You might also like

- Investment Calculator - Ankur WarikooDocument3 pagesInvestment Calculator - Ankur WarikooDivya RaghuvanshiNo ratings yet

- Relieving LetterDocument1 pageRelieving LetterASHISH KUMAR100% (1)

- Safal Niveshak Stock Analysis Excel Version 3.0Document32 pagesSafal Niveshak Stock Analysis Excel Version 3.0SivaRamanNo ratings yet

- Quiz Accounting For Income TaxDocument5 pagesQuiz Accounting For Income TaxCmNo ratings yet

- Developing Profitable Trading Strategies - A Beginner’s Guide to Backtesting using Microsoft ExcelFrom EverandDeveloping Profitable Trading Strategies - A Beginner’s Guide to Backtesting using Microsoft ExcelNo ratings yet

- Capital Today FINAL PPMDocument77 pagesCapital Today FINAL PPMAshish AgrawalNo ratings yet

- Hero MotocorpDocument41 pagesHero MotocorpShivprasad ShenoyNo ratings yet

- Finance Budget - Ankur WarikooDocument26 pagesFinance Budget - Ankur WarikooSimanta KeotNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument32 pagesSafal Niveshak Stock Analysis Excel Guidejitintoteja_82No ratings yet

- Khanna Paper Market Share ReportDocument30 pagesKhanna Paper Market Share ReportIshan Mahajan100% (2)

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetJitendra PatelNo ratings yet

- Bank Reconciliation: Match Books to BankDocument5 pagesBank Reconciliation: Match Books to BankJireh RiveraNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideNeeraj KumarNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- LR Format 1.2Document1 pageLR Format 1.2Ch.Suresh SuryaNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetRavi RanjanNo ratings yet

- Astral Poly TechDocument32 pagesAstral Poly TechAbhishek DasNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetAnandNo ratings yet

- Parag Milk FoodsDocument32 pagesParag Milk FoodsDivya MukherjeeNo ratings yet

- Safal Niveshak Stock Analysis Excel Version 3.0Document32 pagesSafal Niveshak Stock Analysis Excel Version 3.0MarkusNo ratings yet

- Auto AncilliaryDocument41 pagesAuto AncilliaryursvinciNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetShadab khanNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument33 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetManas BanerjeeNo ratings yet

- Apoorva LeasingDocument37 pagesApoorva LeasingBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument33 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetAmitMehtaNo ratings yet

- Csit ExcelDocument39 pagesCsit ExcelRAJESH GUPTANo ratings yet

- Guj. State FinDocument37 pagesGuj. State FinBandaru NarendrababuNo ratings yet

- VakrangeeDocument32 pagesVakrangeePriti UpadhyayNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel Guideprabhusp7No ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This Spreadsheetdivya mNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetraghunaththakarNo ratings yet

- HDFC AmcDocument37 pagesHDFC AmcBandaru NarendrababuNo ratings yet

- Apollo SindooriDocument37 pagesApollo Sindooriprabhusp7No ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetSivakumar KandasamyNo ratings yet

- Cerebra IntegrDocument37 pagesCerebra IntegrBandaru NarendrababuNo ratings yet

- Bajaj Finance AnalysisDocument37 pagesBajaj Finance AnalysisUjwal KhandokarNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetCm ShegrafNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetPawan ChaturvediNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideR SURYAANo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel Guideprabhusp7No ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetPrabhu SpNo ratings yet

- Ester IndustriesDocument37 pagesEster Industriesprabhusp7No ratings yet

- DR Lal Pathlabs (1) Fundamental AnalysisDocument37 pagesDR Lal Pathlabs (1) Fundamental AnalysisGkl AjtNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Titan BiotechDocument37 pagesTitan BiotechshridharNo ratings yet

- Ambuja CemDocument37 pagesAmbuja CemsanaNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel GuideBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- Manappuram FinDocument37 pagesManappuram FinpixogiriNo ratings yet

- Jyoti CNC AutoDocument37 pagesJyoti CNC AutoSubham JainNo ratings yet

- Dabur IndiaDocument37 pagesDabur IndiaDeepak SaxenaNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument35 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetCm ShegrafNo ratings yet

- Hind. UnileverDocument37 pagesHind. UnileveradasdasNo ratings yet

- Safal Niveshak Stock Analysis Excel Version 4.0Document37 pagesSafal Niveshak Stock Analysis Excel Version 4.0Ramesh ReddyNo ratings yet

- Alphageo (India)Document37 pagesAlphageo (India)Bandaru NarendrababuNo ratings yet

- Apollo TyresDocument37 pagesApollo TyresBandaru NarendrababuNo ratings yet

- Heritage FoodsDocument37 pagesHeritage Foodsravi.youNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetravi.youNo ratings yet

- Godrej AgrovetDocument37 pagesGodrej AgrovetBandaru NarendrababuNo ratings yet

- Aqua Pumps InfraDocument37 pagesAqua Pumps InfraBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This Spreadsheetprabhusp7No ratings yet

- Cambridge TechDocument37 pagesCambridge TechBandaru NarendrababuNo ratings yet

- Stock Analysis Excel Guide for Long Term InvestingDocument37 pagesStock Analysis Excel Guide for Long Term InvestinggirirajNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetDocument37 pagesSafal Niveshak Stock Analysis Excel (Ver. 4.0) : How To Use This SpreadsheetshridharNo ratings yet

- Crest VenturesDocument37 pagesCrest VenturesBandaru NarendrababuNo ratings yet

- Safal Niveshak Stock Analysis Excel GuideDocument37 pagesSafal Niveshak Stock Analysis Excel Guideravi.youNo ratings yet

- Marketing Hubspot CustomerDocument1 pageMarketing Hubspot CustomerASHISH KUMARNo ratings yet

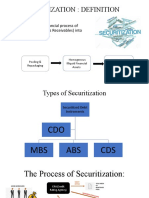

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- Transporter Declaration Format For Non Deduction of Tds in PDFDocument1 pageTransporter Declaration Format For Non Deduction of Tds in PDFASHISH KUMAR67% (3)

- Transporter Declaration Format For Non Deduction of Tds in PDFDocument1 pageTransporter Declaration Format For Non Deduction of Tds in PDFASHISH KUMAR67% (3)

- SA Summary Session2 Group2Document2 pagesSA Summary Session2 Group2ASHISH KUMARNo ratings yet

- Fundamental of Business Intelligence.Document5 pagesFundamental of Business Intelligence.ASHISH KUMARNo ratings yet

- Pricing Strips and Term StructureDocument5 pagesPricing Strips and Term StructureASHISH KUMARNo ratings yet

- 1 1CICI Bank DDM My: Io008 GG 29030 529986Document1 page1 1CICI Bank DDM My: Io008 GG 29030 529986ASHISH KUMARNo ratings yet

- Unit 3 ID - CBDocument62 pagesUnit 3 ID - CBASHISH KUMARNo ratings yet

- IIMBG SA Group 3 Project DetailsDocument7 pagesIIMBG SA Group 3 Project DetailsASHISH KUMARNo ratings yet

- Unit 5 CMDocument22 pagesUnit 5 CMASHISH KUMARNo ratings yet

- Unit 2 FDDocument34 pagesUnit 2 FDASHISH KUMARNo ratings yet

- Declaration 194C NoTDSTransporterDocument1 pageDeclaration 194C NoTDSTransporternitinnawar100% (2)

- Unit 7 DDDocument34 pagesUnit 7 DDASHISH KUMARNo ratings yet

- Unit-4: Information SystemsDocument63 pagesUnit-4: Information SystemsASHISH KUMARNo ratings yet

- Unit 1 FMDocument42 pagesUnit 1 FMASHISH KUMARNo ratings yet

- Electronic PaymentsDocument60 pagesElectronic PaymentsASHISH KUMARNo ratings yet

- Unit 4 WCDocument59 pagesUnit 4 WCASHISH KUMARNo ratings yet

- Powerpoint Templates Powerpoint TemplatesDocument30 pagesPowerpoint Templates Powerpoint TemplatesASHISH KUMARNo ratings yet

- Publish..roskifzan AReviewonOnlineShoppingStudiesDocument13 pagesPublish..roskifzan AReviewonOnlineShoppingStudiesDrey OjemrepNo ratings yet

- Accoun1 SpaceDocument25 pagesAccoun1 SpacePerlas Flordeliza100% (1)

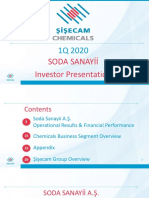

- SODA 2020 Q1 IR PresentationDocument42 pagesSODA 2020 Q1 IR PresentationprasenjitNo ratings yet

- Business Ethics and Integrity A Case Study On 300Document18 pagesBusiness Ethics and Integrity A Case Study On 300LayNo ratings yet

- Team 8 Buyers and Sellers Negotiation AnalysisDocument9 pagesTeam 8 Buyers and Sellers Negotiation AnalysisSWAGATO MUKHERJEENo ratings yet

- Cash BudgetDocument17 pagesCash BudgetElle RaineNo ratings yet

- Module 7: Financials: ENTPLA1 - Thalia AtendidoDocument17 pagesModule 7: Financials: ENTPLA1 - Thalia AtendidoNevan NovaNo ratings yet

- 21 ChapterDocument30 pages21 Chapteribrahim javedNo ratings yet

- Scaler ResumeDocument1 pageScaler ResumeRitik VermaNo ratings yet

- Sherin - CV UpdatedDocument5 pagesSherin - CV Updatedanon_333386456No ratings yet

- Chapter 1 BpoDocument12 pagesChapter 1 BpogkzunigaNo ratings yet

- Accountant UPDATEDocument1 pageAccountant UPDATEyuyukikijulyNo ratings yet

- Sajid Ali CVDocument1 pageSajid Ali CVAvcom TechnologiesNo ratings yet

- Request For ProposalDocument40 pagesRequest For ProposalTender infoNo ratings yet

- 11th Accountancy EM WWW - Tntextbooks.inDocument352 pages11th Accountancy EM WWW - Tntextbooks.inRamesh RengarajanNo ratings yet

- R11Document2 pagesR11Felileo BeltranNo ratings yet

- 10 Managers Across Different IndustriesDocument12 pages10 Managers Across Different IndustriesHema NairNo ratings yet

- Human Resource Management Research Paper PDFDocument5 pagesHuman Resource Management Research Paper PDFqqcxbtbndNo ratings yet

- 4.2 Costs, Scale of Production and Break-Even Analysis - LearnerDocument23 pages4.2 Costs, Scale of Production and Break-Even Analysis - LearnerDhivya Lakshmirajan100% (1)

- Chapter 1 WPS OfficeDocument7 pagesChapter 1 WPS OfficeOmelkhair YahyaNo ratings yet

- Noble Corp 10-Q Report for Quarter Ending Sept 30 2010Document118 pagesNoble Corp 10-Q Report for Quarter Ending Sept 30 2010msim10No ratings yet

- Job DiscerptionDocument3 pagesJob Discerptionblissblock27No ratings yet

- Tingkat Stres Dan Kualitas Tidur Mahasiswa: Keywords: Level of Stress, Stress Management, Sleep QualityDocument6 pagesTingkat Stres Dan Kualitas Tidur Mahasiswa: Keywords: Level of Stress, Stress Management, Sleep QualityJemmy KherisnaNo ratings yet

- ESSENTIAL OILS AND SCENTED CANDLES FINANCIALSDocument12 pagesESSENTIAL OILS AND SCENTED CANDLES FINANCIALSExequiel AmbasingNo ratings yet

- France en Dec. 2022 v3Document37 pagesFrance en Dec. 2022 v3Tarek OsmanNo ratings yet