You might also like

- Chapter 12 - Returns - NotesDocument15 pagesChapter 12 - Returns - NotesPuran GuptaNo ratings yet

- GST RETURN GUIDEDocument9 pagesGST RETURN GUIDESanthosh K SNo ratings yet

- Everything You Need to Know About GST ReturnsDocument11 pagesEverything You Need to Know About GST ReturnsYukta AgrawalNo ratings yet

- GST Registration Process and ReturnsDocument7 pagesGST Registration Process and ReturnsAkshay KumarNo ratings yet

- Unit 2 - Part III - Returns Under GST - 30!07!2021Document4 pagesUnit 2 - Part III - Returns Under GST - 30!07!2021Milan ChandaranaNo ratings yet

- GST Returns Assessment and Penal ProvisionsDocument9 pagesGST Returns Assessment and Penal ProvisionsAishuNo ratings yet

- GST Return & FilingDocument14 pagesGST Return & Filingjibin samuelNo ratings yet

- Assignmen GST 5Document10 pagesAssignmen GST 5BhavnaNo ratings yet

- Chapter IX of CGST Act Read With CGST Rules, 2017 & Notifications PrescribedDocument26 pagesChapter IX of CGST Act Read With CGST Rules, 2017 & Notifications PrescribedManali PingaleNo ratings yet

- INCOME TAX AND GST. JURAZ-Module 4Document8 pagesINCOME TAX AND GST. JURAZ-Module 4TERZO IncNo ratings yet

- Presentation (2) (1) - 1Document12 pagesPresentation (2) (1) - 1drawback979No ratings yet

- Presentation (2) (1) - 1Document12 pagesPresentation (2) (1) - 1drawback979No ratings yet

- H4 - GST at GVC: Spark For The DayDocument5 pagesH4 - GST at GVC: Spark For The DayKenny PhilipsNo ratings yet

- GST Unit VDocument29 pagesGST Unit VMani Maran123No ratings yet

- GST Returns NotesDocument5 pagesGST Returns NotesvishnureachmeNo ratings yet

- Basics of GST - Day 1Document15 pagesBasics of GST - Day 1raghav sharmaNo ratings yet

- CA Ashish Chaudhary 1Document30 pagesCA Ashish Chaudhary 1sonapakhi nandyNo ratings yet

- Introduction To GST Unit 1 8 Mark Questions.Document4 pagesIntroduction To GST Unit 1 8 Mark Questions.manoharchary157No ratings yet

- Filing GST Returns - A Guide to Understanding Key Compliance RequirementsDocument7 pagesFiling GST Returns - A Guide to Understanding Key Compliance RequirementsJCGCFGCGNo ratings yet

- GST STeps To File ReturnDocument22 pagesGST STeps To File ReturnAnnu KashyapNo ratings yet

- GST - GOODS & Service Tax What Is GSTDocument4 pagesGST - GOODS & Service Tax What Is GSTsubbiah kailasamNo ratings yet

- Key Highlights of India's Model GST LawDocument4 pagesKey Highlights of India's Model GST LawRajula Gurva ReddyNo ratings yet

- Indirect Tax Laws 1Document10 pagesIndirect Tax Laws 1GunjanNo ratings yet

- Types of GST ReturnsDocument5 pagesTypes of GST ReturnsParvathy MNo ratings yet

- GST Presentation 15032019Document113 pagesGST Presentation 15032019Viky AkNo ratings yet

- Unit I.4 - Levy and Collection of GSTDocument38 pagesUnit I.4 - Levy and Collection of GSTFake MailNo ratings yet

- Unit 5 GSTDocument3 pagesUnit 5 GSTNishu KatiyarNo ratings yet

- Complete Guide On Revocation of Cancellation of GST Registration (As Per Latest Notification) - Taxguru - inDocument3 pagesComplete Guide On Revocation of Cancellation of GST Registration (As Per Latest Notification) - Taxguru - insuraj shekhawatNo ratings yet

- Mixed Income - ITRDocument71 pagesMixed Income - ITRMiguel CasimNo ratings yet

- 7tax Administration LectureDocument48 pages7tax Administration LectureHawa MudalaNo ratings yet

- GST Faq by CSDocument6 pagesGST Faq by CSyashj91No ratings yet

- Standardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaDocument29 pagesStandardised PPT On GST: Indirect Taxes Committee The Institute of Chartered Accountants of IndiaManjunathreddy SeshadriNo ratings yet

- Composition Under GSTDocument12 pagesComposition Under GSTSHAMBHU DAYALNo ratings yet

- GST AuditDocument9 pagesGST Auditdhruv MahajanNo ratings yet

- GST Presentation MsmeDocument114 pagesGST Presentation MsmeViky AkNo ratings yet

- Unit 4Document16 pagesUnit 4Abhishek Kumar GuptaNo ratings yet

- GST-603 Unit 5Document3 pagesGST-603 Unit 5GauharNo ratings yet

- LLB GST Notes Unit-4Document15 pagesLLB GST Notes Unit-4It's time to studyNo ratings yet

- Presentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Document44 pagesPresentation On Taxation To The Construction Industry Federation of Zimbabwe (Cifoz)Franco DurantNo ratings yet

- FCI - GST - Manual On Returns and PaymentsDocument30 pagesFCI - GST - Manual On Returns and PaymentsAmber ChaturvediNo ratings yet

- BBA 6th Semester Study Material For GST (Unit III)Document6 pagesBBA 6th Semester Study Material For GST (Unit III)Priya SinghNo ratings yet

- Sei - ItrDocument36 pagesSei - ItrMiguel CasimNo ratings yet

- Issues of Compliance in GSTDocument8 pagesIssues of Compliance in GSTMahiya Ahmad100% (1)

- CENTURION UNIVERSITY GSTDocument32 pagesCENTURION UNIVERSITY GSTBANANI DASNo ratings yet

- Unit 4 GSTDocument13 pagesUnit 4 GSTViral OkNo ratings yet

- BIR Registration RequirementsDocument27 pagesBIR Registration RequirementsCrizziaNo ratings yet

- Tax Law - Penal ProvisionsDocument23 pagesTax Law - Penal ProvisionsArsalan Ahmad100% (1)

- TAX-CPAR Lecture Filing and Penalties Version 2Document23 pagesTAX-CPAR Lecture Filing and Penalties Version 2YamateNo ratings yet

- Taxation Reviewer - REODocument202 pagesTaxation Reviewer - REOtmica7260No ratings yet

- Methods of Accounting: AX Ccounting Eriods AND EthodsDocument11 pagesMethods of Accounting: AX Ccounting Eriods AND EthodsAiron BendañaNo ratings yet

- Summary of Tax RemediesDocument15 pagesSummary of Tax Remediesquinn ezekielNo ratings yet

- 5th REGISTRATION DoneDocument19 pages5th REGISTRATION DoneAli NadafNo ratings yet

- Registration Under GST: The Content of Debit NoteDocument13 pagesRegistration Under GST: The Content of Debit Notegowthami ravinuthalaNo ratings yet

- GST Returns and FormsDocument46 pagesGST Returns and FormsSachin KhapareNo ratings yet

- Benefits of GST ImplementationDocument6 pagesBenefits of GST ImplementationMinhans SrivastavaNo ratings yet

- GST UNIT 3Document22 pagesGST UNIT 3darshansah1990No ratings yet

- Unit:4 GST: By: Simran Jain Assistant Professor GibsDocument46 pagesUnit:4 GST: By: Simran Jain Assistant Professor GibsTushar SrivastavaNo ratings yet

- Income Tax Compliance GuideDocument13 pagesIncome Tax Compliance GuideRomero Joseph AnthonyNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- 1040 Exam Prep: Module II - Basic Tax ConceptsFrom Everand1040 Exam Prep: Module II - Basic Tax ConceptsRating: 1.5 out of 5 stars1.5/5 (2)

- Evaluating Organizational Performance Through Audit ProceduresDocument11 pagesEvaluating Organizational Performance Through Audit ProceduresNagarjuna ReddyNo ratings yet

- Auditing and AssuranceDocument52 pagesAuditing and AssuranceNagarjuna ReddyNo ratings yet

- BAJAJ FINANCE LIMITED Company Overview, Board, ShareholdingDocument12 pagesBAJAJ FINANCE LIMITED Company Overview, Board, ShareholdingNagarjuna ReddyNo ratings yet

- Cpa Audit NotesDocument38 pagesCpa Audit Notesronalddavisc007No ratings yet

- Privatization and Its Benefits Theory and EvidenceDocument57 pagesPrivatization and Its Benefits Theory and EvidenceNagarjuna ReddyNo ratings yet

- Winning Back Customer Trust About Food Hygiene and Bringing Back More Restaurants On To Their PlatformsDocument1 pageWinning Back Customer Trust About Food Hygiene and Bringing Back More Restaurants On To Their PlatformsNagarjuna ReddyNo ratings yet

- Strategy Demographic Psychographic Segmentation StrategiesDocument2 pagesStrategy Demographic Psychographic Segmentation StrategiesNagarjuna ReddyNo ratings yet

- Mutual Fund Assignment (4th July)Document14 pagesMutual Fund Assignment (4th July)Nagarjuna ReddyNo ratings yet

- Privatization, Performance, and Efficiency: A Study of Indian BanksDocument11 pagesPrivatization, Performance, and Efficiency: A Study of Indian BanksNagarjuna ReddyNo ratings yet

- Cash Flow Ans 12.1Document2 pagesCash Flow Ans 12.1Nagarjuna ReddyNo ratings yet

- Year End Store Stock (2011) Mens Shirts 2200Document2 pagesYear End Store Stock (2011) Mens Shirts 2200Nagarjuna ReddyNo ratings yet

- Return: Return What Is GST ReturnDocument3 pagesReturn: Return What Is GST ReturnNagarjuna ReddyNo ratings yet

- R Saiteja-Fpb1921Document278 pagesR Saiteja-Fpb1921Nagarjuna ReddyNo ratings yet

- Info CaseeDocument2 pagesInfo CaseeNagarjuna ReddyNo ratings yet

- GST I - A I: IN Ndia N NtroductionDocument36 pagesGST I - A I: IN Ndia N NtroductionNagarjuna ReddyNo ratings yet

- BRT T3Document5 pagesBRT T3Nagarjuna ReddyNo ratings yet

- Cash Flow Ans 12.1Document2 pagesCash Flow Ans 12.1Nagarjuna ReddyNo ratings yet

- A Study On Drivers of Brand Switching Behaviour of Consumers From Jio To AirtelDocument41 pagesA Study On Drivers of Brand Switching Behaviour of Consumers From Jio To AirtelNagarjuna ReddyNo ratings yet

- Order The Questions Are Posed. in Your Answers, Use The Numbering SystemDocument3 pagesOrder The Questions Are Posed. in Your Answers, Use The Numbering SystemScri BidNo ratings yet

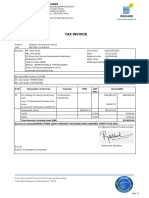

- InvoiceDocument1 pageInvoicealok singhNo ratings yet

- GST Credit Note WB 2212205 A A 65120Document1 pageGST Credit Note WB 2212205 A A 65120web webNo ratings yet

- E-WAY BILL DetailsDocument1 pageE-WAY BILL DetailsrohanNo ratings yet

- 1701a - Page 2Document1 page1701a - Page 2Sygee BotantanNo ratings yet

- Income Taxation ReviewerDocument9 pagesIncome Taxation ReviewerAira MabezaNo ratings yet

- 2023-06-28T14-13 Transaction #6239812736131370-12598287Document1 page2023-06-28T14-13 Transaction #6239812736131370-12598287Neha FayazNo ratings yet

- Tnvat Form WW Fy 15-16Document30 pagesTnvat Form WW Fy 15-16samaadhuNo ratings yet

- RR 8-98Document2 pagesRR 8-98Irene Balmes-LomibaoNo ratings yet

- Payslip Feb 2024Document1 pagePayslip Feb 2024usemask2No ratings yet

- MAT09NATT10028Document5 pagesMAT09NATT10028Helen YousifNo ratings yet

- REVENUE REGULATIONS NO. 25-2002 Issued On December 16, 2002 Amends RRDocument1 pageREVENUE REGULATIONS NO. 25-2002 Issued On December 16, 2002 Amends RRCliff DaquioagNo ratings yet

- 1835-Article Text-9082-1-10-20221214 PDFDocument10 pages1835-Article Text-9082-1-10-20221214 PDFYahengjin DjinNo ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment YearParth GamiNo ratings yet

- p45 Form Download PDFDocument1 pagep45 Form Download PDFJohn JohnNo ratings yet

- TaxationDocument11 pagesTaxationAnonymous ougAoiPZNo ratings yet

- URA Shame List As at 31-12-2015Document2 pagesURA Shame List As at 31-12-2015jadwongscribdNo ratings yet

- Creba Vs Romulo TaxDocument3 pagesCreba Vs Romulo TaxNichole LanuzaNo ratings yet

- Understand India's Tax System ReformsDocument9 pagesUnderstand India's Tax System ReformsAmreen kousarNo ratings yet

- BillDocument1 pageBillUB MalikNo ratings yet

- TwillsPrivilege Receipt 123428636344Document2 pagesTwillsPrivilege Receipt 123428636344Babu Nuvu evaruNo ratings yet

- Julien Day School Fees (2024-25)Document8 pagesJulien Day School Fees (2024-25)anamitrachowdhury89No ratings yet

- BIR Form 1901Document1 pageBIR Form 1901Abdul Nassif Faisal80% (5)

- Obillos V CIRDocument1 pageObillos V CIRjane ling adolfoNo ratings yet

- Republic v. SorianoDocument3 pagesRepublic v. SorianoEllis LagascaNo ratings yet

- Kenya Ports Authority: Tax InvoiceDocument1 pageKenya Ports Authority: Tax InvoiceGeofrey NzomoNo ratings yet

- Mediclaim 80dDocument5 pagesMediclaim 80dPaymaster ServicesNo ratings yet

- Double Taxation Avoidance AgreementDocument8 pagesDouble Taxation Avoidance AgreementSanaur RahmanNo ratings yet

- RMC No. 32-2022Document5 pagesRMC No. 32-2022Shiela Marie MaraonNo ratings yet

- (G1) Highlights of The Train Law Ra 10963 and NIRCDocument37 pages(G1) Highlights of The Train Law Ra 10963 and NIRCFiliusdeiNo ratings yet