You might also like

- Category Management Cycle & Checklist: Gateway Review: Stop, Think, CheckDocument9 pagesCategory Management Cycle & Checklist: Gateway Review: Stop, Think, CheckStipe SinkoNo ratings yet

- Fabm2 Sce Week 6-8Document61 pagesFabm2 Sce Week 6-8mary rose aragonNo ratings yet

- Chapter 10 Types and Forms of Organizational ChangeDocument22 pagesChapter 10 Types and Forms of Organizational ChangeTurki Jarallah75% (4)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument13 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionMarielle Mae BurbosNo ratings yet

- BUS 1.3 - Financial Awareness - Level 4 AssignmentDocument9 pagesBUS 1.3 - Financial Awareness - Level 4 AssignmentDave PulpulaanNo ratings yet

- Chapter 1Document15 pagesChapter 1Rhodessa CotengNo ratings yet

- Fabm Ii - Bank ReconciliationDocument41 pagesFabm Ii - Bank ReconciliationAvril OlivarezNo ratings yet

- BSAIS 304 SyllabusDocument3 pagesBSAIS 304 SyllabusAdrian Perolino DelosoNo ratings yet

- Special and CombinationDocument8 pagesSpecial and CombinationDanica Shane EscobidalNo ratings yet

- Chapter 6 Accounting Concepts and PrinciplesDocument39 pagesChapter 6 Accounting Concepts and PrinciplesCharlyn galahanNo ratings yet

- BSBMKG433 Project PortfolioDocument10 pagesBSBMKG433 Project PortfolioFrancis Dave Peralta BitongNo ratings yet

- Accounting Equation: LessonDocument14 pagesAccounting Equation: LessonJdkrkejNo ratings yet

- Service Bus - Acctg CycleDocument34 pagesService Bus - Acctg CycleJenniferNo ratings yet

- Business Ethics and Social Responsibility ABM A Answersheet SummativeDocument5 pagesBusiness Ethics and Social Responsibility ABM A Answersheet SummativeCyra Joy Francisco100% (1)

- Fundamentals AnswerDocument12 pagesFundamentals AnswerRienalyn Dumlao Duldulao-DaligconNo ratings yet

- Demo Lesson 2021-NancyDocument22 pagesDemo Lesson 2021-NancyNancy AtentarNo ratings yet

- ABM - FABM11-IIIg - J - 28Document2 pagesABM - FABM11-IIIg - J - 28Mary Grace Pagalan Ladaran0% (1)

- Accounts Notes For BCA - IncompleteDocument56 pagesAccounts Notes For BCA - IncompleteSahil Kumar Gupta100% (1)

- Accounting1 Midterm Exam 1st Sem Ay2017-18Document13 pagesAccounting1 Midterm Exam 1st Sem Ay2017-18Uy SamuelNo ratings yet

- Entrepreneurship LAS 5 Q4 Week 5 6Document10 pagesEntrepreneurship LAS 5 Q4 Week 5 6Desiree Jane SaleraNo ratings yet

- Tos in FABM2 Second QuarterDocument2 pagesTos in FABM2 Second QuarterLAARNI REBONGNo ratings yet

- Fabm1 Summative ExamDocument8 pagesFabm1 Summative ExamAbegail PanangNo ratings yet

- Fabm2 q2 m3 Bank Reconciliation EditedDocument29 pagesFabm2 q2 m3 Bank Reconciliation EditedMaria anjilu VillanuevaNo ratings yet

- DL101 Module4 Trademarks PDFDocument43 pagesDL101 Module4 Trademarks PDFAbhishek ShahNo ratings yet

- Merchandising BusinessDocument31 pagesMerchandising BusinessAngelo ReyesNo ratings yet

- q4 Abm Fundamentals of Abm1 11 Week 3Document6 pagesq4 Abm Fundamentals of Abm1 11 Week 3Judy Ann Villanueva100% (1)

- Shs Abm: Accounting EquationDocument4 pagesShs Abm: Accounting EquationJellyNo ratings yet

- Topic 14 - Income and Business TaxationDocument71 pagesTopic 14 - Income and Business TaxationFrancez Anne Guanzon100% (1)

- Basic Acctg CH1Document76 pagesBasic Acctg CH1Danica Medina0% (1)

- Senior High School Department: Quarter 3 - Module 8: Merchandising Concern (Part 1)Document9 pagesSenior High School Department: Quarter 3 - Module 8: Merchandising Concern (Part 1)Jaye RuantoNo ratings yet

- LP in ABMDocument4 pagesLP in ABMGLICER MANGARON100% (1)

- Unit II Lesson 5 and 6 ADJUSTING ENTRIES and FSDocument25 pagesUnit II Lesson 5 and 6 ADJUSTING ENTRIES and FSAlezandra SantelicesNo ratings yet

- LESSON 10 Business TransactionsDocument8 pagesLESSON 10 Business TransactionsUnamadable UnleomarableNo ratings yet

- 6 Posting To The LedgerDocument3 pages6 Posting To The Ledgerapi-299265916No ratings yet

- Fundamentals of Abm 1: First QuarterDocument8 pagesFundamentals of Abm 1: First QuarterIvan NuescaNo ratings yet

- Fabm 2: Quarter 3 - Module 2 Statement of Comprehensive Income For Service & Merchandising BusinessDocument23 pagesFabm 2: Quarter 3 - Module 2 Statement of Comprehensive Income For Service & Merchandising BusinessMaria Nikka GarciaNo ratings yet

- 04 PRE-TEST OR POST-TEST Jeremy OrtegaDocument14 pages04 PRE-TEST OR POST-TEST Jeremy OrtegaJeremy OrtegaNo ratings yet

- Prefinal Exam Set B (Fabm1)Document4 pagesPrefinal Exam Set B (Fabm1)Zybel RosalesNo ratings yet

- Fabm 1 Quiz TheoriesDocument4 pagesFabm 1 Quiz TheoriesJanafaye Krisha100% (1)

- Day1 10daysaccountingchallengeDocument16 pagesDay1 10daysaccountingchallengeSeungyun ChoNo ratings yet

- Las Q4 Fabm 1 GagalacDocument26 pagesLas Q4 Fabm 1 GagalacAira Venice GuyadaNo ratings yet

- Chapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Document37 pagesChapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Ian SumastreNo ratings yet

- FAR Prelim For Printing PDFDocument86 pagesFAR Prelim For Printing PDFMico Villegas BalbuenaNo ratings yet

- QUIZ - FS - SolutionDocument3 pagesQUIZ - FS - SolutionRichelle ManocayNo ratings yet

- FABM2 - q2 - Clas2 Preparation of Bank Reconciliation Statement - v3Document14 pagesFABM2 - q2 - Clas2 Preparation of Bank Reconciliation Statement - v3Joey AgnasNo ratings yet

- FABM1 Lesson8-1 Five Major Accounts-LIABILITIESDocument13 pagesFABM1 Lesson8-1 Five Major Accounts-LIABILITIESWalter MataNo ratings yet

- aCCOUNTING cONCEPTS AND pRINCIPLESDocument4 pagesaCCOUNTING cONCEPTS AND pRINCIPLESMarjealyn PortugalNo ratings yet

- National Accounting Quiz Bee Showdown (NAQDOWN) 2012Document10 pagesNational Accounting Quiz Bee Showdown (NAQDOWN) 2012nfjpia30secgenNo ratings yet

- Accounting Concepts and PrinciplesDocument26 pagesAccounting Concepts and PrinciplesWindelyn Iligan100% (2)

- 01 FabmDocument32 pages01 FabmMavs MadriagaNo ratings yet

- SIC InterpretationsDocument42 pagesSIC InterpretationsJean Fajardo Badillo100% (1)

- Bank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaDocument18 pagesBank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaPSHNo ratings yet

- FAR 2 NotesDocument3 pagesFAR 2 NotesMARK RANIEL ANTAZONo ratings yet

- Module 1 - Applied EconomicsDocument20 pagesModule 1 - Applied EconomicsJoan Llido100% (2)

- 8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Document7 pages8011 Topper 21 101 503 550 10598 Basic Accounting Terms Up201904301415 1556613905 1714Madhu SNo ratings yet

- Adjustments Are Journalized and Posted: Completing The Accounting CycleDocument4 pagesAdjustments Are Journalized and Posted: Completing The Accounting CycleJeva, Marrian Jane NoolNo ratings yet

- Analysis of Financial Statements Mix RatioDocument30 pagesAnalysis of Financial Statements Mix RatioBianca Angela Camayra QuiaNo ratings yet

- 04 Trade Accounts ReceivableDocument7 pages04 Trade Accounts Receivablesharielles /No ratings yet

- FABM2 Module - 1Document3 pagesFABM2 Module - 1Jennifer NayveNo ratings yet

- Public Finance NotesDocument12 pagesPublic Finance NotesshivaniNo ratings yet

- Accounting For Merchandising Business (Report)Document37 pagesAccounting For Merchandising Business (Report)Garet Julia Marie T.100% (1)

- Buss 203 Business FinanceDocument2 pagesBuss 203 Business FinanceTevin67% (3)

- Business Finance Handouts 04Document5 pagesBusiness Finance Handouts 04Shane VeiraNo ratings yet

- Steps in The Accounting Cycle of A Service Business (Posting and Preparing Trial Balance)Document15 pagesSteps in The Accounting Cycle of A Service Business (Posting and Preparing Trial Balance)Zybel RosalesNo ratings yet

- Intel College: Course Name: Business Finance and EconomicsDocument2 pagesIntel College: Course Name: Business Finance and EconomicsRocky Kaur100% (1)

- Adjusting EntriesDocument27 pagesAdjusting EntriesquintosjeryNo ratings yet

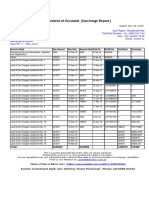

- Surcharge Report BTKSC-P05164Document1 pageSurcharge Report BTKSC-P05164Nasir Badshah AfridiNo ratings yet

- 1 NHAI RFP Website Development..Document80 pages1 NHAI RFP Website Development..happysomi23No ratings yet

- Equivalency Handbook 2019 (Higher Education)Document248 pagesEquivalency Handbook 2019 (Higher Education)Po PenguinNo ratings yet

- Globalization As Economic ProcessDocument3 pagesGlobalization As Economic ProcessmaryaniNo ratings yet

- Organization Structure: Sunaina AhujaDocument22 pagesOrganization Structure: Sunaina AhujaVarun PatniNo ratings yet

- Us Digital Gambling Halftime Report August 2023Document34 pagesUs Digital Gambling Halftime Report August 2023Antonius VincentNo ratings yet

- Kshitij Negi Semester 4 (Csit)Document10 pagesKshitij Negi Semester 4 (Csit)Kshitij NegiNo ratings yet

- Research Notes and Commentaries Doing Well by Doing Good-Case Study: Fair & Lovely' Whitening CreamDocument7 pagesResearch Notes and Commentaries Doing Well by Doing Good-Case Study: Fair & Lovely' Whitening CreamMuqadas JavedNo ratings yet

- Factory Ledger and General Ledger-1Document9 pagesFactory Ledger and General Ledger-1gull skNo ratings yet

- PAT Presentation Nagpur AirportDocument42 pagesPAT Presentation Nagpur AirportHimanshu BhattNo ratings yet

- Week 2 Solutions - Not Covered in LectureDocument1 pageWeek 2 Solutions - Not Covered in LectureJames BogeNo ratings yet

- Dfccil Questions On Railway English 44Document33 pagesDfccil Questions On Railway English 44op nNo ratings yet

- Johannes Sianturi: Personal DetailsDocument3 pagesJohannes Sianturi: Personal DetailsGreen Sustain EnergyNo ratings yet

- SM. Marketing PlanDocument5 pagesSM. Marketing PlanAnita SubhawariaNo ratings yet

- Assignment Acc2543 Session 2 - 2022Document8 pagesAssignment Acc2543 Session 2 - 2022afiq hisyamNo ratings yet

- Market StructureDocument15 pagesMarket StructureLyka UrmaNo ratings yet

- Allianz Thematica RTIDocument2 pagesAllianz Thematica RTIEng Hau QuaNo ratings yet

- Micro Economics 1-7Document82 pagesMicro Economics 1-7Tino AlappatNo ratings yet

- Supply Contract Jafar Ag: 1. The Subject of The AgreementDocument10 pagesSupply Contract Jafar Ag: 1. The Subject of The AgreementJafar AGNo ratings yet

- Test 2 - Global Supply Networks Bruno Silvestre: InstructionsDocument6 pagesTest 2 - Global Supply Networks Bruno Silvestre: InstructionsDuc AnhNo ratings yet

- Rubenlicera Com 7272 Top Filipino TechnopreneursDocument30 pagesRubenlicera Com 7272 Top Filipino TechnopreneursJacques LumangNo ratings yet

- A Consultancy Project On Master Tiles & Ceramic Industries LTD SUBMITTED TO: Sir Salman Khan MangolDocument68 pagesA Consultancy Project On Master Tiles & Ceramic Industries LTD SUBMITTED TO: Sir Salman Khan MangolSalman ShoukatNo ratings yet

- Math 12-ABM BESR-Q2-Week-4Document19 pagesMath 12-ABM BESR-Q2-Week-4Jomar BenedicoNo ratings yet

- Why Are Some Growth Poles More Successful Than OthersDocument4 pagesWhy Are Some Growth Poles More Successful Than OthersMarie POUSSEREAUNo ratings yet