You might also like

- Entrepreneur 1 PDFDocument12 pagesEntrepreneur 1 PDFLiaqat GulzarNo ratings yet

- CGTMSE MMS Final Summer ProjectDocument36 pagesCGTMSE MMS Final Summer ProjectSuresh Kadam50% (4)

- Seed Capital Fund Scheme PDFDocument13 pagesSeed Capital Fund Scheme PDFLatest Laws TeamNo ratings yet

- Dr. Shakuntala Misra Nationa Rehabilitation: Submitted To: Submitted byDocument14 pagesDr. Shakuntala Misra Nationa Rehabilitation: Submitted To: Submitted byshashi shekhar dixitNo ratings yet

- Credit Guarantee Fund Scheme For MICRO AND SMALL ENTERPRISESDocument2 pagesCredit Guarantee Fund Scheme For MICRO AND SMALL ENTERPRISESsachinoilNo ratings yet

- Inc42 Media: Skip To ContentDocument39 pagesInc42 Media: Skip To Contentshashi shekhar dixitNo ratings yet

- FDocument5 pagesF86sujeetsinghNo ratings yet

- Prime Minister's Employment Generation Programme (PMEGP) - Ministry of Micro, Small & Medium EnterprisesDocument5 pagesPrime Minister's Employment Generation Programme (PMEGP) - Ministry of Micro, Small & Medium EnterprisesVarun ThakurNo ratings yet

- CSEET Business Environment, CA CS Harish Mathariya, YES Academy For CS, PuneDocument41 pagesCSEET Business Environment, CA CS Harish Mathariya, YES Academy For CS, PuneMayank KhetanNo ratings yet

- CGTMSE Information Booklet 2015Document56 pagesCGTMSE Information Booklet 2015Puneet AgarwalNo ratings yet

- Government Schemes For StartupDocument4 pagesGovernment Schemes For StartupSahil GaudeNo ratings yet

- Credit Guarantee Fund Scheme For Micro and Small EnterprisesDocument3 pagesCredit Guarantee Fund Scheme For Micro and Small EnterprisesSuprio NandyNo ratings yet

- Assignment No 6Document4 pagesAssignment No 61346 EE Omkar PrasadNo ratings yet

- Report On SME Banking Scope in Bangladesh (Part-9) : FindingsDocument5 pagesReport On SME Banking Scope in Bangladesh (Part-9) : Findingsnahidul202No ratings yet

- Impact Evaluation of Prime Minister's Employment Generation ProgramDocument39 pagesImpact Evaluation of Prime Minister's Employment Generation ProgramDhruv JainNo ratings yet

- What Is Microcredit?Document10 pagesWhat Is Microcredit?hiteshNo ratings yet

- Module 4Document7 pagesModule 4Vaidehi ShuklaNo ratings yet

- Mudra Loan Salient Features in EnglishDocument2 pagesMudra Loan Salient Features in EnglishYogish KumbleNo ratings yet

- Challenge Fund For Smes: State Bank of PakistanDocument8 pagesChallenge Fund For Smes: State Bank of PakistanMansoor InvoicemateNo ratings yet

- 07 - Chapter 1 MudraDocument16 pages07 - Chapter 1 Mudrayogesh sharmaNo ratings yet

- Report On Loan Syndication & Financial Services For Fund Based Credit Facility in The Form of Cash CreditDocument76 pagesReport On Loan Syndication & Financial Services For Fund Based Credit Facility in The Form of Cash Creditravishivhare89% (9)

- A Study On IDLC Finance LimitedDocument33 pagesA Study On IDLC Finance LimitedKelly McmillanNo ratings yet

- FP TekunDocument13 pagesFP TekunMaryamKhalilah100% (1)

- Internship Report On Jibon Bima Corporation, BangladeshDocument57 pagesInternship Report On Jibon Bima Corporation, Bangladeshzunayedctg80% (10)

- CGTMSEDocument4 pagesCGTMSEPrasath KumarNo ratings yet

- Practical No. 5Document7 pagesPractical No. 5Omkar KhutwadNo ratings yet

- Schemes For MsmeDocument68 pagesSchemes For MsmeGanesh N100% (1)

- Ede 6 PRDocument6 pagesEde 6 PRsingaporeid006No ratings yet

- PRADHANA MANTRI MUDRA YOJANA-grp12Document22 pagesPRADHANA MANTRI MUDRA YOJANA-grp12Anaswara C ANo ratings yet

- CGTMSEDocument43 pagesCGTMSEAnkur Datta100% (1)

- Introduction of SmedaDocument5 pagesIntroduction of SmedaTƛyyƛb ƛliNo ratings yet

- Can Startups Get Bank Loan Without Any Collateral Security?: Working Capital Loan From BanksDocument3 pagesCan Startups Get Bank Loan Without Any Collateral Security?: Working Capital Loan From BanksrajNo ratings yet

- NABARDDocument40 pagesNABARDJesse LarsenNo ratings yet

- Rural Banking - UpdatesJune17Document59 pagesRural Banking - UpdatesJune17raghuviltapuramNo ratings yet

- Brochure MSME Fin 10-12april 2023 EZDocument3 pagesBrochure MSME Fin 10-12april 2023 EZamit choudharyNo ratings yet

- MSMEDocument7 pagesMSMERitika SharmaNo ratings yet

- An Easy Guide On Sme Asaan Finance Scheme (Saaf) For Lending To Smes Without CollateralDocument16 pagesAn Easy Guide On Sme Asaan Finance Scheme (Saaf) For Lending To Smes Without CollateralRakesh KumarNo ratings yet

- EDE MicroprojectDocument15 pagesEDE MicroprojectNitesh Gowardhan BorlaNo ratings yet

- Sip ProjectDocument114 pagesSip ProjectSubham JaiswalNo ratings yet

- Model EducationDocument5 pagesModel EducationHASNEIN SADIKOTNo ratings yet

- Skill Loan Scheme - Ministry of Skill Development and Entrepreneurship - Goverment of IndiaDocument2 pagesSkill Loan Scheme - Ministry of Skill Development and Entrepreneurship - Goverment of IndiaSailesh NimmagaddaNo ratings yet

- Summer Training ReportDocument119 pagesSummer Training ReportSALONI KHANDELWALNo ratings yet

- History of Stand Up IndiaDocument15 pagesHistory of Stand Up IndiaPragathi MittalNo ratings yet

- Chapter 5 CGTMSEDocument17 pagesChapter 5 CGTMSEMikeNo ratings yet

- Mar 102022 Smespd 02 eDocument83 pagesMar 102022 Smespd 02 esalam ahmedNo ratings yet

- PMKVY Guidelines (2016-2020)Document112 pagesPMKVY Guidelines (2016-2020)Shubham ChaudharyNo ratings yet

- PMKVY Scheme BookletDocument10 pagesPMKVY Scheme Bookletdileepkr97No ratings yet

- NMFDCDocument23 pagesNMFDCdeepam2108No ratings yet

- Success Stories 123Document90 pagesSuccess Stories 123Sai KrishnaNo ratings yet

- BASIC Bank Full ReviewDocument6 pagesBASIC Bank Full ReviewJonaed Ashek Md. RobinNo ratings yet

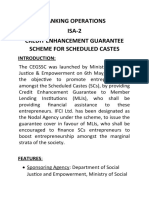

- Banking Operartions Isa-2 (Group-1)Document12 pagesBanking Operartions Isa-2 (Group-1)Analize PintoNo ratings yet

- Module 04 EntDocument116 pagesModule 04 EntBhavik RathodNo ratings yet

- Executive SummaryDocument73 pagesExecutive SummarySachin PacharneNo ratings yet

- Policy Analysis AssignmentDocument6 pagesPolicy Analysis AssignmentAsmitha NNo ratings yet

- MUDRA Disha PandeDocument6 pagesMUDRA Disha Pandepande_dishaNo ratings yet

- Mudra YojnaDocument5 pagesMudra YojnaastikdubeyNo ratings yet

- CSIS - NewGuidelinesDocument4 pagesCSIS - NewGuidelinesPriyam SrivastavaNo ratings yet

- Working Capital FinanceDocument54 pagesWorking Capital FinanceAnkur RazdanNo ratings yet

- CLASS 8th SEC A NewDocument1 pageCLASS 8th SEC A NewSahil BeighNo ratings yet

- Class X FinalDocument1 pageClass X FinalSahil BeighNo ratings yet

- Answer Key For Provided Question PaperDocument1 pageAnswer Key For Provided Question PaperSahil BeighNo ratings yet

- Section B: Little Angels Educational Institute Result For The Computer Exam PaperDocument1 pageSection B: Little Angels Educational Institute Result For The Computer Exam PaperSahil BeighNo ratings yet

- Computer Result For Class X Section BDocument2 pagesComputer Result For Class X Section BSahil BeighNo ratings yet

- Class X Answer KeyDocument1 pageClass X Answer KeySahil BeighNo ratings yet

- Academic Calendar Even Sem 2020 PDFDocument2 pagesAcademic Calendar Even Sem 2020 PDFSahil BeighNo ratings yet

- Statistica - Statistical Methods III SemDocument2 pagesStatistica - Statistical Methods III SemSahil BeighNo ratings yet

- CLASS 8th Answer KeyDocument1 pageCLASS 8th Answer KeySahil BeighNo ratings yet

- ENCE 603 Management Science Applications in Project Management Lectures 5-7Document70 pagesENCE 603 Management Science Applications in Project Management Lectures 5-7Vindraj ChopdekarNo ratings yet

- Government of Jammu and Kashmir: Labour & Employment Department Civil Secretariat Srinagar/ JammuDocument13 pagesGovernment of Jammu and Kashmir: Labour & Employment Department Civil Secretariat Srinagar/ JammuSahil BeighNo ratings yet

- Comparative Management and Its Effect On International BusinessDocument4 pagesComparative Management and Its Effect On International BusinessSahil BeighNo ratings yet

- Introduction To Operation Research Unit-1Document15 pagesIntroduction To Operation Research Unit-1Sahil BeighNo ratings yet

- CBT Result Corrigendum PDFDocument2 pagesCBT Result Corrigendum PDFSahil BeighNo ratings yet

- Acedamic Calender 2017 18 Autumn SemesterDocument2 pagesAcedamic Calender 2017 18 Autumn SemesterSagun ShresthaNo ratings yet

- Dissertation PPT Digital Marketing by Aarif BashirDocument13 pagesDissertation PPT Digital Marketing by Aarif BashirSahil BeighNo ratings yet

- My Resume For MbaDocument2 pagesMy Resume For MbaSahil BeighNo ratings yet

- Dissertation On Digital Marketing by Aarif BashirDocument17 pagesDissertation On Digital Marketing by Aarif BashirSahil BeighNo ratings yet

- Working Capital Management by ZahidDocument18 pagesWorking Capital Management by ZahidSahil BeighNo ratings yet

- Resume Format NewDocument2 pagesResume Format NewSahil BeighNo ratings yet

- 18.11.19 Exam-1 PDFDocument1 page18.11.19 Exam-1 PDFRupesh MandalNo ratings yet

- Comparative Management and Its Effect On International BusinessDocument4 pagesComparative Management and Its Effect On International BusinessSahil BeighNo ratings yet

- Contract Letter 31 May 2020 To, Sahil Beigh Haygot Services Private Limited (Document2 pagesContract Letter 31 May 2020 To, Sahil Beigh Haygot Services Private Limited (Sahil BeighNo ratings yet

- Jetking Prospectus 2019Document28 pagesJetking Prospectus 2019Rose Maichel0% (1)

- Comparative Management and Its Effect On International BusinessDocument4 pagesComparative Management and Its Effect On International BusinessSahil BeighNo ratings yet

- Mobile Services: Your Account Summary This Month'S ChargesDocument2 pagesMobile Services: Your Account Summary This Month'S ChargesSahil BeighNo ratings yet

- PDF PDFDocument1 pagePDF PDFSahil BeighNo ratings yet

- Earthwork: Topic #625-000-007 Plans Preparation Manual, Volume 1 January 1, 2017Document16 pagesEarthwork: Topic #625-000-007 Plans Preparation Manual, Volume 1 January 1, 2017Kiflom BirhaneNo ratings yet

- Le KMR 18 PDFDocument8 pagesLe KMR 18 PDFSahil BeighNo ratings yet

- Tape ScriptsDocument52 pagesTape ScriptstatyanaNo ratings yet

- Scholarships S. No Scholarships Commonwealth Scholarship ProgrammeDocument3 pagesScholarships S. No Scholarships Commonwealth Scholarship ProgrammeAsad HussainNo ratings yet

- E-02-PN Qualification Standard For Diploma in Engineering NQF Level 6 20Document25 pagesE-02-PN Qualification Standard For Diploma in Engineering NQF Level 6 20shalona behariNo ratings yet

- East LA College - 9.4 2016 Spring - ScheduleDocument144 pagesEast LA College - 9.4 2016 Spring - ScheduleDushtu_HuloNo ratings yet

- Railway Reservation SystemDocument34 pagesRailway Reservation SystemTHANIGAINATHAN.G.D 10A3No ratings yet

- UserGuide2018 508 PDFDocument95 pagesUserGuide2018 508 PDFStormm Van RooiNo ratings yet

- Engineering 2010Document326 pagesEngineering 2010Sahand HussainNo ratings yet

- NHDC Limited: Sl. No Designation / Grade / Pay Scale MinimumqualificationDocument6 pagesNHDC Limited: Sl. No Designation / Grade / Pay Scale MinimumqualificationKrishna MyakalaNo ratings yet

- 78 308 PBDocument119 pages78 308 PBАнна ШаповаловаNo ratings yet

- Guidelines For Credit Accumulation, Grade Point Average and Degree Classification - 1Document5 pagesGuidelines For Credit Accumulation, Grade Point Average and Degree Classification - 1vita bandaNo ratings yet

- Advantages of Taking Up Stem in Senior High School: Preparation For CollegeDocument45 pagesAdvantages of Taking Up Stem in Senior High School: Preparation For CollegeTeam BEE100% (1)

- Univotec BTECH-ICT-HAND BOOKDocument17 pagesUnivotec BTECH-ICT-HAND BOOKArulkumaran Mahendrarajah0% (1)

- Victor Chironda CV 2019Document4 pagesVictor Chironda CV 2019Alex LebedevNo ratings yet

- Website PHD Prog PDFDocument7 pagesWebsite PHD Prog PDFPreetam DandpatNo ratings yet

- Ee Laws, Codes, and Professional Ethics: Presented By: Aaron L. NambatacDocument5 pagesEe Laws, Codes, and Professional Ethics: Presented By: Aaron L. NambatacAaron NambatacNo ratings yet

- Long Advt. of Junior Lecturer Adv No 02 of 2009-10Document8 pagesLong Advt. of Junior Lecturer Adv No 02 of 2009-10nikhilmyworld6932100% (3)

- GTE Letter - Sangeeta WaibaDocument7 pagesGTE Letter - Sangeeta Waibaraju niraulaNo ratings yet

- Permit To Study FormatDocument2 pagesPermit To Study FormatJayson Asis100% (5)

- Student Name: Shehnum Moazzam - 20201241464 Course Title: Business Communication Submission Date: December 2,2020Document5 pagesStudent Name: Shehnum Moazzam - 20201241464 Course Title: Business Communication Submission Date: December 2,2020Shehnum MoazzamNo ratings yet

- Bulletin of Information For Admission 2020 - 2021: (A Central University) (Accredited 'A' Grade by NAAC)Document62 pagesBulletin of Information For Admission 2020 - 2021: (A Central University) (Accredited 'A' Grade by NAAC)Swadesh KumarNo ratings yet

- EDP BUTEX Intake 3 2023Document4 pagesEDP BUTEX Intake 3 2023babuNo ratings yet

- Property Studies Postgrad Real Estate June 2016Document20 pagesProperty Studies Postgrad Real Estate June 2016takuva03No ratings yet

- Indian Institute of Technology KharagpurDocument66 pagesIndian Institute of Technology KharagpurNyay DarpanNo ratings yet

- What Is Sustainability?Document11 pagesWhat Is Sustainability?Kouame AdjepoleNo ratings yet

- Legal Ethics CasesDocument116 pagesLegal Ethics CasesPrincess Melanie Melendez100% (1)

- Letter of Motivation (Financial Services Management)Document1 pageLetter of Motivation (Financial Services Management)Tanzeel Ur Rahman100% (5)

- Virtual Universigty Prospectus 2017 18Document114 pagesVirtual Universigty Prospectus 2017 18Gulzar Ahmad Rawn0% (1)

- Pec Regulations For Engineering EducationDocument10 pagesPec Regulations For Engineering EducationZeeShan AwAnNo ratings yet

- Mba Project GuidelinesDocument8 pagesMba Project GuidelinesKrishnamohan VaddadiNo ratings yet

- MA-MSc, Spring 2017Document116 pagesMA-MSc, Spring 2017Muhammad BilalNo ratings yet

- Dark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.From EverandDark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.Rating: 4.5 out of 5 stars4.5/5 (110)

- The Age of Magical Overthinking: Notes on Modern IrrationalityFrom EverandThe Age of Magical Overthinking: Notes on Modern IrrationalityRating: 4 out of 5 stars4/5 (24)

- Prisoners of Geography: Ten Maps That Explain Everything About the WorldFrom EverandPrisoners of Geography: Ten Maps That Explain Everything About the WorldRating: 4.5 out of 5 stars4.5/5 (1145)

- 1177 B.C.: The Year Civilization Collapsed: Revised and UpdatedFrom Everand1177 B.C.: The Year Civilization Collapsed: Revised and UpdatedRating: 4.5 out of 5 stars4.5/5 (110)

- Selling the Dream: The Billion-Dollar Industry Bankrupting AmericansFrom EverandSelling the Dream: The Billion-Dollar Industry Bankrupting AmericansRating: 4 out of 5 stars4/5 (17)

- Briefly Perfectly Human: Making an Authentic Life by Getting Real About the EndFrom EverandBriefly Perfectly Human: Making an Authentic Life by Getting Real About the EndNo ratings yet

- The Wicked and the Willing: An F/F Gothic Horror Vampire NovelFrom EverandThe Wicked and the Willing: An F/F Gothic Horror Vampire NovelRating: 4 out of 5 stars4/5 (21)

- Why We Die: The New Science of Aging and the Quest for ImmortalityFrom EverandWhy We Die: The New Science of Aging and the Quest for ImmortalityRating: 4 out of 5 stars4/5 (3)

- If I Did It: Confessions of the KillerFrom EverandIf I Did It: Confessions of the KillerRating: 3 out of 5 stars3/5 (133)

- Cult, A Love Story: Ten Years Inside a Canadian Cult and the Subsequent Long Road of RecoveryFrom EverandCult, A Love Story: Ten Years Inside a Canadian Cult and the Subsequent Long Road of RecoveryRating: 4 out of 5 stars4/5 (44)

- Altamont: The Rolling Stones, the Hells Angels, and the Inside Story of Rock's Darkest DayFrom EverandAltamont: The Rolling Stones, the Hells Angels, and the Inside Story of Rock's Darkest DayRating: 4 out of 5 stars4/5 (25)

- The Exvangelicals: Loving, Living, and Leaving the White Evangelical ChurchFrom EverandThe Exvangelicals: Loving, Living, and Leaving the White Evangelical ChurchRating: 4.5 out of 5 stars4.5/5 (13)

- The Body Is Not an Apology, Second Edition: The Power of Radical Self-LoveFrom EverandThe Body Is Not an Apology, Second Edition: The Power of Radical Self-LoveRating: 4.5 out of 5 stars4.5/5 (367)

- Troubled: A Memoir of Foster Care, Family, and Social ClassFrom EverandTroubled: A Memoir of Foster Care, Family, and Social ClassRating: 4.5 out of 5 stars4.5/5 (26)

- Hey, Hun: Sales, Sisterhood, Supremacy, and the Other Lies Behind Multilevel MarketingFrom EverandHey, Hun: Sales, Sisterhood, Supremacy, and the Other Lies Behind Multilevel MarketingRating: 4 out of 5 stars4/5 (103)

- Disfigured: On Fairy Tales, Disability, and Making SpaceFrom EverandDisfigured: On Fairy Tales, Disability, and Making SpaceRating: 4.5 out of 5 stars4.5/5 (395)

- The Other Significant Others: Reimagining Life with Friendship at the CenterFrom EverandThe Other Significant Others: Reimagining Life with Friendship at the CenterRating: 4 out of 5 stars4/5 (1)

- Perfect Murder, Perfect Town: The Uncensored Story of the JonBenet Murder and the Grand Jury's Search for the TruthFrom EverandPerfect Murder, Perfect Town: The Uncensored Story of the JonBenet Murder and the Grand Jury's Search for the TruthRating: 3.5 out of 5 stars3.5/5 (68)

- Never Chase Men Again: 38 Dating Secrets to Get the Guy, Keep Him Interested, and Prevent Dead-End RelationshipsFrom EverandNever Chase Men Again: 38 Dating Secrets to Get the Guy, Keep Him Interested, and Prevent Dead-End RelationshipsRating: 4.5 out of 5 stars4.5/5 (387)

- Teaching to Transgress: Education as the Practice of FreedomFrom EverandTeaching to Transgress: Education as the Practice of FreedomRating: 5 out of 5 stars5/5 (76)

- American Jezebel: The Uncommon Life of Anne Hutchinson, the Woman Who Defied the PuritansFrom EverandAmerican Jezebel: The Uncommon Life of Anne Hutchinson, the Woman Who Defied the PuritansRating: 3.5 out of 5 stars3.5/5 (66)

- Dark Feminine Energy: The Ultimate Guide To Become a Femme Fatale, Unveil Your Shadow, Decrypt Male Psychology, Enhance Attraction With Magnetic Body Language and Master the Art of SeductionFrom EverandDark Feminine Energy: The Ultimate Guide To Become a Femme Fatale, Unveil Your Shadow, Decrypt Male Psychology, Enhance Attraction With Magnetic Body Language and Master the Art of SeductionRating: 5 out of 5 stars5/5 (1)

- Little Princes: One Man's Promise to Bring Home the Lost Children of NepalFrom EverandLittle Princes: One Man's Promise to Bring Home the Lost Children of NepalNo ratings yet

- The Ancestor's Tale: A Pilgrimage to the Dawn of EvolutionFrom EverandThe Ancestor's Tale: A Pilgrimage to the Dawn of EvolutionRating: 4 out of 5 stars4/5 (811)