You might also like

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetShadab khanNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetSivakumar KandasamyNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument33 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetAmitMehtaNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetJitendra PatelNo ratings yet

- Heritage FoodsDocument37 pagesHeritage Foodsravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetASHISH KUMARNo ratings yet

- Saint-Gob. SekurDocument37 pagesSaint-Gob. Sekurprabhusp7No ratings yet

- Guj. State FinDocument37 pagesGuj. State FinBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel InsightsDocument37 pagesSafal Niveshak Stock Analysis Excel InsightsBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This Spreadsheetdivya mNo ratings yet

- Cords CableDocument37 pagesCords CableBandaru NarendrababuNo ratings yet

- Gillette IndiaDocument37 pagesGillette IndiaBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel Guideprabhusp7No ratings yet

- Hero MotocorpDocument41 pagesHero MotocorpShivprasad ShenoyNo ratings yet

- Apoorva LeasingDocument37 pagesApoorva LeasingBandaru NarendrababuNo ratings yet

- Basf IndiaDocument37 pagesBasf IndiaBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetBandaru NarendrababuNo ratings yet

- Ambuja CemDocument37 pagesAmbuja CemsanaNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- HDFC AmcDocument37 pagesHDFC AmcBandaru NarendrababuNo ratings yet

- Astral Poly TechDocument32 pagesAstral Poly TechAbhishek DasNo ratings yet

- Ester IndustriesDocument37 pagesEster Industriesprabhusp7No ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideNeeraj KumarNo ratings yet

- Safal Niveshak Stock Analysis Excel Version 4.0Document37 pagesSafal Niveshak Stock Analysis Excel Version 4.0Ramesh ReddyNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument33 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetManas BanerjeeNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetraghunaththakarNo ratings yet

- Csit ExcelDocument39 pagesCsit ExcelRAJESH GUPTANo ratings yet

- VakrangeeDocument32 pagesVakrangeePriti UpadhyayNo ratings yet

- Safal Niveshak Stock Analysis Excel Version 3.0Document32 pagesSafal Niveshak Stock Analysis Excel Version 3.0MarkusNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideR SURYAANo ratings yet

- Bajaj Finance AnalysisDocument37 pagesBajaj Finance AnalysisUjwal KhandokarNo ratings yet

- Alphageo (India)Document37 pagesAlphageo (India)Bandaru NarendrababuNo ratings yet

- Titan BiotechDocument37 pagesTitan BiotechshridharNo ratings yet

- Fredun PharmaDocument37 pagesFredun PharmaBandaru NarendrababuNo ratings yet

- Apollo SindooriDocument37 pagesApollo Sindooriprabhusp7No ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument32 pagesSafal Niveshak Stock Analysis Excel Guidejitintoteja_82No ratings yet

- Safal Niveshak Stock Analysis Excel Version 3.0Document32 pagesSafal Niveshak Stock Analysis Excel Version 3.0SivaRamanNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- DR Lal Pathlabs (1) Fundamental AnalysisDocument37 pagesDR Lal Pathlabs (1) Fundamental AnalysisGkl AjtNo ratings yet

- UflexDocument45 pagesUflexrishabNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetAnandNo ratings yet

- Stock Analysis Excel Guide for Long Term InvestingDocument37 pagesStock Analysis Excel Guide for Long Term InvestinggirirajNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- Auto AncilliaryDocument41 pagesAuto AncilliaryursvinciNo ratings yet

- Kirl. FerrousDocument37 pagesKirl. Ferrousravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetshridharNo ratings yet

- Apollo TyresDocument37 pagesApollo TyresBandaru NarendrababuNo ratings yet

- Dabur IndiaDocument37 pagesDabur IndiaDeepak SaxenaNo ratings yet

- Hind. UnileverDocument37 pagesHind. UnileveradasdasNo ratings yet

- Cerebra IntegrDocument37 pagesCerebra IntegrBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetPawan ChaturvediNo ratings yet

- Aqua Pumps InfraDocument37 pagesAqua Pumps InfraBandaru NarendrababuNo ratings yet

- Reliance IndustrDocument37 pagesReliance IndustrchaitanyaNo ratings yet

- Bajaj FinservDocument37 pagesBajaj FinservBandaru NarendrababuNo ratings yet

- Zee EntertainmenDocument37 pagesZee Entertainmenprabhusp7No ratings yet

- Allcargo LogistDocument37 pagesAllcargo LogistsanaNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Developing Profitable Trading Strategies - A Beginner’s Guide to Backtesting using Microsoft ExcelFrom EverandDeveloping Profitable Trading Strategies - A Beginner’s Guide to Backtesting using Microsoft ExcelNo ratings yet

- Kotak - Q3FY18-Investor PresentationDocument38 pagesKotak - Q3FY18-Investor PresentationDivya MukherjeeNo ratings yet

- Q1FY19 Investor Presentation PDFDocument37 pagesQ1FY19 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Q4FY18 Investor Presentation PDFDocument39 pagesQ4FY18 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Q4FY18 Investor Presentation PDFDocument39 pagesQ4FY18 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Q1FY19 Investor Presentation PDFDocument37 pagesQ1FY19 Investor Presentation PDFDivya MukherjeeNo ratings yet

- Kotak - Q3FY19 Investor PresentationDocument37 pagesKotak - Q3FY19 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak Q1FY20 Investor PresentationDocument35 pagesKotak Q1FY20 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak Securities FY19Document38 pagesKotak Securities FY19ss gNo ratings yet

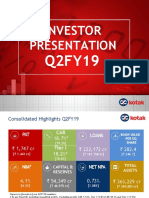

- Kotak - Q2FY19 Investor PresentationDocument37 pagesKotak - Q2FY19 Investor PresentationDivya MukherjeeNo ratings yet

- Kotak - Investor Presentation Q1fy21Document38 pagesKotak - Investor Presentation Q1fy21Divya MukherjeeNo ratings yet

- Kotak - Q3FY20 Investor PresentationDocument37 pagesKotak - Q3FY20 Investor PresentationDivya MukherjeeNo ratings yet

- KOTAK - Q2FY20 Investor PresentationDocument34 pagesKOTAK - Q2FY20 Investor PresentationDivya MukherjeeNo ratings yet

- UdayKotak HemendraKothari RKLaxman InterviwesDocument34 pagesUdayKotak HemendraKothari RKLaxman InterviwesDivya MukherjeeNo ratings yet

- Kotak Mahindra Group: Investor PresentationDocument36 pagesKotak Mahindra Group: Investor PresentationDivya MukherjeeNo ratings yet

- Kot KM Hind NK: A A Ra BaDocument303 pagesKot KM Hind NK: A A Ra BaDivya MukherjeeNo ratings yet

- AGMnotice-9th July 2020 PDFDocument325 pagesAGMnotice-9th July 2020 PDFNandani AnandNo ratings yet

- Kot KM Hind NK: A A Ra BaDocument303 pagesKot KM Hind NK: A A Ra BaDivya MukherjeeNo ratings yet

- GROUP QUARTERLY RESULTS SNAPSHOTDocument6 pagesGROUP QUARTERLY RESULTS SNAPSHOTDivya MukherjeeNo ratings yet

- 3227 Dabur Ar 2018 19 PDFDocument292 pages3227 Dabur Ar 2018 19 PDFMahima DangiNo ratings yet

- Case1 Big Bull CapitalDocument75 pagesCase1 Big Bull CapitalSakshi SharmaNo ratings yet

- Case: Riyadh SportsDocument4 pagesCase: Riyadh SportslackylukNo ratings yet

- Cost Benefit Analysis AllDocument31 pagesCost Benefit Analysis AllBakang NalaropNo ratings yet

- Entrepreneurial Finance 5Th Edition Full ChapterDocument41 pagesEntrepreneurial Finance 5Th Edition Full Chapterjennifer.wilson918100% (25)

- International Financial Management 13 Edition: by Jeff MaduraDocument36 pagesInternational Financial Management 13 Edition: by Jeff MaduraJaime SerranoNo ratings yet

- Corporate RestructuringDocument12 pagesCorporate RestructuringMoguche CollinsNo ratings yet

- Ibig 04 08Document45 pagesIbig 04 08Russell KimNo ratings yet

- Forecasting Stock Returns: What Signals Matter, and What Do They Say Now?Document20 pagesForecasting Stock Returns: What Signals Matter, and What Do They Say Now?madcraft9832No ratings yet

- Chapter 9 - Home WorkDocument8 pagesChapter 9 - Home WorkFaisel MohamedNo ratings yet

- 2020 Level I OnDemandVideo SS13 R41 Module 2Document6 pages2020 Level I OnDemandVideo SS13 R41 Module 2Arturos lanNo ratings yet

- REAL OPTIONS Great BookDocument41 pagesREAL OPTIONS Great BookAnanya KhuranaNo ratings yet

- Nykaa - Fundamental Technical AnalysisDocument6 pagesNykaa - Fundamental Technical Analysiskhyati kaulNo ratings yet

- Introduction to Valuing Securities with DCF and Relative ModelsDocument94 pagesIntroduction to Valuing Securities with DCF and Relative ModelsRaiHan AbeDinNo ratings yet

- Balrampur Sugar MillsDocument49 pagesBalrampur Sugar MillsPiyush Garg100% (1)

- Capital Budgeting PPT 1Document75 pagesCapital Budgeting PPT 1Sakshi SharmaNo ratings yet

- Financial Analysis of Amalgamation Between TCS CMC A Project Report PDFDocument16 pagesFinancial Analysis of Amalgamation Between TCS CMC A Project Report PDFRajeshNo ratings yet

- Developing - A - Fundraising - Strategy - For StartupsDocument11 pagesDeveloping - A - Fundraising - Strategy - For StartupsAnkur JoshiNo ratings yet

- Ranking Investment Proposals: Learning ObjectiveDocument5 pagesRanking Investment Proposals: Learning ObjectivePratibha NagvekarNo ratings yet

- Corporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadDocument38 pagesCorporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadAndrea Howard100% (23)

- TCS Valuation RaportsDocument22 pagesTCS Valuation Raportsmr.rahulgoyal0% (2)

- Tute Solution - CHP 06Document5 pagesTute Solution - CHP 06Aryan KalyanNo ratings yet

- HTTP Viking - Som.yale - Edu Will Finman540 Classnotes Class7Document7 pagesHTTP Viking - Som.yale - Edu Will Finman540 Classnotes Class7corporateboy36596No ratings yet

- FIN311 AssignmrntDocument2 pagesFIN311 Assignmrntsuleman yousafzaiNo ratings yet

- AHL Universe - Recommendation SummaryDocument3 pagesAHL Universe - Recommendation Summarykamran99999No ratings yet

- Methods of Handling Project Risk: Lecture No. 30 Professor C. S. Park Fundamentals of Engineering EconomicsDocument23 pagesMethods of Handling Project Risk: Lecture No. 30 Professor C. S. Park Fundamentals of Engineering EconomicsFeni Ayu LestariNo ratings yet

- Tool #61. The Use of Discount RatesDocument5 pagesTool #61. The Use of Discount RatesRodolfo TupayachiNo ratings yet

- In Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126777Document1 pageIn Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126777Amit PandeyNo ratings yet

- FM2 Notes 3prefinalsDocument13 pagesFM2 Notes 3prefinalsLera KathNo ratings yet

- Chapter - 8: Capital Budgeting DecisionsDocument44 pagesChapter - 8: Capital Budgeting DecisionsAmisha SinghNo ratings yet

- Acquiring an Established Business GuideDocument7 pagesAcquiring an Established Business GuideAjiLalNo ratings yet