You might also like

- International Commercial ClaimDocument14 pagesInternational Commercial ClaimSuzette J. DelaRocha100% (5)

- Startup SecretsDocument24 pagesStartup SecretsJohn BetancourtNo ratings yet

- 11 Business Mistakes To AvoidDocument14 pages11 Business Mistakes To Avoidmyotherone100% (1)

- Triangular Arbitrage: Actual Cross Rate and What The Cross Rate Ought To BeDocument8 pagesTriangular Arbitrage: Actual Cross Rate and What The Cross Rate Ought To BeIndeevar SarkarNo ratings yet

- Mca - 204 - FM & CFDocument28 pagesMca - 204 - FM & CFjaitripathi26No ratings yet

- Lesson 6 - Why An Entrepreneurial Mindset Is Essential For BusinessDocument8 pagesLesson 6 - Why An Entrepreneurial Mindset Is Essential For BusinessMarc Loui RiveroNo ratings yet

- Commercial Mortgage Broker Leads ListDocument102 pagesCommercial Mortgage Broker Leads ListMalik UzairNo ratings yet

- MIT Student ResumesDocument26 pagesMIT Student ResumesIvan Vargas100% (1)

- Venture Capital Firms, Finance Companies, and Financial Conglomerates ExplainedDocument8 pagesVenture Capital Firms, Finance Companies, and Financial Conglomerates ExplainedShuvro Rahman75% (12)

- Arbitrage and Law of One PriceDocument5 pagesArbitrage and Law of One Pricearmando.chappell1005No ratings yet

- Cal PERSDocument17 pagesCal PERSFortuneNo ratings yet

- Guy Kawasaki - How To Create An Enchanting Pitch #OfficeandGuyKDocument7 pagesGuy Kawasaki - How To Create An Enchanting Pitch #OfficeandGuyKTrss IkeniNo ratings yet

- 4 Proven Strategies for Successful Solar Cold Calling ScriptsDocument9 pages4 Proven Strategies for Successful Solar Cold Calling ScriptsKAUSHIK SOLANKINo ratings yet

- Team Three Hour TCPDocument24 pagesTeam Three Hour TCPapi-30304208No ratings yet

- Fabozzi CH 32 CDS HW AnswersDocument19 pagesFabozzi CH 32 CDS HW AnswersTrish Jumbo100% (1)

- Mental WealthDocument128 pagesMental WealthCollinsNo ratings yet

- Economic Order QuantityDocument7 pagesEconomic Order QuantityShuvro RahmanNo ratings yet

- Triangular ArbitrageDocument5 pagesTriangular ArbitrageSajid HussainNo ratings yet

- IFM Numericals Solutions Christ 2023Document43 pagesIFM Numericals Solutions Christ 2023Dhruvi Agarwal100% (1)

- Sample Sales PitchDocument2 pagesSample Sales PitchHenry NnorommNo ratings yet

- Cash Flow Forecast and StrategiesDocument34 pagesCash Flow Forecast and StrategiesShuvro RahmanNo ratings yet

- The Foreign Exchange MarketDocument29 pagesThe Foreign Exchange MarketSam Sep A Sixtyone100% (1)

- Someka Templates Info PDFDocument1 pageSomeka Templates Info PDFnkemoviaNo ratings yet

- Onboarding Questionaire Mash BonigalaDocument8 pagesOnboarding Questionaire Mash BonigalaMihaiIliescuNo ratings yet

- How to Build a Successful Mobile App BusinessDocument21 pagesHow to Build a Successful Mobile App BusinessrajuNo ratings yet

- FFC Dental Clinic Business Website ProposalDocument8 pagesFFC Dental Clinic Business Website ProposalKimmy Manzano0% (1)

- The WSI Franchise Business Opportunity in BahrainDocument21 pagesThe WSI Franchise Business Opportunity in BahrainWSIEstisharatechNo ratings yet

- Yoga Niche Secrets PDFDocument28 pagesYoga Niche Secrets PDFGerry LiaetzsNo ratings yet

- Automatic Response Words PDFDocument27 pagesAutomatic Response Words PDFDuong Thai BinhNo ratings yet

- Customer Analysis: 12/03/09 Dr. Kartik Dave 1Document106 pagesCustomer Analysis: 12/03/09 Dr. Kartik Dave 1Ritesh PatnaikNo ratings yet

- 100 Popular Web ToolsDocument24 pages100 Popular Web ToolstuputasNo ratings yet

- Linkedin - Docs CompilationDocument147 pagesLinkedin - Docs CompilationKiran NNo ratings yet

- Week 8 Salary Negotiation Skills TestDocument3 pagesWeek 8 Salary Negotiation Skills TestSergeiBugrovNo ratings yet

- MMSLists Successful Email Marketing MethodsDocument15 pagesMMSLists Successful Email Marketing MethodsIrinel Busca0% (1)

- ATHAL Public Relations & Marketing - PackagesDocument7 pagesATHAL Public Relations & Marketing - PackagesATHAL Public Relations & Marketing100% (1)

- Arbitrage opportunities in currency exchange ratesDocument10 pagesArbitrage opportunities in currency exchange ratesZubair ChowdhuryNo ratings yet

- Session 14 - 16 Triangluar AbritrageDocument29 pagesSession 14 - 16 Triangluar Abritragebrownpie2019No ratings yet

- 3 Foreign Exchange Markets - IIDocument5 pages3 Foreign Exchange Markets - IINaomi LyngdohNo ratings yet

- Arbitrage TheoryDocument13 pagesArbitrage TheoryRimpy SondhNo ratings yet

- Answer: Q - 1 (RTP N - S 2020, N S)Document15 pagesAnswer: Q - 1 (RTP N - S 2020, N S)sandesh SandeshNo ratings yet

- Riangular Arbitrage ExampleDocument6 pagesRiangular Arbitrage ExampleAmiko GogitidzeNo ratings yet

- Forex Transaction Types Spot Forward RatesDocument9 pagesForex Transaction Types Spot Forward Ratesmeghaparekh11No ratings yet

- International FinanceDocument44 pagesInternational FinanceSAMSONI lucasNo ratings yet

- Multinational Financial Management 10th Edition Shapiro Solutions ManualDocument15 pagesMultinational Financial Management 10th Edition Shapiro Solutions Manualcoactiongaleaiyan100% (22)

- Currency Derivatives ArbitrageDocument27 pagesCurrency Derivatives ArbitrageMinh NgọcNo ratings yet

- Answers To The Chapter ExercisesDocument14 pagesAnswers To The Chapter ExercisesSamina MahmoodNo ratings yet

- Forex Market Structure and OperationsDocument25 pagesForex Market Structure and OperationsmbondoNo ratings yet

- International Arbitrage and Interest Rate Parity: From International Finance by Jeff MaduraDocument49 pagesInternational Arbitrage and Interest Rate Parity: From International Finance by Jeff Maduraabdullah.zhayatNo ratings yet

- Illustrations For Practice Q&ADocument5 pagesIllustrations For Practice Q&ADhruvi AgarwalNo ratings yet

- USM1 FIN 614 Week02 WorkProblemsWorksheetDocument13 pagesUSM1 FIN 614 Week02 WorkProblemsWorksheetwaszenvNo ratings yet

- L2 R11 CERD Q-Bank Set 2 With AnswerDocument16 pagesL2 R11 CERD Q-Bank Set 2 With AnswerAhsan RasheedNo ratings yet

- Answers To The Chapter ExercisesDocument14 pagesAnswers To The Chapter ExercisesMohamed LibanNo ratings yet

- Sample Questions and SolutionsDocument5 pagesSample Questions and Solutionsn.iremodaciNo ratings yet

- Practice Question of International ArbitrageDocument5 pagesPractice Question of International ArbitrageHania DollNo ratings yet

- If NumericalsDocument13 pagesIf NumericalsArindam Chatterjee0% (1)

- Lots, Leverage and Margin - Forex4noobsDocument5 pagesLots, Leverage and Margin - Forex4noobsTesa MuhammadNo ratings yet

- New No 20 Cointech2u Tutarial - Plan Have SoundDocument35 pagesNew No 20 Cointech2u Tutarial - Plan Have Soundwiwat dussadinNo ratings yet

- Solutions MergedDocument32 pagesSolutions MergedjuanpablooriolNo ratings yet

- Chapter 1 - Foreign Currecies Exchange MarketDocument47 pagesChapter 1 - Foreign Currecies Exchange MarketThư Trần Thị AnhNo ratings yet

- (123doc) - Bai-Tap-On-Tap-AnswerDocument4 pages(123doc) - Bai-Tap-On-Tap-AnswerTrần Thị Mai AnhNo ratings yet

- Suggested Solutions Chapter 5Document5 pagesSuggested Solutions Chapter 5hayat0150% (2)

- How to profit from triangular arbitrage and covered interest rate arbitrageDocument7 pagesHow to profit from triangular arbitrage and covered interest rate arbitrageHạng VũNo ratings yet

- Illustrations For PracticeDocument3 pagesIllustrations For PracticeDhruvi AgarwalNo ratings yet

- UntitledDocument268 pagesUntitledkalyanNo ratings yet

- Foreign Exchange MarketDocument29 pagesForeign Exchange MarketRavi SistaNo ratings yet

- Multinational Finance-Tutorial 7 AsnwerDocument24 pagesMultinational Finance-Tutorial 7 Asnwerchun88100% (2)

- Colposcopy Done Last 5 YearsDocument1 pageColposcopy Done Last 5 YearsShuvro RahmanNo ratings yet

- Chapter - 5 Capital BudgetingDocument9 pagesChapter - 5 Capital BudgetingShuvro RahmanNo ratings yet

- Bangladesh sees record FDI in FY19 led by Japan Tobacco acquisitionDocument6 pagesBangladesh sees record FDI in FY19 led by Japan Tobacco acquisitionShuvro RahmanNo ratings yet

- Balance of Payments: Chapter Learning ObjectivesDocument74 pagesBalance of Payments: Chapter Learning ObjectivesShuvro RahmanNo ratings yet

- What Is Break Even Analysis?: Cost Accounting Total Revenue Fixed and Variable CostsDocument9 pagesWhat Is Break Even Analysis?: Cost Accounting Total Revenue Fixed and Variable CostsShuvro RahmanNo ratings yet

- Rural & Urban Econ-Ch 1Document23 pagesRural & Urban Econ-Ch 1Shuvro RahmanNo ratings yet

- MotivationDocument38 pagesMotivationShuvro RahmanNo ratings yet

- Bank Fund Case1Document2 pagesBank Fund Case1Shuvro RahmanNo ratings yet

- Insurance in Bangladesh: A Growing IndustryDocument17 pagesInsurance in Bangladesh: A Growing IndustryShuvro RahmanNo ratings yet

- Money, Monetary Policy and Bangladesh BankDocument11 pagesMoney, Monetary Policy and Bangladesh BankShuvro RahmanNo ratings yet

- Women EntrepreneurshipDocument33 pagesWomen EntrepreneurshipAseem1100% (8)

- OB Course TopicsDocument3 pagesOB Course TopicsShuvro RahmanNo ratings yet

- Corporate EntrepreneurshipDocument19 pagesCorporate EntrepreneurshipShuvro RahmanNo ratings yet

- Microcredit and EntrepreneurshipDocument2 pagesMicrocredit and EntrepreneurshipShuvro RahmanNo ratings yet

- Premiums For Insurance MathDocument6 pagesPremiums For Insurance MathShuvro Rahman100% (1)

- Financial CorruptionDocument22 pagesFinancial CorruptionShuvro RahmanNo ratings yet

- Cash Flow ValuationDocument2 pagesCash Flow ValuationShuvro RahmanNo ratings yet

- Financial Distress of CompaniesDocument3 pagesFinancial Distress of CompaniesShuvro RahmanNo ratings yet

- LeverageDocument9 pagesLeverageShuvro RahmanNo ratings yet

- Introduction to Understanding RiskDocument33 pagesIntroduction to Understanding RiskShuvro RahmanNo ratings yet

- Technical Analysis ChapterDocument24 pagesTechnical Analysis ChapterShuvro RahmanNo ratings yet

- Understanding Accounting and Financial ManagementDocument5 pagesUnderstanding Accounting and Financial ManagementShuvro RahmanNo ratings yet

- Cash Flow ValuationDocument2 pagesCash Flow ValuationShuvro RahmanNo ratings yet

- China To Create Special Currency Test ZoneDocument10 pagesChina To Create Special Currency Test ZoneShuvro RahmanNo ratings yet

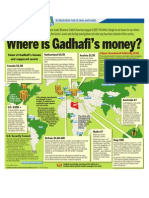

- Where Is Gadhafi's Money?Document1 pageWhere Is Gadhafi's Money?The London Free Press100% (2)

- Fins QuizDocument5 pagesFins QuizAyWestNo ratings yet

- CHAPTER 2: Financial Analysis RatiosDocument15 pagesCHAPTER 2: Financial Analysis RatioslaurenNo ratings yet

- Samsung ThailandDocument25 pagesSamsung Thailandlipzgalz9080No ratings yet

- Option One 2006-1 Jul07Document72 pagesOption One 2006-1 Jul07janisnagobadsNo ratings yet

- Think Outside The Boss Pop Ed SlidesDocument31 pagesThink Outside The Boss Pop Ed SlidesmerrickNo ratings yet

- Strategic Business Objectives of Information SystemsDocument3 pagesStrategic Business Objectives of Information SystemsNike HannaNo ratings yet

- ACC203 - AssignmentDocument2 pagesACC203 - AssignmentHailsey WinterNo ratings yet

- Joint Ventures in Construction Firms in Saudi ArabiaDocument18 pagesJoint Ventures in Construction Firms in Saudi ArabiaEngrAbeer ArifNo ratings yet

- Share Market and Mutual Fund " For: "A Study of Performance and Investors Opinion AboutDocument73 pagesShare Market and Mutual Fund " For: "A Study of Performance and Investors Opinion AboutakshayNo ratings yet

- Naveen Enterprises capital project DCF analysisDocument2 pagesNaveen Enterprises capital project DCF analysisSUBHAJYOTI PALNo ratings yet

- Dubai Islamic Bank (E-Com)Document23 pagesDubai Islamic Bank (E-Com)Zain Ul Abideen100% (1)

- Jindi Enterprises: Presented By-Vikas Tiwari Ankita Pandey Neha AbbhiDocument12 pagesJindi Enterprises: Presented By-Vikas Tiwari Ankita Pandey Neha AbbhilonlinnessNo ratings yet

- International Monetary Systems & Foreign Exchange MarketsDocument47 pagesInternational Monetary Systems & Foreign Exchange MarketsRavi SharmaNo ratings yet

- Real Exchange RatesDocument3 pagesReal Exchange RatesANo ratings yet

- Indian Oil Corporation Rural Retail Outlet Dealer Selection ProcessDocument31 pagesIndian Oil Corporation Rural Retail Outlet Dealer Selection Processaniket025No ratings yet

- Voith DCF Excel FileDocument80 pagesVoith DCF Excel FileVenkat RamanNo ratings yet

- IJRMSS Volume 3, Issue 1 (V) January - March, 2015 PDFDocument112 pagesIJRMSS Volume 3, Issue 1 (V) January - March, 2015 PDFempyrealNo ratings yet

- Asignatura:: Analisis FinancieroDocument15 pagesAsignatura:: Analisis FinancieroDaniNo ratings yet

- Coca Cola WarsDocument9 pagesCoca Cola WarsJoseline MillaNo ratings yet

- Checklist For DividendDocument2 pagesChecklist For DividendKhalid MahmoodNo ratings yet

- ITC Annual Report SynopsisDocument3 pagesITC Annual Report SynopsisItti SinghNo ratings yet

- Decision Trees Background NoteDocument14 pagesDecision Trees Background NoteibrahimNo ratings yet

- Narasimham Committee On Banking Sector ReformsDocument4 pagesNarasimham Committee On Banking Sector ReformsZameer Pasha ShaikNo ratings yet