You might also like

- Grove Master Tech PubsDocument7 pagesGrove Master Tech PubsDenNo ratings yet

- The League ConstitutionDocument6 pagesThe League ConstitutionharrisonmerwinNo ratings yet

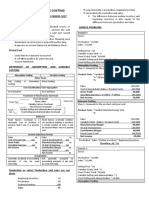

- Absorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualDocument20 pagesAbsorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualPatrick LanceNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFVenise Balia33% (3)

- Mas 9404 Product CostingDocument11 pagesMas 9404 Product CostingEpfie SanchesNo ratings yet

- Afar Government AccountingDocument7 pagesAfar Government AccountingJasmine Lim88% (8)

- Afar Government AccountingDocument7 pagesAfar Government AccountingJasmine Lim88% (8)

- Variable Costing vs. Absorption CostingDocument7 pagesVariable Costing vs. Absorption CostingGêmTürÏngånÖNo ratings yet

- MS 3405 Variable and Absorption CostingDocument5 pagesMS 3405 Variable and Absorption CostingMonica GarciaNo ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Good Governance & Its ComponentsDocument23 pagesGood Governance & Its ComponentsAlgine Escol100% (2)

- Module 1 PPT Audit Process PDFDocument27 pagesModule 1 PPT Audit Process PDFJasmine LimNo ratings yet

- Module 4 Absorption and Variable Costing NotesDocument3 pagesModule 4 Absorption and Variable Costing NotesMadielyn Santarin Miranda100% (3)

- Variable & Absorption Costing LectureDocument11 pagesVariable & Absorption Costing LectureElisha Dhowry PascualNo ratings yet

- Maths F3 KSSM 2019Document132 pagesMaths F3 KSSM 2019蔡卷勋100% (5)

- Muhammad Zakwan Bin Mohd Rafi: Personal ParticularDocument22 pagesMuhammad Zakwan Bin Mohd Rafi: Personal ParticularYvuzi SauraNo ratings yet

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- Absorption and Variable CostingDocument4 pagesAbsorption and Variable CostingChristopher PriceNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- Absorption and Variable CostingDocument5 pagesAbsorption and Variable CostingKIM RAGANo ratings yet

- 03 MAS - Var. & Absorption CostingDocument6 pages03 MAS - Var. & Absorption CostingManwol JangNo ratings yet

- 04 Variable and Absorption CostingDocument8 pages04 Variable and Absorption CostingJunZon VelascoNo ratings yet

- Chapter 7Document12 pagesChapter 7Camille GarciaNo ratings yet

- Absorption Vs VariableDocument10 pagesAbsorption Vs VariableRonie Macasabuang CardosaNo ratings yet

- Rajasthan PDFDocument25 pagesRajasthan PDFVikas MallaNo ratings yet

- Govacctg New PDFDocument190 pagesGovacctg New PDFJasmine Lim100% (1)

- Govacctg New PDFDocument190 pagesGovacctg New PDFJasmine Lim100% (1)

- Voyage Costs ProjectDocument32 pagesVoyage Costs ProjectAndra PurcareaNo ratings yet

- Mas-03: Absorption & Variable CostingDocument4 pagesMas-03: Absorption & Variable CostingClint AbenojaNo ratings yet

- Chapter 9 PDFDocument17 pagesChapter 9 PDFJasmine LimNo ratings yet

- Chapter 9 PDFDocument17 pagesChapter 9 PDFJasmine LimNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Chapter 5 Notes On SalesDocument5 pagesChapter 5 Notes On SalesNikki Estores GonzalesNo ratings yet

- 3MA 03 Absortion and Variable CostingDocument3 pages3MA 03 Absortion and Variable CostingAbigail Regondola BonitaNo ratings yet

- Management Accounting Absorption and Variable Costing Absorption CostingDocument10 pagesManagement Accounting Absorption and Variable Costing Absorption CostingnaddieNo ratings yet

- Absorption (Full Costing) Variable (Direct Costing)Document4 pagesAbsorption (Full Costing) Variable (Direct Costing)Leo Sandy Ambe CuisNo ratings yet

- Absorption Costing GclassDocument4 pagesAbsorption Costing GclassDoromal, Jerome A.No ratings yet

- 3 Absorption Vs Variable CostingDocument16 pages3 Absorption Vs Variable CostingXyril MañagoNo ratings yet

- MAS 04 Absorption CostingDocument6 pagesMAS 04 Absorption CostingJoelyn Grace MontajesNo ratings yet

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFSadile May KayeNo ratings yet

- Notes and Summary in Product Costing With QuizzerDocument12 pagesNotes and Summary in Product Costing With QuizzerCykee Hanna Quizo LumongsodNo ratings yet

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFVenise BaliaNo ratings yet

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFAries Gonzales CaraganNo ratings yet

- MS103 SendingDocument3 pagesMS103 SendingEthel Joy Tolentino GamboaNo ratings yet

- Strategic Management: Topic 3 Variable Costing Versus Absorption CostingDocument20 pagesStrategic Management: Topic 3 Variable Costing Versus Absorption CostingKemerutNo ratings yet

- SIM - Variable and Absorption Costing - 0Document5 pagesSIM - Variable and Absorption Costing - 0lilienesieraNo ratings yet

- Variable and Absorption CostingDocument5 pagesVariable and Absorption CostingAllan Jay CabreraNo ratings yet

- Team Work Makes The Dream Work Acctg15 Var. Absorption CostingDocument4 pagesTeam Work Makes The Dream Work Acctg15 Var. Absorption Costinggeorgia cerezoNo ratings yet

- Overview of Absorption and Variable CostingDocument5 pagesOverview of Absorption and Variable CostingJarrelaine SerranoNo ratings yet

- STRATCOST Module 3 ACDC Handouts by KCWDocument36 pagesSTRATCOST Module 3 ACDC Handouts by KCWAhga MoonNo ratings yet

- ACCTG 42 Module 3Document5 pagesACCTG 42 Module 3Hazel Grace PaguiaNo ratings yet

- MS Absorption-and-Variable-CostingDocument2 pagesMS Absorption-and-Variable-Costingkalloni.zoeNo ratings yet

- MAS.2904 - Variable - Absorption CostingDocument6 pagesMAS.2904 - Variable - Absorption Costingvistalblyss.08No ratings yet

- Variable CostingDocument7 pagesVariable CostingRainie LopezNo ratings yet

- 07 Module 03 AVC PDFDocument12 pages07 Module 03 AVC PDFMarriah Izzabelle Suarez RamadaNo ratings yet

- MAS Product Costing Part IDocument2 pagesMAS Product Costing Part IMary Dale Joie BocalaNo ratings yet

- Costman Variable CostingDocument2 pagesCostman Variable CostingJeremi BernardoNo ratings yet

- Study Guide Variable Versus Absorption CostingDocument9 pagesStudy Guide Variable Versus Absorption CostingFlorie May HizoNo ratings yet

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingDhona Mae FidelNo ratings yet

- D - Absorption and Variable CostingDocument5 pagesD - Absorption and Variable Costingian dizonNo ratings yet

- Our Lady of The Pillar College - CauayanDocument5 pagesOur Lady of The Pillar College - CauayanAnnhtak PNo ratings yet

- Variable and Absorption CostingDocument21 pagesVariable and Absorption Costingbrabz rayNo ratings yet

- COS 103 - Variable Costing ExercisesDocument2 pagesCOS 103 - Variable Costing ExercisesAivie Pangilinan100% (1)

- FINMAN2 GROUP2 Variable and Absorption CostingDocument88 pagesFINMAN2 GROUP2 Variable and Absorption CostingRye Diaz-SanchezNo ratings yet

- Study Guide Variable Versus Absorption CostingDocument8 pagesStudy Guide Variable Versus Absorption CostingFlorie May HizoNo ratings yet

- SCM Unit 4 Variable and Absorption CostingDocument9 pagesSCM Unit 4 Variable and Absorption CostingMargie Garcia LausaNo ratings yet

- MI Synopsis PDFDocument54 pagesMI Synopsis PDFTaufik AhmmedNo ratings yet

- MS 3605 Variable and Absorption CostingDocument5 pagesMS 3605 Variable and Absorption Costingrichshielanghag627No ratings yet

- Chapter 7Document4 pagesChapter 7Mixx MineNo ratings yet

- Variable CostingDocument2 pagesVariable CostingMutia Novita SariNo ratings yet

- M3 Variable Costing As Management ToolDocument6 pagesM3 Variable Costing As Management Toolwingsenigma 00No ratings yet

- MAS Lecture Variable CostingDocument8 pagesMAS Lecture Variable CostingLhoel Delremedios100% (1)

- Ilovepdf Merged MergedDocument12 pagesIlovepdf Merged MergedMa. Trina AnotnioNo ratings yet

- Absorption and Variable CostingDocument4 pagesAbsorption and Variable Costingj financeNo ratings yet

- Financial Market Syllabus - AdayoDocument9 pagesFinancial Market Syllabus - AdayoJasmine LimNo ratings yet

- HOBA - General Procedures-DLSAUDocument25 pagesHOBA - General Procedures-DLSAUJasmine LimNo ratings yet

- Elga and Graduate Outcomes Program Outcomes: College of BusinessDocument7 pagesElga and Graduate Outcomes Program Outcomes: College of BusinessJasmine LimNo ratings yet

- Home Office and Branch AccountingDocument6 pagesHome Office and Branch AccountingJasmine LimNo ratings yet

- Module 1 Importance and Introduction To Financial MarketsDocument13 pagesModule 1 Importance and Introduction To Financial MarketsJasmine LimNo ratings yet

- Business Combination Answer Key PDFDocument15 pagesBusiness Combination Answer Key PDFJasmine LimNo ratings yet

- Business Combination Answer Key PDFDocument15 pagesBusiness Combination Answer Key PDFJasmine LimNo ratings yet

- Acctg-Govnpo-Course PlanDocument7 pagesAcctg-Govnpo-Course PlanJasmine LimNo ratings yet

- Business Combination Discussion and Questions PDFDocument30 pagesBusiness Combination Discussion and Questions PDFJasmine LimNo ratings yet

- Home Office and Branch AccountingDocument6 pagesHome Office and Branch AccountingJasmine LimNo ratings yet

- Business Tax 1 LectureDocument4 pagesBusiness Tax 1 LectureJasmine LimNo ratings yet

- Forefront II Trading CorporationDocument6 pagesForefront II Trading CorporationJasmine LimNo ratings yet

- 5 Negotiable InstrumentsDocument10 pages5 Negotiable InstrumentsJasmine LimNo ratings yet

- Maxbank FilesDocument6 pagesMaxbank FilesD Del SalNo ratings yet

- Ciptadana Equity Market Outlook 2020 Final PDFDocument270 pagesCiptadana Equity Market Outlook 2020 Final PDFBangkit ZuasNo ratings yet

- PinoyME Policy Paper Oct 2010Document24 pagesPinoyME Policy Paper Oct 2010PinoyMe100% (1)

- Abm Recollected Questions 2017Document17 pagesAbm Recollected Questions 2017shirish8272No ratings yet

- Solutions To Chapter 12Document8 pagesSolutions To Chapter 12Luzz LandichoNo ratings yet

- Colorado Coalition For The Homeless CSBG 2018 ApplicationDocument22 pagesColorado Coalition For The Homeless CSBG 2018 ApplicationRICK STANTONNo ratings yet

- Cpec and Regional ConnectivityDocument18 pagesCpec and Regional ConnectivityUzair BashirNo ratings yet

- Establishing Partnerships Among DifferentDocument2 pagesEstablishing Partnerships Among DifferentAbigail AvecillaNo ratings yet

- Belarus Project DetailsDocument2 pagesBelarus Project DetailsNikki KleveNo ratings yet

- Scarcity, Choice, Opportunity Costs, Forms of ExchangeDocument18 pagesScarcity, Choice, Opportunity Costs, Forms of Exchangeanon-583057100% (1)

- Example Did Berkeley 1.11Document4 pagesExample Did Berkeley 1.11panosx87No ratings yet

- Suspect Property Lead Management - Management Mode 01032013Document28 pagesSuspect Property Lead Management - Management Mode 01032013KyleZapantaNo ratings yet

- PAS 7 Statement of Cash FlowsDocument4 pagesPAS 7 Statement of Cash Flowsnash lastNo ratings yet

- Deloitte Touche Tohmatsu LimitedDocument19 pagesDeloitte Touche Tohmatsu LimitedNIHARIKA PARASHARNo ratings yet

- Supply ChainDocument3 pagesSupply ChainSonaEndowNo ratings yet

- CV - Kanai Deb Nath-Economist - Updated-Jan 2019Document7 pagesCV - Kanai Deb Nath-Economist - Updated-Jan 2019debnathkanaiNo ratings yet

- Sales Agreement To Arlene HadapDocument2 pagesSales Agreement To Arlene HadapChay CruzNo ratings yet

- Ipsas 13 LeasesDocument2 pagesIpsas 13 LeasesritunathNo ratings yet

- It 000135879998 2023 00Document1 pageIt 000135879998 2023 00Qavi UddinNo ratings yet

- Forex Money ManagementDocument2 pagesForex Money ManagementДаваасамбуу ЧадраабалNo ratings yet

- Sports Industry in PakistanDocument21 pagesSports Industry in Pakistanmian umarNo ratings yet

- FTRPS1276R 2020-21Document2 pagesFTRPS1276R 2020-21manasNo ratings yet