You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- LeverageDocument64 pagesLeverageUsha Padyana100% (1)

- The Wealth Matrix - Shifting From Active To Passive Income 5 Day WeekendDocument7 pagesThe Wealth Matrix - Shifting From Active To Passive Income 5 Day Weekendkegezifapa0% (1)

- CPWA CODE 101-150 (Guide Part 4) PDFDocument15 pagesCPWA CODE 101-150 (Guide Part 4) PDFshekarj80% (5)

- 9211stmt 16022017 1499569616627 PDFDocument5 pages9211stmt 16022017 1499569616627 PDFInfohoggNo ratings yet

- Kapital LamiyaDocument1 pageKapital LamiyaSadiq PenahovNo ratings yet

- Financial Crises: Lessons From The Past, Preparation For The FutureDocument298 pagesFinancial Crises: Lessons From The Past, Preparation For The FutureJayeshNo ratings yet

- J-Curve Disparity Between The Goods Sector and The Services Sector: Evidence From AustraliaDocument6 pagesJ-Curve Disparity Between The Goods Sector and The Services Sector: Evidence From AustraliaKhaled AhmadNo ratings yet

- Bangladesh DevaluationDocument24 pagesBangladesh DevaluationKhaled AhmadNo ratings yet

- Thailand Currency DevaluationDocument41 pagesThailand Currency DevaluationKhaled AhmadNo ratings yet

- Turkey DevaluationDocument9 pagesTurkey DevaluationKhaled AhmadNo ratings yet

- Devaluation ChinaDocument5 pagesDevaluation ChinaKhaled AhmadNo ratings yet

- Chapter 6 Personality, Lifestyles, and Values: Consumer Behaviour, 7e (Solomon)Document34 pagesChapter 6 Personality, Lifestyles, and Values: Consumer Behaviour, 7e (Solomon)Khaled AhmadNo ratings yet

- Currency DevaluationDocument24 pagesCurrency DevaluationKhaled AhmadNo ratings yet

- Aul Dekwaneh Khaled Ahmad Senior Presentatio - SpringDocument19 pagesAul Dekwaneh Khaled Ahmad Senior Presentatio - SpringKhaled AhmadNo ratings yet

- Currency Devaluation Working PaperDocument57 pagesCurrency Devaluation Working PaperKhaled Ahmad100% (1)

- Aul Dekwaneh Khaled Ahmad Senior Presentatio - SpringDocument19 pagesAul Dekwaneh Khaled Ahmad Senior Presentatio - SpringKhaled AhmadNo ratings yet

- Macro Mid 1 SolutionDocument4 pagesMacro Mid 1 SolutionMd. Sakib HossainNo ratings yet

- MFIN6622 Teaching Notes Session 2 (Delivered)Document66 pagesMFIN6622 Teaching Notes Session 2 (Delivered)Riha MachireddyNo ratings yet

- Statement 2020MTH06 551509617Document2 pagesStatement 2020MTH06 551509617Vijay KumarNo ratings yet

- Terms and Conditions For Emi On Cashback Offer On Flipkart Axis Bank Credit Card NewDocument3 pagesTerms and Conditions For Emi On Cashback Offer On Flipkart Axis Bank Credit Card NewGoffardNo ratings yet

- Business Studies: Bharat Heavy Electricals LimitedDocument43 pagesBusiness Studies: Bharat Heavy Electricals LimitedVenkatramana K0% (2)

- IAS 36 MCQ AnswersDocument3 pagesIAS 36 MCQ AnswersUmar bin AsfarNo ratings yet

- Financial Statement Analysis 2019Document28 pagesFinancial Statement Analysis 2019ALPASLAN TOKERNo ratings yet

- Stock ValuationDocument7 pagesStock ValuationZinebCherkaouiNo ratings yet

- Flash Memory 2Document9 pagesFlash Memory 2Sachin GuptaNo ratings yet

- 1068026189-Special NoticeDocument4 pages1068026189-Special NoticeBVS NAGABABUNo ratings yet

- Comparative Analysis of Merchant Banking Services in Public Sector Bank & Private Sector BankDocument37 pagesComparative Analysis of Merchant Banking Services in Public Sector Bank & Private Sector BankAmarbant Singh DNo ratings yet

- USA v. Theresa Tetley Sentencing MemoDocument17 pagesUSA v. Theresa Tetley Sentencing MemoCrowdfundInsiderNo ratings yet

- Long Term Capital Management The Dangers of LeverageDocument25 pagesLong Term Capital Management The Dangers of LeveragepidieNo ratings yet

- Hyperinflation ZimbabweDocument3 pagesHyperinflation ZimbabweAayanRoyNo ratings yet

- 3.EF232.FIMIL II Question CMA September 2022 Exam.Document8 pages3.EF232.FIMIL II Question CMA September 2022 Exam.nobiNo ratings yet

- CaseofnorwayDocument12 pagesCaseofnorwaykhchengNo ratings yet

- TLV 20221111164418 2022-Q3-ReportDocument84 pagesTLV 20221111164418 2022-Q3-Reportafrodita99977No ratings yet

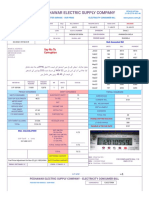

- Pesco Online BillDocument1 pagePesco Online BillMubashir JanNo ratings yet

- Ejercito vs. SandiganbayanDocument4 pagesEjercito vs. SandiganbayanDum DumNo ratings yet

- Functions of Credit Administration DepartmentDocument4 pagesFunctions of Credit Administration Departmentsamaritasaha100% (1)

- Concepts of The Accounting Basis of Government Accounting: September 2018Document7 pagesConcepts of The Accounting Basis of Government Accounting: September 2018Jon LangajedNo ratings yet

- Differences Between Cash Dividends and Stock DividendsDocument4 pagesDifferences Between Cash Dividends and Stock DividendsUme Aiman Binte NasarNo ratings yet

- Financial ManagementDocument6 pagesFinancial ManagementDaniel HunksNo ratings yet

- Financial Metrics ExampleDocument2 pagesFinancial Metrics ExampleSourav shabuNo ratings yet