesModule 1 - Review TestTBA PacificNo ratings yet

- Adamson University College of Business Administration Financial Accounting III Midterm Examination OriginalDocument5 pagesAdamson University College of Business Administration Financial Accounting III Midterm Examination OriginalMarie Tes LocsinNo ratings yet

- Acctg 115 - CH 5 SolutionsDocument11 pagesAcctg 115 - CH 5 SolutionsSharadPanchal100% (1)

- Accounts Statement IiDocument51 pagesAccounts Statement Iiapi-19728905No ratings yet

- Millenials Marapr Univ Basic IncomeDocument322 pagesMillenials Marapr Univ Basic IncomeJillian LilasNo ratings yet

- Kunci JWB pkt2. 3 PDsuburDocument45 pagesKunci JWB pkt2. 3 PDsuburSyifa FaNo ratings yet

- Economics Unit 4 - Past Paper Section A 20 & 30 Mark QuestionsDocument7 pagesEconomics Unit 4 - Past Paper Section A 20 & 30 Mark QuestionsNigov ChigovNo ratings yet

- 1 B - Answer - Thories - Asset - Liability - Equity - Mas - MidtermsDocument23 pages1 B - Answer - Thories - Asset - Liability - Equity - Mas - MidtermsAlthea mary kate MorenoNo ratings yet