You might also like

- Enclosure No. 6: Election Application PacketDocument8 pagesEnclosure No. 6: Election Application PacketLen LegaspiNo ratings yet

- Design Thinking ReflectionDocument3 pagesDesign Thinking ReflectionNeil PerlasNo ratings yet

- MMW LESSON 2.1 PropositionsDocument29 pagesMMW LESSON 2.1 PropositionsAngelo Paolo CamotaNo ratings yet

- TRAIN Briefing - Revised Personal Income Tax RatesDocument73 pagesTRAIN Briefing - Revised Personal Income Tax RatesElizaFaithEcleoNo ratings yet

- Income Tax Solutions Manual Chapter SummariesDocument60 pagesIncome Tax Solutions Manual Chapter SummariesPaul Justin Sison Mabao88% (32)

- ENTREPRENEURIAL MIND REPORTING (Production of Goods and Services-Marketing The Small Business)Document18 pagesENTREPRENEURIAL MIND REPORTING (Production of Goods and Services-Marketing The Small Business)IC SevillanoNo ratings yet

- Group Members: Muhammad Asif Mashhood Javed Hamza Akhtar Uzair AslamDocument33 pagesGroup Members: Muhammad Asif Mashhood Javed Hamza Akhtar Uzair Aslamarshad iqbalNo ratings yet

- Accounting Is A Process of Analyzing (Business Transactions, Recording and Communicating Information To UsersDocument12 pagesAccounting Is A Process of Analyzing (Business Transactions, Recording and Communicating Information To UsersAnne BustilloNo ratings yet

- DC Booms Service Training OverviewDocument129 pagesDC Booms Service Training OverviewTamás Leményi100% (1)

- Adjusting EntriesDocument35 pagesAdjusting EntriesEliyah CalucagNo ratings yet

- How To Calculate Gross ProfitDocument3 pagesHow To Calculate Gross ProfitQais WaqasNo ratings yet

- Consumer BehaviorDocument15 pagesConsumer BehaviorSaurabhGuptaNo ratings yet

- Accounting 5 - Closing EntriesDocument13 pagesAccounting 5 - Closing EntriesOanh NguyenNo ratings yet

- Pas 28 Investment in AssociatesDocument1 pagePas 28 Investment in AssociatesrandyNo ratings yet

- Chapter 2: Accounting Equation and The Double-Entry SystemDocument15 pagesChapter 2: Accounting Equation and The Double-Entry SystemSteffane Mae SasutilNo ratings yet

- Fabm2 Sce Week 6-8Document61 pagesFabm2 Sce Week 6-8mary rose aragonNo ratings yet

- Financial StatementDocument5 pagesFinancial StatementJubelle Tacusalme PunzalanNo ratings yet

- Central Concepts of EconomicsDocument37 pagesCentral Concepts of EconomicsRenaldi stwnNo ratings yet

- Lesson 1 CFASDocument14 pagesLesson 1 CFASkenneth coronelNo ratings yet

- Dhaka Epz Factory List & List of Inspected Factories by EIMS For AllianceDocument12 pagesDhaka Epz Factory List & List of Inspected Factories by EIMS For Alliancearman chowdhury100% (4)

- #02 Conceptual FrameworkDocument5 pages#02 Conceptual FrameworkZaaavnn VannnnnNo ratings yet

- Personal Styling Service-Contract - No WatermarkDocument5 pagesPersonal Styling Service-Contract - No WatermarkLexine Emille100% (1)

- Merchandising Income StatementsDocument9 pagesMerchandising Income StatementsJaye RuantoNo ratings yet

- 2020 Ifs InsuranceDocument262 pages2020 Ifs InsuranceSensi CTPrima100% (1)

- Supreme Court Case DigestDocument119 pagesSupreme Court Case DigestCon Pu50% (2)

- Reviewer in FabmDocument5 pagesReviewer in FabmJhoanna Elaine CuizonNo ratings yet

- Analysis of C&F Store's Financial StatementsDocument1 pageAnalysis of C&F Store's Financial Statementsmarissa casareno almueteNo ratings yet

- Scope of Public Finance and its Key ConceptsDocument12 pagesScope of Public Finance and its Key ConceptsshivaniNo ratings yet

- Periodic and Perpetual Inventory SystemDocument19 pagesPeriodic and Perpetual Inventory SystemMichelle RotairoNo ratings yet

- CH 5 - AdjustmentsDocument24 pagesCH 5 - Adjustmentsmuhamad elmiNo ratings yet

- 8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Document7 pages8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Madhu SNo ratings yet

- Contra AccountsDocument6 pagesContra AccountsRaviSankarNo ratings yet

- Writing Up A Case StudyDocument3 pagesWriting Up A Case StudyalliahnahNo ratings yet

- Ch. 1 HW Solutions-9eDocument19 pagesCh. 1 HW Solutions-9eNgNo ratings yet

- FAR 2 NotesDocument3 pagesFAR 2 NotesMARK RANIEL ANTAZONo ratings yet

- Module 1 Lesson 1 - Reading Activity No. 1Document4 pagesModule 1 Lesson 1 - Reading Activity No. 1Sam BayetaNo ratings yet

- ACTBAS 2 - Lecture 1 Merchandising Business and Inventory SystemDocument7 pagesACTBAS 2 - Lecture 1 Merchandising Business and Inventory SystemJason Robert MendozaNo ratings yet

- Semi Final Exam (Accounting)Document4 pagesSemi Final Exam (Accounting)MyyMyy JerezNo ratings yet

- 2009 F-1 Class NotesDocument4 pages2009 F-1 Class NotesgqxgrlNo ratings yet

- IM3 Partnership Operations ProblemsDocument4 pagesIM3 Partnership Operations ProblemsXivaughn Sebastian0% (1)

- Economic History of The PhilippinesDocument4 pagesEconomic History of The PhilippinesClint Agustin M. RoblesNo ratings yet

- ECON - Ch. 1-4Document12 pagesECON - Ch. 1-4CheskaNo ratings yet

- Accounting EquationDocument55 pagesAccounting EquationRahul VermaNo ratings yet

- Strengths and WeaknessDocument2 pagesStrengths and Weaknessapi-482961632No ratings yet

- Business Finance Semi ExamDocument1 pageBusiness Finance Semi ExamAimelenne Jay Aninion100% (1)

- Accountancy Profession and Standards ExplainedDocument13 pagesAccountancy Profession and Standards ExplainedKevin OnaroNo ratings yet

- Measuring National IncomeDocument7 pagesMeasuring National Incomeanora7No ratings yet

- FINC 304 Managerial EconomicsDocument21 pagesFINC 304 Managerial EconomicsJephthah BansahNo ratings yet

- Part II Partnerhsip CorporationDocument101 pagesPart II Partnerhsip CorporationKhrestine ElejidoNo ratings yet

- W4 Module 4 FINANCIAL RATIOS Part 2BDocument12 pagesW4 Module 4 FINANCIAL RATIOS Part 2BDanica VetuzNo ratings yet

- FabmDocument18 pagesFabmYangyang Leslie100% (1)

- Lesson 1 Statement of Financial PositionDocument22 pagesLesson 1 Statement of Financial PositionMylene SantiagoNo ratings yet

- Sales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitDocument5 pagesSales 140, 800 Less: Cost of Sales (84, 480) Gross ProfitMichaela KowalskiNo ratings yet

- Accounting For Public Sector and Civil Society 2022 LatestDocument170 pagesAccounting For Public Sector and Civil Society 2022 LatestZerai Hagos HailemariamNo ratings yet

- Worksheet 5 Q2 TaxationDocument15 pagesWorksheet 5 Q2 TaxationJennifer FabiaNo ratings yet

- IAS 19 SummaryDocument6 pagesIAS 19 SummaryMuchaa VlogNo ratings yet

- Accounting and Its Environment - PowerPoint PresentationDocument30 pagesAccounting and Its Environment - PowerPoint PresentationBhea G. ManaloNo ratings yet

- VRTS 112-Activity Number 1Document1 pageVRTS 112-Activity Number 1Gina PrancelisoNo ratings yet

- Completing the Accounting CycleDocument4 pagesCompleting the Accounting CycleJeva, Marrian Jane NoolNo ratings yet

- Partnership and Corporation Part 1Document60 pagesPartnership and Corporation Part 1Jeraldine DejanNo ratings yet

- Unit I and 2Document6 pagesUnit I and 2harlene_luNo ratings yet

- Business Finance-Semi-Final ExamDocument3 pagesBusiness Finance-Semi-Final ExamHLeigh Nietes-Gabutan100% (1)

- Basic Documents and Transactions Related To Bank DepositsDocument18 pagesBasic Documents and Transactions Related To Bank DepositsDiana Fernandez MagnoNo ratings yet

- Analysis of Financial Statements Mix RatioDocument30 pagesAnalysis of Financial Statements Mix RatioBianca Angela Camayra QuiaNo ratings yet

- Accounting SystemDocument84 pagesAccounting Systemkhatib mtumweniNo ratings yet

- Journalizing, Posting and Trial BalanceDocument19 pagesJournalizing, Posting and Trial BalanceDanica del RosarioNo ratings yet

- Introduction To Accounting & Financial Statements: MN 3042 - Business Economics and Financial Accounting Offered byDocument31 pagesIntroduction To Accounting & Financial Statements: MN 3042 - Business Economics and Financial Accounting Offered byAwishka ThuduwageNo ratings yet

- CSE August 2020Document15 pagesCSE August 2020tNo ratings yet

- Proof of Cash or Four Column ReconciliationDocument6 pagesProof of Cash or Four Column ReconciliationMico Villegas BalbuenaNo ratings yet

- Rizal LiberalismDocument2 pagesRizal LiberalismMico Villegas BalbuenaNo ratings yet

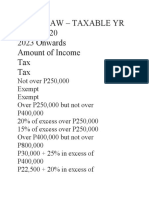

- Train Law - Taxable Yr 2018 - 2020 2023 Onwards Amount of Income Tax TaxDocument5 pagesTrain Law - Taxable Yr 2018 - 2020 2023 Onwards Amount of Income Tax TaxMico Villegas BalbuenaNo ratings yet

- Local Media2303227450598506287Document18 pagesLocal Media2303227450598506287Mico Villegas BalbuenaNo ratings yet

- Tie Breaker QuizDocument3 pagesTie Breaker QuizMico Villegas BalbuenaNo ratings yet

- 6 CS Form 100 Revised September 2016 PDFDocument2 pages6 CS Form 100 Revised September 2016 PDFNiel Edar Balleza100% (2)

- Nws Radiosonde and Uvm Cricketsonde ComparisonDocument1 pageNws Radiosonde and Uvm Cricketsonde ComparisonMico Villegas BalbuenaNo ratings yet

- Radiosonde SDocument14 pagesRadiosonde SMico Villegas BalbuenaNo ratings yet

- Consumer Protection Digests and Case Studies-Volume II (07122015)Document202 pagesConsumer Protection Digests and Case Studies-Volume II (07122015)Mico Villegas BalbuenaNo ratings yet

- Consumer Protection Digests and Case Studies-Volume II (07122015)Document202 pagesConsumer Protection Digests and Case Studies-Volume II (07122015)Mico Villegas BalbuenaNo ratings yet

- Consultants DirectoryDocument36 pagesConsultants DirectoryAnonymous yjLUF9gDTSNo ratings yet

- UPT Unit 8 Vers ADocument12 pagesUPT Unit 8 Vers AValeria GarciaNo ratings yet

- Younis 2020Document5 pagesYounis 2020nalakathshamil8No ratings yet

- Balcony AnalysysDocument4 pagesBalcony AnalysysKory EstesNo ratings yet

- The King's Avatar - A Compilatio - Butterfly BlueDocument8,647 pagesThe King's Avatar - A Compilatio - Butterfly BlueDarka gamesNo ratings yet

- Much NeedeDocument11 pagesMuch NeedeRijul KarkiNo ratings yet

- The Role of Molecular Testing in The Differential Diagnosis of Salivary Gland CarcinomasDocument17 pagesThe Role of Molecular Testing in The Differential Diagnosis of Salivary Gland CarcinomasMariela Judith UCNo ratings yet

- HQ 170aDocument82 pagesHQ 170aTony WellsNo ratings yet

- Floor MatsDocument3 pagesFloor MatsGhayas JawedNo ratings yet

- California Evaluation Procedures For New Aftermarket Catalytic ConvertersDocument27 pagesCalifornia Evaluation Procedures For New Aftermarket Catalytic Convertersferio252No ratings yet

- ) (Significant Digits Are Bounded To 1 Due To 500m. However I Will Use 2SD To Make More Sense of The Answers)Document4 pages) (Significant Digits Are Bounded To 1 Due To 500m. However I Will Use 2SD To Make More Sense of The Answers)JeevikaGoyalNo ratings yet

- FEA Finite Element Analysis Tutorial ProblemsDocument16 pagesFEA Finite Element Analysis Tutorial ProblemsVinceTanNo ratings yet

- Wiz107sr User Manual en v1.0Document29 pagesWiz107sr User Manual en v1.0Pauli Correa ArriagadaNo ratings yet

- Manual SOC2 DVR Mini 90nDocument83 pagesManual SOC2 DVR Mini 90nDeybby Luna Laredo0% (1)

- Improved Line Maze Solving Algorithm For PDFDocument2 pagesImproved Line Maze Solving Algorithm For PDFRaja Joko MusridhoNo ratings yet

- Due Diligence InvestmentsDocument6 pagesDue Diligence InvestmentselinzolaNo ratings yet

- Equipment Sheet: Cable Laying VesselDocument2 pagesEquipment Sheet: Cable Laying Vesselsitu brestNo ratings yet

- Full download book Neurology Neonatology Questions And Controversies Neonatology Questions Controversies Pdf pdfDocument41 pagesFull download book Neurology Neonatology Questions And Controversies Neonatology Questions Controversies Pdf pdfzelma.lansberry528100% (12)

- Elementos ElectrónicosDocument9 pagesElementos ElectrónicosKratt DeividNo ratings yet

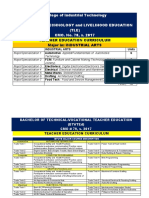

- College of Industrial Technology Bachelor of Technology and Livelihood Education (TLE) CMO. No. 78, S. 2017Document5 pagesCollege of Industrial Technology Bachelor of Technology and Livelihood Education (TLE) CMO. No. 78, S. 2017Industrial TechnologyNo ratings yet

- Missing Number Series Questions Specially For Sbi Po PrelimsDocument18 pagesMissing Number Series Questions Specially For Sbi Po PrelimsKriti SinghaniaNo ratings yet

- SDA HLD Template v1.3Document49 pagesSDA HLD Template v1.3Samuel TesfayeNo ratings yet

- Analysis and Design of BeamsDocument12 pagesAnalysis and Design of BeamsHasanain AlmusawiNo ratings yet