You might also like

- Nota k3 LodgingDocument55 pagesNota k3 LodgingsyafawatisamanNo ratings yet

- Introduction To HospitalityDocument139 pagesIntroduction To HospitalityhhsNo ratings yet

- Classifying hotels based on location, size, services, target markets and moreDocument15 pagesClassifying hotels based on location, size, services, target markets and moreRohit LohiyaNo ratings yet

- Classification of HotelsDocument6 pagesClassification of Hotelsabhisheknath80% (5)

- Importance of Hotel IndustryDocument24 pagesImportance of Hotel Industrykavish_nagar24560% (5)

- History: The History of The Hospitality Industry Dates All The WayDocument10 pagesHistory: The History of The Hospitality Industry Dates All The WaySAKET TYAGINo ratings yet

- Lesson 5 EditedDocument14 pagesLesson 5 EditedMichael AndersonNo ratings yet

- Classification of HotelsDocument37 pagesClassification of HotelsShovan HazraNo ratings yet

- Hotel Rooms Division OperationsDocument55 pagesHotel Rooms Division OperationsLorenza DiniNo ratings yet

- Chapter 3 Hotel BusinessDocument30 pagesChapter 3 Hotel BusinesshkunthukhaNo ratings yet

- Accommodations 2Document64 pagesAccommodations 2monika ashokNo ratings yet

- Detailed Project Report On How To Start A Hotel in BhopalDocument39 pagesDetailed Project Report On How To Start A Hotel in BhopalChaitany JoshiNo ratings yet

- Classification of HotelsDocument14 pagesClassification of HotelsEhdina Tindoy100% (1)

- Presentation On Strategy Formulation and Implementation Hospitality Sector (Taj Hotel and Oberoi Hotel)Document16 pagesPresentation On Strategy Formulation and Implementation Hospitality Sector (Taj Hotel and Oberoi Hotel)Romana Aftab100% (1)

- How To Start A Hotel Detailed Project ReportDocument25 pagesHow To Start A Hotel Detailed Project ReportChaitany Joshi77% (39)

- How To Start A Hotel Detailed Project ReportDocument25 pagesHow To Start A Hotel Detailed Project ReportChaitany Joshi100% (1)

- The Leela - FinalDocument2 pagesThe Leela - Finalalensam879100% (2)

- Classification of HotelsDocument17 pagesClassification of HotelsMarwa KorkabNo ratings yet

- Introduction To The Hotel IndustryDocument10 pagesIntroduction To The Hotel IndustryBijan DeyNo ratings yet

- Introduction To The Hotel IndustryDocument10 pagesIntroduction To The Hotel Industryjayeshvk100% (18)

- Notes Chapter 10 The World of LodgingDocument52 pagesNotes Chapter 10 The World of Lodgingsoti4No ratings yet

- Types of Hotel OwnersDocument24 pagesTypes of Hotel OwnersKYNG GAMARINo ratings yet

- The 7Ps of Marketing Strategy at the Luxury Taj Bengal HotelDocument12 pagesThe 7Ps of Marketing Strategy at the Luxury Taj Bengal HotelGolam Mohammed SardarNo ratings yet

- Oberoi HotelsDocument14 pagesOberoi Hotelsvignesh_010675% (4)

- الضيافه 343Document29 pagesالضيافه 343ناصر -No ratings yet

- Marketing Plan of Oberoi HotelsDocument7 pagesMarketing Plan of Oberoi HotelsPooja Vaid100% (7)

- First City Providential College: Rate DesignationsDocument25 pagesFirst City Providential College: Rate DesignationsAngel BambaNo ratings yet

- Topic 5 - AccommodationDocument4 pagesTopic 5 - AccommodationFerlyn Camua MendozaNo ratings yet

- Rating and Grading of HotelsDocument42 pagesRating and Grading of HotelspantkamalinNo ratings yet

- Hotels categorized by location, clientele, length of stay and moreDocument19 pagesHotels categorized by location, clientele, length of stay and moreDhiman Kanti MridhaNo ratings yet

- Classification of HotelsDocument60 pagesClassification of HotelsMandeep KaurNo ratings yet

- Pranika Fof Presentation 3Document13 pagesPranika Fof Presentation 3MortalNo ratings yet

- Hotel Industry GuideDocument76 pagesHotel Industry GuidePratik Devta DhanukaNo ratings yet

- Case Submitted To: Submitted By:: Dr. Nishith Bhatt Ashish Bhuva Dhaval Parmar Dashrath ChaudharyDocument17 pagesCase Submitted To: Submitted By:: Dr. Nishith Bhatt Ashish Bhuva Dhaval Parmar Dashrath ChaudharySonikadevijNo ratings yet

- Hotel Industry - PrathameshDocument15 pagesHotel Industry - Prathameshmahadeojadhav2013No ratings yet

- Promotional Strategies of Leela PalacesDocument10 pagesPromotional Strategies of Leela PalacesAnkush DagorNo ratings yet

- Hme-F oDocument13 pagesHme-F oCRISTINE MANALONo ratings yet

- Avari Ramada - Group 4Document7 pagesAvari Ramada - Group 4Vivek IyerNo ratings yet

- Copy (2) of Marketing of Five Star HotelsDocument84 pagesCopy (2) of Marketing of Five Star HotelsSohil KotichaNo ratings yet

- Lesson 2 - Hospitality IndustryDocument49 pagesLesson 2 - Hospitality Industrymylene apattadNo ratings yet

- Clasifi of HotelsDocument23 pagesClasifi of HotelstjpkNo ratings yet

- Case Study of Diamond Hotel - BartlebyDocument7 pagesCase Study of Diamond Hotel - BartlebyRYAN ALEXANDER HUGONo ratings yet

- Classification of hotels by size, market and servicesDocument3 pagesClassification of hotels by size, market and servicesbishal luitel100% (1)

- Classification of HotelsDocument30 pagesClassification of HotelsSunil KumarNo ratings yet

- BY: Shantimani Sathwara Asst - Prof, PcteDocument30 pagesBY: Shantimani Sathwara Asst - Prof, PcteMeera R. JadhavNo ratings yet

- Written Document Background of The Scenario: 1.introduction of Hospitality IndustryDocument6 pagesWritten Document Background of The Scenario: 1.introduction of Hospitality IndustryPrasan Xangxa RaiNo ratings yet

- Types of Hotels or Classification of Hotel by TypeDocument5 pagesTypes of Hotels or Classification of Hotel by TypeprachiNo ratings yet

- Hotel and Classification of HotelsDocument13 pagesHotel and Classification of HotelsVanezita Camavilca FigueroaNo ratings yet

- Report FinalDocument111 pagesReport FinalShrishNo ratings yet

- How To Start A Hotel Detailed Project ReportDocument26 pagesHow To Start A Hotel Detailed Project ReportNoor Preet KaurNo ratings yet

- T&H - 1Document12 pagesT&H - 1DIVYABEN ANAMINo ratings yet

- Hotel Industry Guide: Classifying Hotels by Size, Market & ServiceDocument6 pagesHotel Industry Guide: Classifying Hotels by Size, Market & ServiceALI ARSLANNo ratings yet

- Classification of HotelsDocument32 pagesClassification of Hotelsrachita1112No ratings yet

- COPAL Partners The Hospitality IndustryDocument7 pagesCOPAL Partners The Hospitality IndustrySantosh ChauhanNo ratings yet

- Hotei and Catering Services FinalDocument39 pagesHotei and Catering Services FinalankitashettyNo ratings yet

- Hotel MarketingDocument66 pagesHotel MarketingAjay SinghNo ratings yet

- The Certified Hospitality ProfessionalFrom EverandThe Certified Hospitality ProfessionalRating: 5 out of 5 stars5/5 (1)

- Snapshot Pack AutoDocument6 pagesSnapshot Pack AutoVaibhav MahajanNo ratings yet

- Siebel Systems Case Analysis on Handling $2.1M Sale NegotiationDocument7 pagesSiebel Systems Case Analysis on Handling $2.1M Sale NegotiationAmit RajNo ratings yet

- Snapshot Pack - Household Appliances PDFDocument11 pagesSnapshot Pack - Household Appliances PDFAmit RajNo ratings yet

- Retail PDFDocument36 pagesRetail PDFVaibhav KhokharNo ratings yet

- Power Pack - Cold ChainDocument27 pagesPower Pack - Cold ChainAmit RajNo ratings yet

- Comprehensive Pack - MicrofinanceDocument73 pagesComprehensive Pack - MicrofinanceAmit RajNo ratings yet

- Snapshot-Retail IndustryDocument5 pagesSnapshot-Retail IndustryAmit RajNo ratings yet

- Snapshot Pack AutoDocument6 pagesSnapshot Pack AutoVaibhav MahajanNo ratings yet

- Comprehensive Media Pack: Televisions, Radio, Newspapers, Films, Digital, Music & OutlookDocument91 pagesComprehensive Media Pack: Televisions, Radio, Newspapers, Films, Digital, Music & OutlookAswin SajeevNo ratings yet

- Comprehensive Pack - RMGDocument83 pagesComprehensive Pack - RMGAmit RajNo ratings yet

- Snapshot Pack - HotelsDocument10 pagesSnapshot Pack - HotelsAmit RajNo ratings yet

- HOUSEHOLD APPLIANCES: MARKET SIZE, GROWTH AND PENETRATIONDocument30 pagesHOUSEHOLD APPLIANCES: MARKET SIZE, GROWTH AND PENETRATIONAmit RajNo ratings yet

- Power Pack - HotelsDocument37 pagesPower Pack - HotelsAmit RajNo ratings yet

- Comprehensive Pack - RetailDocument74 pagesComprehensive Pack - RetailAmit RajNo ratings yet

- Comprehensive Pack - Household AppliancesDocument66 pagesComprehensive Pack - Household AppliancesAmit RajNo ratings yet

- 2) Session 2 PDFDocument21 pages2) Session 2 PDFAmit RajNo ratings yet

- 4) Session 4 PDFDocument40 pages4) Session 4 PDFAmit RajNo ratings yet

- Snapshot Pack - Household Appliances PDFDocument11 pagesSnapshot Pack - Household Appliances PDFAmit RajNo ratings yet

- Power Pack - IT ServicesDocument34 pagesPower Pack - IT ServicesAmit RajNo ratings yet

- Snap Shot Pack - IT ServicesDocument8 pagesSnap Shot Pack - IT ServicesAmit RajNo ratings yet

- Comprehensive Pack BankingDocument79 pagesComprehensive Pack BankingvinodNo ratings yet

- Snapshot Pack - Household Appliances PDFDocument11 pagesSnapshot Pack - Household Appliances PDFAmit RajNo ratings yet

- Comprehensive Pack - Household AppliancesDocument66 pagesComprehensive Pack - Household AppliancesAmit RajNo ratings yet

- Comprehensive Pack - IT Services PDFDocument85 pagesComprehensive Pack - IT Services PDFAmit RajNo ratings yet

- Power Pack - Banking PDFDocument35 pagesPower Pack - Banking PDFAmit RajNo ratings yet

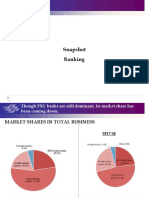

- Snapshot BankingDocument7 pagesSnapshot BankingAmit RajNo ratings yet

- Case Study 1 Hotel ContinentalDocument4 pagesCase Study 1 Hotel ContinentalRoxanne CuizonNo ratings yet

- Course Title Course Code Assignment Code TS-01: Foundation Course in TourismDocument26 pagesCourse Title Course Code Assignment Code TS-01: Foundation Course in TourismIGNOU ASSIGNMENTNo ratings yet

- 9 N 10 DayDocument1 page9 N 10 Dayapi-260839498No ratings yet

- Allied Foam CatalougeDocument27 pagesAllied Foam Catalougesehyong0419No ratings yet

- Scittisch RiteDocument12 pagesScittisch RiteJerryNo ratings yet

- Guangzhou Financial CentreDocument16 pagesGuangzhou Financial CentreRadhika Munshi100% (1)

- BA (Hons) University of Huddersfield, U.K: Module: Accommodation Operations Code: BFI 1033 Module Leader: Asma KhanDocument10 pagesBA (Hons) University of Huddersfield, U.K: Module: Accommodation Operations Code: BFI 1033 Module Leader: Asma KhanAditi ThakurNo ratings yet

- Abu Dhabi's Iconic Leaning Capital Gate TowerDocument3 pagesAbu Dhabi's Iconic Leaning Capital Gate TowerAdeel NiazNo ratings yet

- Spanish for Hotels - Useful PhrasesDocument14 pagesSpanish for Hotels - Useful PhrasesEgla AlishollariNo ratings yet

- Treating Illusions With Kindness. - Kenneth Wapnick, Ph.D.Document16 pagesTreating Illusions With Kindness. - Kenneth Wapnick, Ph.D.Carlos Rodriguez100% (3)

- WxUlw - Document 2 - Draft Business Plan For Swartkops Lodge - Nov 2007Document14 pagesWxUlw - Document 2 - Draft Business Plan For Swartkops Lodge - Nov 2007Fahim Rahman FahimNo ratings yet

- Housekeeping Management ReportDocument21 pagesHousekeeping Management ReportRushi TrivediNo ratings yet

- System Downtime Manual Prochedures 011110 PDFDocument9 pagesSystem Downtime Manual Prochedures 011110 PDFmask72No ratings yet

- Hotel Manager - Job DescriptionDocument2 pagesHotel Manager - Job DescriptionJothee KiiruNo ratings yet

- Pro TipsDocument370 pagesPro TipssteraizNo ratings yet

- 2002 HSE Conference PreviewDocument44 pages2002 HSE Conference PreviewDavid Roberto G100% (1)

- Soal Recount Narrative ProcedureDocument6 pagesSoal Recount Narrative ProcedureBalqist Accyzz AllyyaNo ratings yet

- Prestige Trade Centre - Aerocity - March 2023Document58 pagesPrestige Trade Centre - Aerocity - March 2023gargipurigosaiiNo ratings yet

- No Name of Restaurant P.O.Box Location City Tel. Fax Contact Person Chefs'Mob - No. No.o F Seat S Year EstDocument24 pagesNo Name of Restaurant P.O.Box Location City Tel. Fax Contact Person Chefs'Mob - No. No.o F Seat S Year Estbisankhe2No ratings yet

- Group8 - 1608 - 103662 - HRM - 8 - Group Assignment1 - JD and JS For Hotel Receptionist at Park Hyatt Hotel PDFDocument4 pagesGroup8 - 1608 - 103662 - HRM - 8 - Group Assignment1 - JD and JS For Hotel Receptionist at Park Hyatt Hotel PDFPhan Phúc NguyênNo ratings yet

- La Consolacion College Tanauan Mid-term ExaminationDocument8 pagesLa Consolacion College Tanauan Mid-term ExaminationGene Roy P. Hernandez100% (11)

- Surf & Safe Hotel Organizational StructureDocument8 pagesSurf & Safe Hotel Organizational StructureBlue Anton CruzNo ratings yet

- Differences between Syndicated Estafa and Estafa under the RPCDocument4 pagesDifferences between Syndicated Estafa and Estafa under the RPCBion Henrik PrioloNo ratings yet

- Unit - 1 The Travel and Tourism IndustryDocument21 pagesUnit - 1 The Travel and Tourism IndustrySam ManNo ratings yet

- Desert Magazine 1978 NovemberDocument48 pagesDesert Magazine 1978 Novemberdm1937No ratings yet

- Logistic Note EnglishDocument3 pagesLogistic Note EnglishIR2No ratings yet

- Advertising Assignment 2029mkt - Cam Wiljay Pat and NickDocument13 pagesAdvertising Assignment 2029mkt - Cam Wiljay Pat and Nickapi-320742374No ratings yet

- Gmail - Expedia Travel Confirmation - Wed, Aug 18. - (Itinerary # 72096768606680)Document5 pagesGmail - Expedia Travel Confirmation - Wed, Aug 18. - (Itinerary # 72096768606680)steveNo ratings yet

- Housekeeping Services NCII: Quarter 3Document10 pagesHousekeeping Services NCII: Quarter 3lhenNo ratings yet

- Tatler UK 04.2019Document166 pagesTatler UK 04.2019Lus AmelieNo ratings yet