You might also like

- Top 10 Sample Papers Class 12 Accountancy With SolutionDocument110 pagesTop 10 Sample Papers Class 12 Accountancy With Solutionanagha0890% (1)

- AHM13e Chapter - 03 - Solution To Problems and Key To CasesDocument24 pagesAHM13e Chapter - 03 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Assignment 2Document12 pagesAssignment 2Geetu SharmaNo ratings yet

- Chapter 3 ParcorDocument6 pagesChapter 3 Parcornikki sy40% (5)

- Prestige Telephone CompanyDocument8 pagesPrestige Telephone CompanyRiandy Ar RasyidNo ratings yet

- Far460 - Set 1 - Feb 2021 - Suggested SolutionsDocument8 pagesFar460 - Set 1 - Feb 2021 - Suggested SolutionsRuzaikha razaliNo ratings yet

- Plagiarism Declaration Form (T-DF)Document12 pagesPlagiarism Declaration Form (T-DF)Nur HidayahNo ratings yet

- g1 Final Written Answers Bkal1013Document13 pagesg1 Final Written Answers Bkal1013tasya zakariaNo ratings yet

- Accruals and Prepayments in The FinancialDocument3 pagesAccruals and Prepayments in The FinancialRealGenius (Carl)No ratings yet

- Group 5Document8 pagesGroup 5Doreen OngNo ratings yet

- T12 - ABFA1153 (Extra)Document2 pagesT12 - ABFA1153 (Extra)LOO YU HUANGNo ratings yet

- Pure TradersDocument2 pagesPure Tradersrethaxaba82No ratings yet

- LCCI Level One Final AcctDocument2 pagesLCCI Level One Final AcctStpmTutorialClassNo ratings yet

- Intro To FA SS May 2018Document8 pagesIntro To FA SS May 2018Munodawafa ChimhamhiwaNo ratings yet

- IAS 16 SolutionsDocument19 pagesIAS 16 SolutionsAhmad SaleemNo ratings yet

- Tutor6 ACCDocument4 pagesTutor6 ACCFood TraditionalNo ratings yet

- Financial Statements SolutionsDocument6 pagesFinancial Statements SolutionsSyed HaseebNo ratings yet

- Bkal1013 Business Accounting (Group Project)Document19 pagesBkal1013 Business Accounting (Group Project)Chin EnNo ratings yet

- Solution To Compiled QuestionsDocument7 pagesSolution To Compiled Questionslovia mensahNo ratings yet

- FS With AdjustmentsDocument25 pagesFS With AdjustmentsBlack NightNo ratings yet

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Document9 pagesSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudNo ratings yet

- SOlution File For FRDocument38 pagesSOlution File For FRMonirul Islam MoniirrNo ratings yet

- Principles of AccountingDocument7 pagesPrinciples of AccountingDanish MuradNo ratings yet

- Assessment Instructions (PGBM01 22-23 Semester 1)Document7 pagesAssessment Instructions (PGBM01 22-23 Semester 1)Md. Real MiahNo ratings yet

- Final Exam FA36013 Principles of Accounting Answer SheetDocument4 pagesFinal Exam FA36013 Principles of Accounting Answer Sheetjos huaNo ratings yet

- PYQ June 2018Document4 pagesPYQ June 2018Nur Amira NadiaNo ratings yet

- Full Assignment Financial Accounting Semster 6 2021Document10 pagesFull Assignment Financial Accounting Semster 6 2021Nur Syafiqah NurNo ratings yet

- Quiz 3: Profit Before Taxation - s4 (A) 67,069Document5 pagesQuiz 3: Profit Before Taxation - s4 (A) 67,069fujinlim98No ratings yet

- Solutions PDFDocument5 pagesSolutions PDFprim2698No ratings yet

- Business Accounting Quiz 2 (Answers) Updated.Document7 pagesBusiness Accounting Quiz 2 (Answers) Updated.Hareen JuniorNo ratings yet

- Description Income Expenses Assets LiabilitiesDocument12 pagesDescription Income Expenses Assets LiabilitiesNipuna Perera100% (1)

- Unit 12-Question 12-C Sol (2023)Document2 pagesUnit 12-Question 12-C Sol (2023)shirleygebenga020829No ratings yet

- Trial BalanceDocument9 pagesTrial BalanceoluwafunmilolaabiolaNo ratings yet

- AccountingDocument7 pagesAccountingDaniela Pedrosa100% (1)

- Bacc 126 Assignment 1 Aug - Dec 2023Document11 pagesBacc 126 Assignment 1 Aug - Dec 2023TarusengaNo ratings yet

- Acf 211 M 2018Document6 pagesAcf 211 M 2018Bulelwa HarrisNo ratings yet

- Accounting Assigment 1 WordDocument7 pagesAccounting Assigment 1 WordlemisiatulihaleniNo ratings yet

- Mock ExamDocument4 pagesMock ExamAna-Maria GhNo ratings yet

- Revenue Note 2020: Total Revenues 819,000Document9 pagesRevenue Note 2020: Total Revenues 819,000Lemonade Ave. BeverageNo ratings yet

- A222 Tutorial 2QDocument5 pagesA222 Tutorial 2Qchong huisinNo ratings yet

- Acc01b1 Rek1b01 Main PDFDocument10 pagesAcc01b1 Rek1b01 Main PDFLebohang NgubaneNo ratings yet

- III Practice of Horizontal & Verticle Analysis Activity IIIDocument8 pagesIII Practice of Horizontal & Verticle Analysis Activity IIIZarish AzharNo ratings yet

- III Practice of Horizontal & Verticle Analysis Activity IIIDocument8 pagesIII Practice of Horizontal & Verticle Analysis Activity IIIZarish AzharNo ratings yet

- Finacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsDocument5 pagesFinacial Accounting Ii FA260US ASSIGNMENT 1 (5 Group Member Only) Faculty Department Course Course Code Due Date Possible Marks Examiner (S) Moderator InstructionsJohanna AseliNo ratings yet

- August Q1Document3 pagesAugust Q1tengku rilNo ratings yet

- Acc CDocument7 pagesAcc CYaseen MawlaniNo ratings yet

- Plagiarism Declaration Form (T-DF)Document8 pagesPlagiarism Declaration Form (T-DF)Nur HidayahNo ratings yet

- Answer Question 3Document27 pagesAnswer Question 3ummi sabrina100% (1)

- The Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Document5 pagesThe Following Trial Balance Was Extracted From The Books of Craz LTD As at 31 Dec 2014Pham TrangNo ratings yet

- Nur Qaseh SDN BHD Soci CorrectedDocument5 pagesNur Qaseh SDN BHD Soci CorrectedSyza LinaNo ratings yet

- Group 1, Section B - Financial Statement Term PaperDocument13 pagesGroup 1, Section B - Financial Statement Term PapermerakiNo ratings yet

- Profit After Tax: Revenue 25% Contribution Margin (% Change From Last y - 2%Document29 pagesProfit After Tax: Revenue 25% Contribution Margin (% Change From Last y - 2%Henry TranNo ratings yet

- Financial Accounting and Reporting: IFRS - 2016 June MSDocument17 pagesFinancial Accounting and Reporting: IFRS - 2016 June MSMarchella LukitoNo ratings yet

- FS Training 22.11.07Document9 pagesFS Training 22.11.07abigail noahNo ratings yet

- Solution To Q1 Summer 2022Document2 pagesSolution To Q1 Summer 2022dgornik021No ratings yet

- Solution Example 3Document2 pagesSolution Example 3ashish panwarNo ratings yet

- Individual AssignmentDocument22 pagesIndividual AssignmentEda LimNo ratings yet

- Acc106 Assignment 2 Tie Beauty Enterprise FinalDocument15 pagesAcc106 Assignment 2 Tie Beauty Enterprise Finalnur anisNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- AFEDocument7 pagesAFEsarah josephNo ratings yet

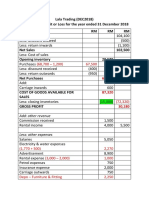

- Lala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTDocument3 pagesLala Trading DEC2018 - SOPL & SOFP DEC2018 AFTER ADJUSTMENTAFIQ RAFIQIN RAHMADNo ratings yet

- BLD 416 Budgeting and Financial Control 1 Lecture Note 2Document9 pagesBLD 416 Budgeting and Financial Control 1 Lecture Note 2Oluwayomi MalomoNo ratings yet

- Securities Brokerage Revenues World Summary: Market Values & Financials by CountryFrom EverandSecurities Brokerage Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Full Assignment hrm1Document7 pagesFull Assignment hrm1Khai Wen OnexoxNo ratings yet

- 2 Logistics in SCM 1Document29 pages2 Logistics in SCM 1Khai Wen OnexoxNo ratings yet

- Supply Chain Technology I: BLCP 201Document14 pagesSupply Chain Technology I: BLCP 201Khai Wen OnexoxNo ratings yet

- Competition: Amphibious Electric Veh Icle CompetitionDocument9 pagesCompetition: Amphibious Electric Veh Icle CompetitionKhai Wen OnexoxNo ratings yet

- Global Supply Chain Operations: September 2015Document24 pagesGlobal Supply Chain Operations: September 2015Khai Wen OnexoxNo ratings yet

- BBMF3083 Portfolio Management: The Investment SettingDocument54 pagesBBMF3083 Portfolio Management: The Investment SettingKhai Wen OnexoxNo ratings yet

- Answers Partnership ExercisesDocument15 pagesAnswers Partnership ExercisesAldrin ZolinaNo ratings yet

- New Annual Report ERC Form DU AO1 1Document97 pagesNew Annual Report ERC Form DU AO1 1Jopan SJNo ratings yet

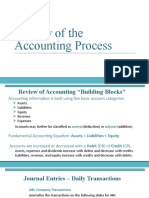

- Review of The Accounting ProcessDocument17 pagesReview of The Accounting ProcessLucy UnNo ratings yet

- Manajemen Asset Bahan DepkeuDocument119 pagesManajemen Asset Bahan DepkeuSyahri ZulkifliNo ratings yet

- Bbfa 4034 Accounting Theory Pratice LatestDocument27 pagesBbfa 4034 Accounting Theory Pratice LatestwensinNo ratings yet

- 12 Accountancy Lyp 2015 Foreign Set1Document42 pages12 Accountancy Lyp 2015 Foreign Set1Ashish GangwalNo ratings yet

- Cash Flow Assignment-TusharDocument8 pagesCash Flow Assignment-TusharAssignments ExpressNo ratings yet

- Practice Multiple Choice Questions For First Test PDFDocument10 pagesPractice Multiple Choice Questions For First Test PDFBringinthehypeNo ratings yet

- Secret Sauce A2 (2020-2021)Document49 pagesSecret Sauce A2 (2020-2021)Eman TahirNo ratings yet

- Common Size Income Statements 2Document7 pagesCommon Size Income Statements 2Aniket KedareNo ratings yet

- Past Adjustments QuestionsDocument6 pagesPast Adjustments QuestionsTanisha JainNo ratings yet

- Fundamentals of Accountancy, Business & Management 1 Second Grading ExaminationDocument6 pagesFundamentals of Accountancy, Business & Management 1 Second Grading ExaminationMc Clent CervantesNo ratings yet

- Acc111 Closing EntriesDocument7 pagesAcc111 Closing Entriesgwyneth palatolonNo ratings yet

- Visa Vertical and Horizontal Analysis ExampleDocument9 pagesVisa Vertical and Horizontal Analysis Examplechad salcidoNo ratings yet

- P1.17 - Equity InvestmentsDocument10 pagesP1.17 - Equity InvestmentsAlmirah's iCPA ReviewNo ratings yet

- Acc 512 Assign 2022Document6 pagesAcc 512 Assign 2022abearkeyanNo ratings yet

- 1458118002cbse Pariksha Accountancy I For 17 March ExamDocument11 pages1458118002cbse Pariksha Accountancy I For 17 March ExamMerlin KNo ratings yet

- Cash Flow Statement StudentDocument60 pagesCash Flow Statement StudentJanine MosatallaNo ratings yet

- Amul DataDocument7 pagesAmul DataPriyanka KotianNo ratings yet

- Ias 1Document6 pagesIas 1Aakanksha SaxenaNo ratings yet

- Lecture07 - Accounting For Tangible Non-Current AssetsDocument47 pagesLecture07 - Accounting For Tangible Non-Current AssetsAnnaNo ratings yet

- Assignment 3 SolutionDocument7 pagesAssignment 3 SolutionAaryaAustNo ratings yet

- TBZ VivzDocument67 pagesTBZ VivzKunal SinghNo ratings yet

- How To Prepare Balance SheetDocument5 pagesHow To Prepare Balance SheetSIddharth CHoudharyNo ratings yet

- Microsoft Intuit Case SolutionDocument22 pagesMicrosoft Intuit Case SolutionHamid S. ParwaniNo ratings yet

- 7110 w18 QP 21 PDFDocument20 pages7110 w18 QP 21 PDFMuhammad ImranNo ratings yet

- CH 05Document73 pagesCH 05Linh Trần Thị KhánhNo ratings yet