You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Comprehensive Pack - RMGDocument83 pagesComprehensive Pack - RMGAmit RajNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Siebel Systems Case Analysis: Group 10 - Section BDocument7 pagesSiebel Systems Case Analysis: Group 10 - Section BAmit RajNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Snapshot-Retail IndustryDocument5 pagesSnapshot-Retail IndustryAmit RajNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Comprehensive Pack - MicrofinanceDocument73 pagesComprehensive Pack - MicrofinanceAmit RajNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Comprehensive Pack - RetailDocument74 pagesComprehensive Pack - RetailAmit RajNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Snapshot Pack - HotelsDocument10 pagesSnapshot Pack - HotelsAmit RajNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- 2) Session 2 PDFDocument21 pages2) Session 2 PDFAmit RajNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Comprehensive Pack - HotelsDocument68 pagesComprehensive Pack - HotelsAmit RajNo ratings yet

- Power Pack - HotelsDocument37 pagesPower Pack - HotelsAmit RajNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- 4) Session 4 PDFDocument40 pages4) Session 4 PDFAmit RajNo ratings yet

- Power Pack - IT ServicesDocument34 pagesPower Pack - IT ServicesAmit RajNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

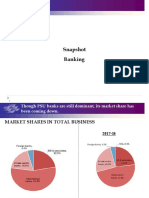

- Snapshot BankingDocument7 pagesSnapshot BankingAmit RajNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Comprehensive Pack - Household AppliancesDocument66 pagesComprehensive Pack - Household AppliancesAmit RajNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Power Pack - Household AppliancesDocument30 pagesPower Pack - Household AppliancesAmit RajNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Chapter 10 Assessment and Key TermsDocument10 pagesChapter 10 Assessment and Key TermsArvee Mark Christian CunananNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Cover Letter For H1B SponsorshipDocument8 pagesCover Letter For H1B Sponsorshiprxfzftckg100% (1)

- Actual Wage Memorandum - Notes and SampleDocument4 pagesActual Wage Memorandum - Notes and SampleJohn DorerNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Ead Expedite Cover LetterDocument5 pagesEad Expedite Cover Letterafiwgzsdf100% (2)

- 1AC - RegionDocument29 pages1AC - RegionMatthew KimNo ratings yet

- Usa Eb-5 Investor Visa Program: Usfc Webinar SeriesDocument17 pagesUsa Eb-5 Investor Visa Program: Usfc Webinar SeriesPushaan SinghNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- NEG Al Ave Itt) : RT PrehgursDocument48 pagesNEG Al Ave Itt) : RT PrehgursHerman HopkinsNo ratings yet

- HNB VisaDocument15 pagesHNB VisaHareesh HareeshNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- All About Nursing AbroadDocument7 pagesAll About Nursing AbroadChristian EstrellaNo ratings yet

- Cover Letter For Change of Status From H4 To F1Document8 pagesCover Letter For Change of Status From H4 To F1emdgjvekgNo ratings yet

- Annual Report 2019: Citizenship and Immigration Services Ombudsman July 12, 2019Document110 pagesAnnual Report 2019: Citizenship and Immigration Services Ombudsman July 12, 2019LA VictorNo ratings yet

- Brenda Koehler Vs InfosysDocument20 pagesBrenda Koehler Vs InfosysTanul ThakurNo ratings yet

- Preparing For A Visa Interview: Review The Following QuestionsDocument6 pagesPreparing For A Visa Interview: Review The Following QuestionsAjay KUmar100% (1)

- Instructions For Application For Employment Authorization: What Is The Purpose of Form I-765?Document27 pagesInstructions For Application For Employment Authorization: What Is The Purpose of Form I-765?Anonymous fFgQaxlgmQNo ratings yet

- Petition For A Nonimmigrant WorkerDocument16 pagesPetition For A Nonimmigrant WorkerulrichNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Aws WJ 201306 PDFDocument170 pagesAws WJ 201306 PDFRenato Barreto100% (1)

- Complaint Against Tata, Class Action DiscriminationDocument23 pagesComplaint Against Tata, Class Action Discriminationmbrown708No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Understanding Immigration Law and Practice Aspen College SeriesDocument61 pagesUnderstanding Immigration Law and Practice Aspen College Seriesjessica.taylor655100% (38)

- Meghana Malviya +91 9131020874 Executive Recruiter & Vendor Management Tekfortune Inc.-Indore, Madhya Pradesh - Dec2018 To PresentDocument2 pagesMeghana Malviya +91 9131020874 Executive Recruiter & Vendor Management Tekfortune Inc.-Indore, Madhya Pradesh - Dec2018 To PresentAditya MujumdarNo ratings yet

- H1B Premium Processing ResumeDocument8 pagesH1B Premium Processing Resumeaflkvapnf100% (1)

- EcomNets Indictment Filed and DocketedDocument27 pagesEcomNets Indictment Filed and DocketedSouthsideCentral100% (1)

- Ac 21 Final RegulationDocument366 pagesAc 21 Final RegulationMehulNo ratings yet

- Western Reserve Health Education/NEOMED Program: Within The Last Two (2) YearsDocument13 pagesWestern Reserve Health Education/NEOMED Program: Within The Last Two (2) YearsRamanpreet Kaur MaanNo ratings yet

- Twitter Bites Into Bitcoin Bait: Accounts of Obama, Biden, Musk, Gates and Others HackedDocument8 pagesTwitter Bites Into Bitcoin Bait: Accounts of Obama, Biden, Musk, Gates and Others HackedGauravNo ratings yet

- I-797c Receipt Notice Scribd - Google SearchDocument2 pagesI-797c Receipt Notice Scribd - Google SearchAshik Ishtiaque EmonNo ratings yet

- Description of Business - Staffing Is An Exciting and Diverse Industry. It Has Blossomed From A Fairly NarrowDocument24 pagesDescription of Business - Staffing Is An Exciting and Diverse Industry. It Has Blossomed From A Fairly NarrowMandeep SharmaNo ratings yet

- EB3 Overview 2018Document11 pagesEB3 Overview 2018Felipe AmorosoNo ratings yet

- Canada Visa Interview QuestionsDocument25 pagesCanada Visa Interview QuestionsCV Dubey100% (3)

- H1B Visa Job Interview Questions and AnswersDocument4 pagesH1B Visa Job Interview Questions and AnswersEphrem zenebe100% (1)

- F1 To H1BDocument2 pagesF1 To H1BRam RamisettiNo ratings yet

- Microsoft 365 Guide to Success: 10 Books in 1 | Kick-start Your Career Learning the Key Information to Master Your Microsoft Office Files to Optimize Your Tasks & Surprise Your Colleagues | Access, Excel, OneDrive, Outlook, PowerPoint, Word, Teams, etc.From EverandMicrosoft 365 Guide to Success: 10 Books in 1 | Kick-start Your Career Learning the Key Information to Master Your Microsoft Office Files to Optimize Your Tasks & Surprise Your Colleagues | Access, Excel, OneDrive, Outlook, PowerPoint, Word, Teams, etc.Rating: 5 out of 5 stars5/5 (3)