You might also like

- Transporter Declaration Format For Non Deduction of Tds in PDFDocument1 pageTransporter Declaration Format For Non Deduction of Tds in PDFASHISH KUMAR67% (3)

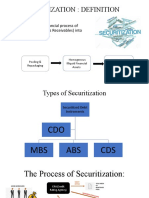

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- SA Summary Session2 Group2Document2 pagesSA Summary Session2 Group2ASHISH KUMARNo ratings yet

- IIMBG SA Group 3 Project DetailsDocument7 pagesIIMBG SA Group 3 Project DetailsASHISH KUMARNo ratings yet

- Pricing Strips and Term StructureDocument5 pagesPricing Strips and Term StructureASHISH KUMARNo ratings yet

- Fundamental of Business Intelligence.Document5 pagesFundamental of Business Intelligence.ASHISH KUMARNo ratings yet

- Unit 5 CMDocument22 pagesUnit 5 CMASHISH KUMARNo ratings yet

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetASHISH KUMARNo ratings yet

- Relieving LetterDocument1 pageRelieving LetterASHISH KUMAR100% (1)

- Unit 3 ID - CBDocument62 pagesUnit 3 ID - CBASHISH KUMARNo ratings yet

- Unit 1 FMDocument42 pagesUnit 1 FMASHISH KUMARNo ratings yet

- Powerpoint Templates Powerpoint TemplatesDocument30 pagesPowerpoint Templates Powerpoint TemplatesASHISH KUMARNo ratings yet

- Electronic PaymentsDocument60 pagesElectronic PaymentsASHISH KUMARNo ratings yet

- Unit 4 WCDocument59 pagesUnit 4 WCASHISH KUMARNo ratings yet

- Unit-4: Information SystemsDocument63 pagesUnit-4: Information SystemsASHISH KUMARNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sample of Exegesis PDFDocument31 pagesSample of Exegesis PDFJoFerNo ratings yet

- De Rama Vs Court of AppealsDocument2 pagesDe Rama Vs Court of AppealsPhilip VistalNo ratings yet

- English For Economics IDocument57 pagesEnglish For Economics IVanadira SekadauNo ratings yet

- Abayon V HRET DigestDocument2 pagesAbayon V HRET DigestDenise DuriasNo ratings yet

- 2.2. Graham CookDocument9 pages2.2. Graham Cookamin138irNo ratings yet

- Garba 2Document9 pagesGarba 2abhisayNo ratings yet

- ML ManualDocument42 pagesML ManualRafa AnanNo ratings yet

- PP Approval Details - B Channel - 2019Document80 pagesPP Approval Details - B Channel - 2019aman3327No ratings yet

- Guide To SyncsortDocument41 pagesGuide To SyncsortShasidhar ReddyNo ratings yet

- Intercellular Communication and Signal TransductionDocument20 pagesIntercellular Communication and Signal TransductionBerkaahh ShoppNo ratings yet

- E Commerce WikipediaDocument20 pagesE Commerce WikipediaUmer AhmedNo ratings yet

- Kinetic Molecular TheoryDocument34 pagesKinetic Molecular TheoryzaneNo ratings yet

- 40 RP Vs SalemDocument3 pages40 RP Vs SalemVanityHughNo ratings yet

- Katarungang Pambarangay - WikipediaDocument13 pagesKatarungang Pambarangay - WikipediaLyn Vyctoria Tarape NaturaNo ratings yet

- Factors Influencing Accounting Course Choice of First Year Accounting Students in UmdcDocument7 pagesFactors Influencing Accounting Course Choice of First Year Accounting Students in UmdcNiñaNo ratings yet

- PRATICE TEST Parts of SpeechDocument7 pagesPRATICE TEST Parts of Speechamin 99No ratings yet

- CrlmaDocument5 pagesCrlmaBibhutiranjan SwainNo ratings yet

- RE GCSE - Important Updates Year 10 Spring 2022Document11 pagesRE GCSE - Important Updates Year 10 Spring 2022nkznghidsnidvNo ratings yet

- En1992 2 ManualDocument86 pagesEn1992 2 ManualMarian Dragos100% (1)

- Clinical Bacteriology: Fawad Mahmood M.Phil. Medical Laboratory SciencesDocument8 pagesClinical Bacteriology: Fawad Mahmood M.Phil. Medical Laboratory SciencesFawad SawabiNo ratings yet

- Contempo Module 5 8 PDF SoftDocument16 pagesContempo Module 5 8 PDF SoftjessaNo ratings yet

- Sources of International LawDocument7 pagesSources of International LawJonathan Valencia0% (1)

- Materi Lanjutan Chapter 7 Kelas 7 Genap, 2021 OKDocument3 pagesMateri Lanjutan Chapter 7 Kelas 7 Genap, 2021 OKAris NdunNo ratings yet

- Leadership Theory PracticeDocument77 pagesLeadership Theory Practice0913314630No ratings yet

- Signal Molecule TrackerDocument4 pagesSignal Molecule Trackerarman_azad_2No ratings yet

- Anansi The SpiderDocument2 pagesAnansi The SpiderStefanie FleenorNo ratings yet

- 109,261,760 Which Makes Up T: Largest Cities in The PhilippinesDocument5 pages109,261,760 Which Makes Up T: Largest Cities in The Philippinescayla mae carlosNo ratings yet

- Ridgerunner - Deborah Christian 2011Document2 pagesRidgerunner - Deborah Christian 2011Knightsbridge~No ratings yet

- Provisions Section 41. Appointment of Receiver.: EstateDocument2 pagesProvisions Section 41. Appointment of Receiver.: EstateMartin Tongco FontanillaNo ratings yet

- Latin Amierca and The Caribbean Choice Board Project Instructions 2016Document3 pagesLatin Amierca and The Caribbean Choice Board Project Instructions 2016api-234947020100% (1)