You might also like

- Survey of Popularity of Credit Cards Issued by Different BanksDocument3 pagesSurvey of Popularity of Credit Cards Issued by Different Bankspritam0000100% (2)

- Winter PRJCT SynopsisDocument15 pagesWinter PRJCT SynopsisNitu Saini100% (1)

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- CardsDocument17 pagesCardsPriyal Shah100% (1)

- Survey of Popularity of Credit Cards Issued by Different Banks PDFDocument3 pagesSurvey of Popularity of Credit Cards Issued by Different Banks PDFArvindKushwaha100% (1)

- Banking Practice Unit 5 What Is A 'Credit Card'Document6 pagesBanking Practice Unit 5 What Is A 'Credit Card'Nandhini VirgoNo ratings yet

- Banking Practice Unit 5 What Is A 'Credit Card'Document6 pagesBanking Practice Unit 5 What Is A 'Credit Card'Nandhini VirgoNo ratings yet

- How to Raise your Credit Score: Proven Strategies to Repair Your Credit Score, Increase Your Credit Score, Overcome Credit Card Debt and Increase Your Credit Limit Volume 3From EverandHow to Raise your Credit Score: Proven Strategies to Repair Your Credit Score, Increase Your Credit Score, Overcome Credit Card Debt and Increase Your Credit Limit Volume 3No ratings yet

- Credit Card PDFDocument15 pagesCredit Card PDFTarun TiwariNo ratings yet

- Credit Repair Guide: How to Fix Credit Score and Remove Negatives From Credit ReportFrom EverandCredit Repair Guide: How to Fix Credit Score and Remove Negatives From Credit ReportRating: 5 out of 5 stars5/5 (5)

- Perception of People Regarding Credit Cards: Presentation ONDocument56 pagesPerception of People Regarding Credit Cards: Presentation ONMani Singh RandhawaNo ratings yet

- Credit and Debit Card Differentiation Assignment ResearchDocument9 pagesCredit and Debit Card Differentiation Assignment Researchsaravana kumarNo ratings yet

- Unit 4 - Consumer Finance and Credit RatingDocument24 pagesUnit 4 - Consumer Finance and Credit RatingAzhar GaziNo ratings yet

- A Report ONDocument68 pagesA Report ONYenkee Adarsh AroraNo ratings yet

- MFIS - Credit CardDocument19 pagesMFIS - Credit Cardmudassar.shirgarcivilNo ratings yet

- Smer PDFDocument50 pagesSmer PDFHarish DesalliNo ratings yet

- Prepared by PC15MBA-034: Basanti BagDocument23 pagesPrepared by PC15MBA-034: Basanti BagSusilPandaNo ratings yet

- Best Cashback Rewards Credit Cards in India Jun 2021 - Offers, ApplyDocument9 pagesBest Cashback Rewards Credit Cards in India Jun 2021 - Offers, ApplyVijay GopalNo ratings yet

- Synopsis: Study of Credit Card in Indian ScenarioDocument12 pagesSynopsis: Study of Credit Card in Indian ScenarioHemraj PatilNo ratings yet

- "A Study On Credit Card": (The Plastic Money)Document86 pages"A Study On Credit Card": (The Plastic Money)Gaurav Gaba100% (1)

- Credit and Debit CardsDocument16 pagesCredit and Debit CardsPriyal Shah100% (1)

- What Are Debitcards??Document10 pagesWhat Are Debitcards??lavanyasundar7No ratings yet

- Project Report On Credit Card1Document81 pagesProject Report On Credit Card1Naveen KNo ratings yet

- Edited Module NotesDocument44 pagesEdited Module NotesWalidahmad AlamNo ratings yet

- Plastic MoneyDocument3 pagesPlastic MoneysachinremaNo ratings yet

- Project Report On Credit Card1Document86 pagesProject Report On Credit Card1Zofail Hassan69% (62)

- Banking Products and Sevices FinalDocument17 pagesBanking Products and Sevices Finaljevesh9No ratings yet

- Project CreditDocument49 pagesProject Creditshailendramishra8286No ratings yet

- Da Afghanistan Bank Afghanistan Payments System: "The National E-Payment Switch of Afghanistan"Document34 pagesDa Afghanistan Bank Afghanistan Payments System: "The National E-Payment Switch of Afghanistan"Asef KhademiNo ratings yet

- Panchnama FormatsDocument2 pagesPanchnama FormatsVikash SharmaNo ratings yet

- Credit Card PresentationDocument24 pagesCredit Card Presentationpradeep367380% (5)

- Credit Card: Dr. Yamini Sharma D.M.SDocument31 pagesCredit Card: Dr. Yamini Sharma D.M.SJames RossNo ratings yet

- Retail BankingDocument25 pagesRetail BankingTrusha Hodiwala80% (5)

- Credit Card BusinessDocument51 pagesCredit Card BusinessAsefNo ratings yet

- Plastic MoneyDocument12 pagesPlastic MoneyJasjot BindraNo ratings yet

- FMS ProjectDocument16 pagesFMS ProjectVinod KumarNo ratings yet

- CREADITDocument64 pagesCREADITSuhailTomarNo ratings yet

- Ecommerce Unit 4Document12 pagesEcommerce Unit 4jhanviNo ratings yet

- Marriage ResumeDocument2 pagesMarriage ResumeSk SharmaNo ratings yet

- Eco 2ND YrDocument23 pagesEco 2ND YrKrishna SaklaniNo ratings yet

- Frauds in Plastic MoneyDocument60 pagesFrauds in Plastic MoneyChitra Salian0% (1)

- Unit 2 - Sbaa7001 Banking Products and ServicesDocument38 pagesUnit 2 - Sbaa7001 Banking Products and ServicesGracyNo ratings yet

- Card Buisiness Crdit Card EtcDocument5 pagesCard Buisiness Crdit Card EtcTarun GargNo ratings yet

- Document 6Document6 pagesDocument 6Yasiru PandigamaNo ratings yet

- Plastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158Document30 pagesPlastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158ramandeeprinkyNo ratings yet

- Axis Bank: Assessment No.1 - Marketing of Financial Services IIDocument8 pagesAxis Bank: Assessment No.1 - Marketing of Financial Services IIPratik MahajanNo ratings yet

- Modern Banking: Measures of The Money Supply, Functions and Types of Financial Institutions, and Modern E-BankingDocument16 pagesModern Banking: Measures of The Money Supply, Functions and Types of Financial Institutions, and Modern E-BankingnripendunandyNo ratings yet

- FinanceDocument5 pagesFinancecrist.jahnskieNo ratings yet

- Akshay Jain HDFC DigitalizationDocument32 pagesAkshay Jain HDFC DigitalizationAkshay JainNo ratings yet

- Plastic Money-The Future Currency: Sunil HarshaDocument10 pagesPlastic Money-The Future Currency: Sunil HarshaMuhammad NaeemNo ratings yet

- Unit 4 Banking MbaDocument18 pagesUnit 4 Banking MbaBadal JaiswalNo ratings yet

- Credit CardsDocument21 pagesCredit Cardsdixita_chotalia3829100% (1)

- Plastic MoneyDocument39 pagesPlastic Moneydakshaangel100% (3)

- Theoritical Framework &literature ReviewDocument27 pagesTheoritical Framework &literature ReviewGelani PradipNo ratings yet

- Debit Card and Credit CardDocument5 pagesDebit Card and Credit Cardbeena antuNo ratings yet

- Transporter Declaration Format For Non Deduction of Tds in PDFDocument1 pageTransporter Declaration Format For Non Deduction of Tds in PDFASHISH KUMAR67% (3)

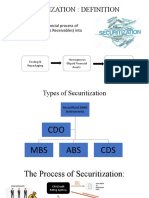

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- Marketing Hubspot CustomerDocument1 pageMarketing Hubspot CustomerASHISH KUMARNo ratings yet

- Transporter Declaration Format For Non Deduction of Tds in PDFDocument1 pageTransporter Declaration Format For Non Deduction of Tds in PDFASHISH KUMAR67% (3)

- 1 1CICI Bank DDM My: Io008 GG 29030 529986Document1 page1 1CICI Bank DDM My: Io008 GG 29030 529986ASHISH KUMARNo ratings yet

- Investment Calculator - Ankur WarikooDocument3 pagesInvestment Calculator - Ankur WarikooDivya RaghuvanshiNo ratings yet

- SA Summary Session2 Group2Document2 pagesSA Summary Session2 Group2ASHISH KUMARNo ratings yet

- Relieving LetterDocument1 pageRelieving LetterASHISH KUMAR100% (1)

- Unit 7 DDDocument34 pagesUnit 7 DDASHISH KUMARNo ratings yet

- Pricing Strips and Term StructureDocument5 pagesPricing Strips and Term StructureASHISH KUMARNo ratings yet

- Finance Budget - Ankur WarikooDocument26 pagesFinance Budget - Ankur WarikooSimanta KeotNo ratings yet

- Fundamental of Business Intelligence.Document5 pagesFundamental of Business Intelligence.ASHISH KUMARNo ratings yet

- IIMBG SA Group 3 Project DetailsDocument7 pagesIIMBG SA Group 3 Project DetailsASHISH KUMARNo ratings yet

- Declaration 194C NoTDSTransporterDocument1 pageDeclaration 194C NoTDSTransporternitinnawar100% (2)

- Safal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetDocument32 pagesSafal Niveshak Stock Analysis Excel (Ver. 3.0) : How To Use This SpreadsheetASHISH KUMARNo ratings yet

- Unit 2 FDDocument34 pagesUnit 2 FDASHISH KUMARNo ratings yet

- Unit 3 ID - CBDocument62 pagesUnit 3 ID - CBASHISH KUMARNo ratings yet

- Unit 5 CMDocument22 pagesUnit 5 CMASHISH KUMARNo ratings yet

- Unit 1 FMDocument42 pagesUnit 1 FMASHISH KUMARNo ratings yet

- Unit-4: Information SystemsDocument63 pagesUnit-4: Information SystemsASHISH KUMARNo ratings yet

- Unit 4 WCDocument59 pagesUnit 4 WCASHISH KUMARNo ratings yet

- Powerpoint Templates Powerpoint TemplatesDocument30 pagesPowerpoint Templates Powerpoint TemplatesASHISH KUMARNo ratings yet

- Business Express Loan Application FormDocument4 pagesBusiness Express Loan Application Formgosmiley67% (3)

- Case Study of Data Mining Application in Banking IndustryDocument9 pagesCase Study of Data Mining Application in Banking Industry37 RAJALAKSHMI RNo ratings yet

- Expenses Tracker 2022 Peter WafulaDocument50 pagesExpenses Tracker 2022 Peter Wafulafrank obimoNo ratings yet

- The 6 Secrets To Build Business CreditDocument8 pagesThe 6 Secrets To Build Business CreditJake Song67% (3)

- Business Rules For Online Fashion Shop Management System: ID Rule Definition Type of Rule Static or Dynamic SourceDocument2 pagesBusiness Rules For Online Fashion Shop Management System: ID Rule Definition Type of Rule Static or Dynamic SourceThanh NguyễnNo ratings yet

- STPM MATHEMATICS M Coursework/Kerja Kursus (Semester 1)Document11 pagesSTPM MATHEMATICS M Coursework/Kerja Kursus (Semester 1)jq75% (4)

- Sample of Reading Toeic TestDocument12 pagesSample of Reading Toeic TesthuyenNo ratings yet

- Role of Sbi & HDFC in Business FinanceDocument47 pagesRole of Sbi & HDFC in Business Financepurusottam_asianpacificNo ratings yet

- Copywriting Gems PDFDocument25 pagesCopywriting Gems PDFKemal SadžakNo ratings yet

- Adr Practical Problems 2019 TypedDocument11 pagesAdr Practical Problems 2019 TypedMamatha RangaswamyNo ratings yet

- PSFK Retail Report - Jun/2010Document84 pagesPSFK Retail Report - Jun/2010Lorenzo MendozaNo ratings yet

- Aspire Budget 2.8 PDFDocument274 pagesAspire Budget 2.8 PDFLucas DinizNo ratings yet

- Airtel Postpaid Bill - Nov - 2023Document5 pagesAirtel Postpaid Bill - Nov - 2023Navdeep Roy100% (2)

- DDDDDocument21 pagesDDDDRed Rapture67% (3)

- Brand Loyalty Programs-Are They ShamsDocument10 pagesBrand Loyalty Programs-Are They ShamsYves BelebenieNo ratings yet

- BANK MUSCAT-Tariff Eng BookDocument14 pagesBANK MUSCAT-Tariff Eng BookmujeebmuscatNo ratings yet

- Tunisia Review PolicyDocument13 pagesTunisia Review PolicyAmna EhsanNo ratings yet

- Bookkeeper, Customer Service, Office Manager, Accounts ReceivablDocument2 pagesBookkeeper, Customer Service, Office Manager, Accounts Receivablapi-76801641No ratings yet

- Document PDFDocument3 pagesDocument PDFVal Escobar MagumunNo ratings yet

- Images - Wise Personal Customer AgreementDocument35 pagesImages - Wise Personal Customer AgreementGabriel VALLESNo ratings yet

- The Ultimate Guide To Starting A Credit Repair Business PDFDocument310 pagesThe Ultimate Guide To Starting A Credit Repair Business PDFNickson Sylvestre100% (16)

- Riba, Gharar and MaysirDocument14 pagesRiba, Gharar and MaysirAhmad Pazil Md Isa93% (14)

- Automatic Receipts WhitepaperDocument35 pagesAutomatic Receipts WhitepapersurveyresponderNo ratings yet

- Cash Flow Analysis Chapter Appendix Cma Adapted Tabcomp inDocument1 pageCash Flow Analysis Chapter Appendix Cma Adapted Tabcomp intrilocksp SinghNo ratings yet

- EducationalflyerDocument28 pagesEducationalflyerDaniel MoraNo ratings yet

- Reception For O'Malley For PresidentDocument2 pagesReception For O'Malley For PresidentSunlight FoundationNo ratings yet

- UAE Cybercrime Law of 2012Document10 pagesUAE Cybercrime Law of 2012Matt J. DuffyNo ratings yet

- Agreement DataTransfer SCHUFA PDFDocument1 pageAgreement DataTransfer SCHUFA PDFElfa RiniNo ratings yet

- Project Work On FOODMANDUDocument19 pagesProject Work On FOODMANDUPrabin ChaudharyNo ratings yet

- I Bet You Thought - Ny FedDocument36 pagesI Bet You Thought - Ny FedK100% (2)