You might also like

- Career Rules: How to Choose Right and Get the Life You WantFrom EverandCareer Rules: How to Choose Right and Get the Life You WantNo ratings yet

- Rakesh Jhunjhunwala's views on wealth creation, stock investing and business evaluationDocument8 pagesRakesh Jhunjhunwala's views on wealth creation, stock investing and business evaluationtarachandmara100% (3)

- Success Story of Subhiksha, India's Largest Retail Chain: Ventures and Wipro's Aziz Premji As Its InvestorsDocument7 pagesSuccess Story of Subhiksha, India's Largest Retail Chain: Ventures and Wipro's Aziz Premji As Its Investorsjanamj13No ratings yet

- Mahabharata in Polyester: The Making of the World's Richest Brothers and Their FeudFrom EverandMahabharata in Polyester: The Making of the World's Richest Brothers and Their FeudRating: 3 out of 5 stars3/5 (3)

- My WayDocument53 pagesMy Wayatul8860491212100% (1)

- Success Story of Subhiksha Indias Largest Retail ChainDocument4 pagesSuccess Story of Subhiksha Indias Largest Retail ChainShivam MakkarNo ratings yet

- Interview With Mukesh AmbaniDocument11 pagesInterview With Mukesh Ambanidwarika1987No ratings yet

- SUBHIKSHADocument12 pagesSUBHIKSHAAkshat ChaturvediNo ratings yet

- Success Story PDFDocument56 pagesSuccess Story PDFhemantmNo ratings yet

- Thinking Smart: How to Master Work, Life and Everything In-BetweenFrom EverandThinking Smart: How to Master Work, Life and Everything In-BetweenRating: 4 out of 5 stars4/5 (1)

- Adani SpeechDocument3 pagesAdani SpeechmrckkannadaNo ratings yet

- Investing Over a Cup of Tea: My not so profound thoughts on investing ǀ Beginner’s guide to investing in the stock marketFrom EverandInvesting Over a Cup of Tea: My not so profound thoughts on investing ǀ Beginner’s guide to investing in the stock marketNo ratings yet

- Steve BelkinDocument13 pagesSteve BelkinpodxNo ratings yet

- In Retrospect, This is What it Takes to Build a Successful BusinessFrom EverandIn Retrospect, This is What it Takes to Build a Successful BusinessNo ratings yet

- Managerial Skills Lab File JahnviDocument45 pagesManagerial Skills Lab File JahnviAnkit PandeyNo ratings yet

- Full-time to Fulfilled - The blueprint to success as an independent consultantFrom EverandFull-time to Fulfilled - The blueprint to success as an independent consultantNo ratings yet

- Why Are You Afraid To Become An Enterpreneur?: Remember The Question We Asked You The First Day?Document60 pagesWhy Are You Afraid To Become An Enterpreneur?: Remember The Question We Asked You The First Day?Jupinder KaurNo ratings yet

- What Young India WantsDocument139 pagesWhat Young India WantsbetsyNo ratings yet

- Opportunity Investing: How To Revitalize Urban And Rural Communities With Opportunity FundsFrom EverandOpportunity Investing: How To Revitalize Urban And Rural Communities With Opportunity FundsNo ratings yet

- Despite The Glamour and Fame, Hard-Work Always Comes First in This Job - Says Vinod Verma, Freelance Journalist With BBC, NDTV & Amar UjwalaDocument6 pagesDespite The Glamour and Fame, Hard-Work Always Comes First in This Job - Says Vinod Verma, Freelance Journalist With BBC, NDTV & Amar UjwalaMentor ClubNo ratings yet

- The Safe Investor: How to Make Your Money Grow in a Volatile Global EconomyFrom EverandThe Safe Investor: How to Make Your Money Grow in a Volatile Global EconomyNo ratings yet

- Millionaire Confidential: Discover in This IssueDocument39 pagesMillionaire Confidential: Discover in This IssueAnonymous HsoXPyNo ratings yet

- The Underage CEOs: Fascinating Stories of Young Indians Who Became CEOs in their TwentiesFrom EverandThe Underage CEOs: Fascinating Stories of Young Indians Who Became CEOs in their TwentiesNo ratings yet

- Basant Maheshwari Interview Sept. 2014Document59 pagesBasant Maheshwari Interview Sept. 2014Wayne GonsalvesNo ratings yet

- Stay Hungry Stay Foolish Book SummaryDocument12 pagesStay Hungry Stay Foolish Book SummaryAardityam SharmaNo ratings yet

- L'ENTREPRENEUR June-July 2012 Issue Highlights Introversion in EntrepreneurshipDocument33 pagesL'ENTREPRENEUR June-July 2012 Issue Highlights Introversion in EntrepreneurshipKeyur KhoontNo ratings yet

- Blind Faith: Our Misplaced Trust in the Stock Market and Smarter, Safer Ways to InvestFrom EverandBlind Faith: Our Misplaced Trust in the Stock Market and Smarter, Safer Ways to InvestNo ratings yet

- Interview With PV Subramanyam PDFDocument42 pagesInterview With PV Subramanyam PDFAsif IrfanNo ratings yet

- Journey into Personal Leadership: Positively Impacting over 5,000 LivesFrom EverandJourney into Personal Leadership: Positively Impacting over 5,000 LivesNo ratings yet

- IIMB Alumni Magzin Final - 16!05!2011Document48 pagesIIMB Alumni Magzin Final - 16!05!2011Sridhar DPNo ratings yet

- Satyaveer Pal "To Learn To Read IS TO LIGHT A FIRE Every Syllable That Is Spelled Out, Is A Spark" - Victor HugoDocument2 pagesSatyaveer Pal "To Learn To Read IS TO LIGHT A FIRE Every Syllable That Is Spelled Out, Is A Spark" - Victor Hugorhythem henryNo ratings yet

- Reminiscences of A Technical Analyst Around Dalal Street - DR C K NarayanDocument45 pagesReminiscences of A Technical Analyst Around Dalal Street - DR C K Narayansids_dch100% (1)

- Subhash Chandra: A Great Entrepreneur EverDocument21 pagesSubhash Chandra: A Great Entrepreneur Everchavda_jigs02No ratings yet

- ICICIDocument3 pagesICICIAman kumar singhNo ratings yet

- Reminiscences GADocument41 pagesReminiscences GAanalyst_anil14No ratings yet

- Documents: We're Using Facebook To Personalize Your ExperienceDocument10 pagesDocuments: We're Using Facebook To Personalize Your ExperienceTakwa Un-nadwiNo ratings yet

- Zero To Billions - The Zerodha StoryDocument45 pagesZero To Billions - The Zerodha StoryVacancies ProfessionalsNo ratings yet

- A Biography On Kishore BiyaniDocument41 pagesA Biography On Kishore BiyaniAsifshaikh7566No ratings yet

- The Best Advice I Ever GOT: Jignesh ShahDocument11 pagesThe Best Advice I Ever GOT: Jignesh ShahDisha DishaNo ratings yet

- IT Happened IN Ndia: Book ReviewDocument8 pagesIT Happened IN Ndia: Book ReviewshankyshineNo ratings yet

- Losing One's Business and Starting Over: Sirivat VoravetvuthikunDocument20 pagesLosing One's Business and Starting Over: Sirivat VoravetvuthikunMichio TeraokaNo ratings yet

- IIMA-Day To Day Economics - Satish Y. DeodharDocument110 pagesIIMA-Day To Day Economics - Satish Y. Deodhardarshi7100% (26)

- Graham and Doddsville: Making Heads and Tails of Mohnish PabraiDocument5 pagesGraham and Doddsville: Making Heads and Tails of Mohnish PabraiRudra Goud100% (1)

- Convocation Address: Anil D. Ambani Reliance Industries LimitedDocument7 pagesConvocation Address: Anil D. Ambani Reliance Industries LimitedkalirajgurusamyNo ratings yet

- Ebook India - Young Leaders at Every LevelDocument225 pagesEbook India - Young Leaders at Every LevelkNo ratings yet

- My Previous Transcript View A More Recent LectureDocument9 pagesMy Previous Transcript View A More Recent Lecturesotirisg_1100% (1)

- 01: A.K AzadDocument13 pages01: A.K AzadFaiza Islam IslamNo ratings yet

- NR NarayanamurthyDocument6 pagesNR NarayanamurthyMamta PatelNo ratings yet

- Associating 62110265Document3 pagesAssociating 62110265Kartik DharNo ratings yet

- Asit Baran Pati MoneyControlDocument4 pagesAsit Baran Pati MoneyControlShibnath SadhukhanNo ratings yet

- Robert Kiyosaki - Success StoriesDocument822 pagesRobert Kiyosaki - Success StoriesAiza Jane LumintonNo ratings yet

- Kotak - Q3FY18-Investor PresentationDocument38 pagesKotak - Q3FY18-Investor PresentationDivya MukherjeeNo ratings yet

- Q1FY19 Investor Presentation PDFDocument37 pagesQ1FY19 Investor Presentation PDFDivya MukherjeeNo ratings yet

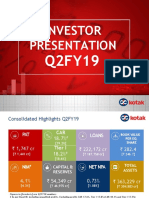

- Kotak - Q2FY19 Investor PresentationDocument37 pagesKotak - Q2FY19 Investor PresentationDivya MukherjeeNo ratings yet

- Q4FY18 Investor Presentation PDFDocument39 pagesQ4FY18 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Q4FY18 Investor Presentation PDFDocument39 pagesQ4FY18 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Q1FY19 Investor Presentation PDFDocument37 pagesQ1FY19 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Kotak - Q3FY19 Investor PresentationDocument37 pagesKotak - Q3FY19 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak Q1FY20 Investor PresentationDocument35 pagesKotak Q1FY20 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak Mahindra Group: Investor PresentationDocument36 pagesKotak Mahindra Group: Investor PresentationDivya MukherjeeNo ratings yet

- Kotak - Q3FY20 Investor PresentationDocument37 pagesKotak - Q3FY20 Investor PresentationDivya MukherjeeNo ratings yet

- Kot KM Hind NK: A A Ra BaDocument303 pagesKot KM Hind NK: A A Ra BaDivya MukherjeeNo ratings yet

- KOTAK - Q2FY20 Investor PresentationDocument34 pagesKOTAK - Q2FY20 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak Securities FY19Document38 pagesKotak Securities FY19ss gNo ratings yet

- Parag Milk FoodsDocument32 pagesParag Milk FoodsDivya MukherjeeNo ratings yet

- AGMnotice-9th July 2020 PDFDocument325 pagesAGMnotice-9th July 2020 PDFNandani AnandNo ratings yet

- Kot KM Hind NK: A A Ra BaDocument303 pagesKot KM Hind NK: A A Ra BaDivya MukherjeeNo ratings yet

- Kotak - Investor Presentation Q1fy21Document38 pagesKotak - Investor Presentation Q1fy21Divya MukherjeeNo ratings yet

- 3227 Dabur Ar 2018 19 PDFDocument292 pages3227 Dabur Ar 2018 19 PDFMahima DangiNo ratings yet

- GROUP QUARTERLY RESULTS SNAPSHOTDocument6 pagesGROUP QUARTERLY RESULTS SNAPSHOTDivya MukherjeeNo ratings yet

- ACL GRC Risk Manager - Usage Guide V1.1Document28 pagesACL GRC Risk Manager - Usage Guide V1.1Rohit ShettyNo ratings yet

- Moon Fast Schedule 2024Document1 pageMoon Fast Schedule 2024mimiemendoza18No ratings yet

- AIOUDocument2 pagesAIOUHoorabwaseemNo ratings yet

- EST I - Literacy Test I (Language)Document20 pagesEST I - Literacy Test I (Language)Mohammed Abdallah100% (1)

- Sonigra Manav Report Finle-Converted EDITEDDocument50 pagesSonigra Manav Report Finle-Converted EDITEDDABHI PARTHNo ratings yet

- College of Physical Therapy Produces Skilled ProfessionalsDocument6 pagesCollege of Physical Therapy Produces Skilled ProfessionalsRia Mae Abellar SalvadorNo ratings yet

- X RayDocument16 pagesX RayMedical Physics2124No ratings yet

- Marulaberry Kicad EbookDocument23 pagesMarulaberry Kicad EbookPhan HaNo ratings yet

- An Overview of The FUPLA 2 Tools: Project DatabaseDocument2 pagesAn Overview of The FUPLA 2 Tools: Project DatabaseJulio Cesar Rojas SaavedraNo ratings yet

- Project Report On AdidasDocument33 pagesProject Report On Adidassanyam73% (37)

- Reversing a String in 8086 Micro Project ReportDocument4 pagesReversing a String in 8086 Micro Project ReportOm IngleNo ratings yet

- Bhakti Trader Ram Pal JiDocument232 pagesBhakti Trader Ram Pal JiplancosterNo ratings yet

- English Extra Conversation Club International Women's DayDocument2 pagesEnglish Extra Conversation Club International Women's Dayevagloria11No ratings yet

- The Interview: P F T IDocument14 pagesThe Interview: P F T IkkkkccccNo ratings yet

- LogDocument119 pagesLogcild MonintjaNo ratings yet

- Eagle Test ReportDocument25 pagesEagle Test ReportMuhammad FahadNo ratings yet

- Serv7107 V05N01 TXT7Document32 pagesServ7107 V05N01 TXT7azry_alqadry100% (6)

- Body Shaming Among School Going AdolesceDocument5 pagesBody Shaming Among School Going AdolesceClara Widya Mulya MNo ratings yet

- Project Report Software and Web Development Company: WWW - Dparksolutions.inDocument12 pagesProject Report Software and Web Development Company: WWW - Dparksolutions.inRavi Kiran Rajbhure100% (1)

- Technical Description: BoilerDocument151 pagesTechnical Description: BoilerÍcaro VianaNo ratings yet

- Corporate Governance in SMEsDocument18 pagesCorporate Governance in SMEsSana DjaanineNo ratings yet

- Financial Accounting IFRS 3rd Edition Weygandt Solutions Manual 1Document8 pagesFinancial Accounting IFRS 3rd Edition Weygandt Solutions Manual 1jacob100% (34)

- 10 Tips To Support ChildrenDocument20 pages10 Tips To Support ChildrenRhe jane AbucejoNo ratings yet

- A ULTIMA ReleaseNotesAxiomV PDFDocument38 pagesA ULTIMA ReleaseNotesAxiomV PDFIVANALTAMARNo ratings yet

- School of Public Health: Haramaya University, ChmsDocument40 pagesSchool of Public Health: Haramaya University, ChmsRida Awwal100% (1)

- PedigreesDocument5 pagesPedigreestpn72hjg88No ratings yet

- Delhi (The Capital of India) : Ebook by Ssac InstituteDocument27 pagesDelhi (The Capital of India) : Ebook by Ssac InstituteAnanjay ChawlaNo ratings yet

- TNG UPDATE InstructionsDocument10 pagesTNG UPDATE InstructionsDiogo Alexandre Crivelari CrivelNo ratings yet

- Service Positioning and DesignDocument3 pagesService Positioning and DesignSaurabh SinhaNo ratings yet

- Philippine Police Report Suicide InvestigationDocument2 pagesPhilippine Police Report Suicide InvestigationPAUL ALDANA82% (34)

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistFrom EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistRating: 4.5 out of 5 stars4.5/5 (73)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- How to Measure Anything: Finding the Value of Intangibles in BusinessFrom EverandHow to Measure Anything: Finding the Value of Intangibles in BusinessRating: 3.5 out of 5 stars3.5/5 (4)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000From EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Rating: 4.5 out of 5 stars4.5/5 (86)

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityFrom EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityRating: 4.5 out of 5 stars4.5/5 (4)

- Joy of Agility: How to Solve Problems and Succeed SoonerFrom EverandJoy of Agility: How to Solve Problems and Succeed SoonerRating: 4 out of 5 stars4/5 (1)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanFrom EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanRating: 4.5 out of 5 stars4.5/5 (79)

- Note Brokering for Profit: Your Complete Work At Home Success ManualFrom EverandNote Brokering for Profit: Your Complete Work At Home Success ManualNo ratings yet

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (34)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)From EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Rating: 4.5 out of 5 stars4.5/5 (4)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 5 out of 5 stars5/5 (2)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthFrom EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthNo ratings yet

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelFrom Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNo ratings yet

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsFrom EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsNo ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet