You might also like

- Pet Care in PeruDocument16 pagesPet Care in Perurominaysabel100% (1)

- Sauces, Dressings and Condiments in PeruDocument12 pagesSauces, Dressings and Condiments in Perujoaquin salernoNo ratings yet

- Dog Food Cookbook: 41 Healthy and Easy Recipes for Your Best FriendFrom EverandDog Food Cookbook: 41 Healthy and Easy Recipes for Your Best FriendRating: 5 out of 5 stars5/5 (1)

- Processed Fruit and Vegetables in PeruDocument9 pagesProcessed Fruit and Vegetables in PeruMiguel DaneriNo ratings yet

- Laundry Care in PeruDocument12 pagesLaundry Care in PeruDanitza Villazana Gómez0% (1)

- Concentrates in PeruDocument9 pagesConcentrates in PeruMiguel DaneriNo ratings yet

- Coffee in Peru: Euromonitor International December 2019Document10 pagesCoffee in Peru: Euromonitor International December 2019Dennis Marwin Pereyra DiazNo ratings yet

- Sports Nutrition in PeruDocument14 pagesSports Nutrition in PeruMiguel Daneri100% (1)

- Consumer Lifestyles in PeruDocument60 pagesConsumer Lifestyles in PerurominaysabelNo ratings yet

- Food-Report Statistics PDFDocument162 pagesFood-Report Statistics PDFТатьяна КасимоваNo ratings yet

- Suntory: Rebranding The Japanese Whisky HighballDocument9 pagesSuntory: Rebranding The Japanese Whisky HighballNicola ZucchettiNo ratings yet

- Marketing Decision Making (MKDM) : New Product Demand Forecasting Session 4Document30 pagesMarketing Decision Making (MKDM) : New Product Demand Forecasting Session 4kanishka sharmaNo ratings yet

- Estrategia Telefónica de ArgentinaDocument77 pagesEstrategia Telefónica de ArgentinaAndres PaolantonioNo ratings yet

- Assignment Nestle Refrigerated Foods Case Analysis Muhzeen NDocument9 pagesAssignment Nestle Refrigerated Foods Case Analysis Muhzeen NkonerukrishnakantNo ratings yet

- Volume Forecast For New ProductsDocument35 pagesVolume Forecast For New ProductsPreyanshu SainiNo ratings yet

- Spirits in PeruDocument16 pagesSpirits in PeruMiguel DaneriNo ratings yet

- Beauty & Personal Care in Latin America: Category ReviewDocument62 pagesBeauty & Personal Care in Latin America: Category ReviewGlory MendozaNo ratings yet

- Sanitary Protection in Peru AnalysisDocument2 pagesSanitary Protection in Peru AnalysisDayan ChemelloNo ratings yet

- A Framework For Managing The Innovation ProcessDocument13 pagesA Framework For Managing The Innovation ProcessEDUARDO SEBRIANO100% (2)

- Bottled Water in PeruDocument8 pagesBottled Water in PeruMiguel DaneriNo ratings yet

- Ingeniería Industrial: Creación de Empresa Dedicada A La Fabricación Y Comercialización de Comida Natural para PerrosDocument59 pagesIngeniería Industrial: Creación de Empresa Dedicada A La Fabricación Y Comercialización de Comida Natural para PerrosAlber E. Duque100% (2)

- Innocent Drinks (Smoothie)Document31 pagesInnocent Drinks (Smoothie)Swapnil RajebhosaleNo ratings yet

- DTL EWeek2017c08 Euromonitor enDocument31 pagesDTL EWeek2017c08 Euromonitor enVidhiNo ratings yet

- Sweet Biscuits, Snack Bars and Fruit Snacks in MexicoDocument16 pagesSweet Biscuits, Snack Bars and Fruit Snacks in MexicoReynerio VilledaNo ratings yet

- Dirección de Marketing Philip Kotler y Kevin Lane Keller PDFDocument498 pagesDirección de Marketing Philip Kotler y Kevin Lane Keller PDFJose100% (2)

- B2B Market Attractiveness Evaluation How To Size Opportunities and Reduce RiskDocument21 pagesB2B Market Attractiveness Evaluation How To Size Opportunities and Reduce RiskpsyxicatNo ratings yet

- Corporate Finance by Ivo WelchDocument28 pagesCorporate Finance by Ivo WelchLê AnhNo ratings yet

- S&B - Kombucha Market - Global Forecast To 2020Document25 pagesS&B - Kombucha Market - Global Forecast To 2020anomenusNo ratings yet

- Caso Zara Traduccion y RespuestasDocument8 pagesCaso Zara Traduccion y RespuestasbryanNo ratings yet

- Anu CaseDocument4 pagesAnu CaseAnu DeepNo ratings yet

- Plantilla Matriz BCGDocument3 pagesPlantilla Matriz BCGjamessNo ratings yet

- EMIS Insights - Colombia Consumer Goods and Retail 2020 - 2021Document73 pagesEMIS Insights - Colombia Consumer Goods and Retail 2020 - 2021Jimmy MirandaNo ratings yet

- Innovation at WhirlpoolDocument18 pagesInnovation at Whirlpoolsugapriya38No ratings yet

- Business Model Design Case Study - Nespresso May 2018Document12 pagesBusiness Model Design Case Study - Nespresso May 2018cyborg0121No ratings yet

- Case Questions - Chabros InternationalDocument1 pageCase Questions - Chabros Internationalsyedasana001No ratings yet

- Gatorade - Client BriefDocument2 pagesGatorade - Client BriefMarie-Caroline CHAPIRONNo ratings yet

- Truearth Healthy Foods: Marketing Management - IiDocument4 pagesTruearth Healthy Foods: Marketing Management - IivinodNo ratings yet

- FutureBrand - Country Index - 2020Document83 pagesFutureBrand - Country Index - 2020TS MediaNo ratings yet

- Case 2 Innocent LTD: Being Good Is Good For Business: A Classic Case in Point Was The Body Shop Chain ofDocument3 pagesCase 2 Innocent LTD: Being Good Is Good For Business: A Classic Case in Point Was The Body Shop Chain ofAndres GrossoNo ratings yet

- Kraft Case RbeersDocument4 pagesKraft Case Rbeersapi-490755452No ratings yet

- Beer in PeruDocument12 pagesBeer in PeruAlmendra ChavezNo ratings yet

- Red Bull Precess of Globalization in EuropeDocument3 pagesRed Bull Precess of Globalization in EuropeSilviu Popa100% (1)

- Montreaux Chocolate USA Spreadsheet T3 21Document7 pagesMontreaux Chocolate USA Spreadsheet T3 21Kriti GoenkaNo ratings yet

- Latin America Ecommerce 2020 EMarketerDocument23 pagesLatin America Ecommerce 2020 EMarketerDaniel 1o Perfil pessoal Gerenciador das BMSNo ratings yet

- Marketing 5.0Document20 pagesMarketing 5.0Coral AnthuanetNo ratings yet

- Sample Case BriefDocument4 pagesSample Case Briefacoustic7850% (2)

- Virgin Media's - Diversification StrategyDocument6 pagesVirgin Media's - Diversification StrategyRachita SinghNo ratings yet

- Maru Case - ExcelPage2Document39 pagesMaru Case - ExcelPage2Md.Imteyazuddin GhouseNo ratings yet

- Generaciones Perú. Todas para Una y Cada Una Con Lo SuyoDocument35 pagesGeneraciones Perú. Todas para Una y Cada Una Con Lo SuyoKaren ChavezNo ratings yet

- Comparision of Patanjali and HulDocument5 pagesComparision of Patanjali and HulAtri Asati100% (1)

- Pet Care in India - BriefingDocument17 pagesPet Care in India - BriefingDeepak Dahiya100% (1)

- Cat Food in Colombia 2017Document12 pagesCat Food in Colombia 2017Jose Angel IrachetaNo ratings yet

- Dog Food in Colombia 2017Document13 pagesDog Food in Colombia 2017Jose Angel IrachetaNo ratings yet

- Pet Care in India Briefing PDFDocument17 pagesPet Care in India Briefing PDFguptarahul1992No ratings yet

- Pet Products in The PhilippinesDocument8 pagesPet Products in The PhilippinesrieNo ratings yet

- Pet Care in Colombia 2017Document17 pagesPet Care in Colombia 2017Jose Angel IrachetaNo ratings yet

- Ready - Meals - in - Peru 2019Document9 pagesReady - Meals - in - Peru 2019Dennis Marwin Pereyra DiazNo ratings yet

- Pet Products in Colombia: Euromonitor International May 2020Document8 pagesPet Products in Colombia: Euromonitor International May 2020sofia rodriguezNo ratings yet

- Target Shots I-UnlockedDocument257 pagesTarget Shots I-Unlockedsaumya ranjan nayakNo ratings yet

- MG8591 Principles of Management 2,13 MARKS Converted 1Document90 pagesMG8591 Principles of Management 2,13 MARKS Converted 14723 Nilamani M100% (1)

- Unit V Human Resource Planning in Nepal:-Demographic Trend AnalysisDocument5 pagesUnit V Human Resource Planning in Nepal:-Demographic Trend AnalysisSujan ChaudharyNo ratings yet

- Tenant Verification Form PDFDocument2 pagesTenant Verification Form PDFmohit kumarNo ratings yet

- Case Study-Design Thinking in IBMDocument50 pagesCase Study-Design Thinking in IBMSANYA KAPOORNo ratings yet

- Kaizen: A Lean Manufacturing Tool For Continuous ImprovementDocument24 pagesKaizen: A Lean Manufacturing Tool For Continuous ImprovementSamrudhi PetkarNo ratings yet

- Digital Transformation OF FMCG Supply Chain: Case Presentation (Nitie, Mumbai)Document10 pagesDigital Transformation OF FMCG Supply Chain: Case Presentation (Nitie, Mumbai)snehaarpiNo ratings yet

- Topic 1 The Corporation and StakeholdersDocument3 pagesTopic 1 The Corporation and StakeholdersAprilNo ratings yet

- Listening Test Unit 6Document2 pagesListening Test Unit 6Xuân Bách0% (1)

- Top 10 Warehouse ManagementDocument48 pagesTop 10 Warehouse ManagementmmarizNo ratings yet

- GiftDocument6 pagesGiftalive2flirtNo ratings yet

- Project Cycle Management Report (AEPAM Pub.288)Document64 pagesProject Cycle Management Report (AEPAM Pub.288)Waqar AhmadNo ratings yet

- While It Is True That Increases in Efficiency Generate Productivity IncreasesDocument3 pagesWhile It Is True That Increases in Efficiency Generate Productivity Increasesgod of thunder ThorNo ratings yet

- Lum Chang Technical BrochureDocument68 pagesLum Chang Technical BrochureBatu GajahNo ratings yet

- Personal Lease Adam LightfootDocument9 pagesPersonal Lease Adam Lightfootaaakinkumi115No ratings yet

- Gender Pay Gap - HSBCDocument17 pagesGender Pay Gap - HSBCruksana khatoonNo ratings yet

- Labor Costs in Manufacturing IndustriesDocument18 pagesLabor Costs in Manufacturing Industriesminhduc2010No ratings yet

- Webank'S Supply Chain Finance Solution: Confidential & ProprietaryDocument15 pagesWebank'S Supply Chain Finance Solution: Confidential & ProprietaryimuesNo ratings yet

- MAA763 Governance and Fraud: Revision T2 2017Document40 pagesMAA763 Governance and Fraud: Revision T2 2017MalikNo ratings yet

- IE 317 Case Study 4: Bsie Ii Group 7Document37 pagesIE 317 Case Study 4: Bsie Ii Group 7Chel Armenton100% (1)

- Fighting Food Waste Using The Circular Economy ReportDocument40 pagesFighting Food Waste Using The Circular Economy ReportCaroline Velenthio AmansyahNo ratings yet

- Jntuh r19 Mba SyllabusDocument54 pagesJntuh r19 Mba SyllabusK MaheshNo ratings yet

- Jakawali ParachuteDocument1 pageJakawali Parachuteparasailing jakartaNo ratings yet

- Al-Baraka Islamic Bank Internship ReportDocument69 pagesAl-Baraka Islamic Bank Internship Reportbbaahmad89100% (8)

- Slip Gaji (3)Document2 pagesSlip Gaji (3)Olele Olala50% (2)

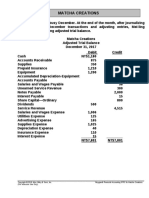

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- Shift Report: Availability Performance Rate Quality Products RateDocument6 pagesShift Report: Availability Performance Rate Quality Products RatehwhhadiNo ratings yet

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- f1 Kaplan Kit CompressDocument236 pagesf1 Kaplan Kit CompressRomaan AliNo ratings yet

- Causes of Low Literacy Rate in PakistanDocument27 pagesCauses of Low Literacy Rate in PakistanSaba Naeem82% (17)

- Roxane Gay & Everand Originals Presents: Good Girl: Notes on Dog RescueFrom EverandRoxane Gay & Everand Originals Presents: Good Girl: Notes on Dog RescueRating: 5 out of 5 stars5/5 (3)

- The Other End of the Leash: Why We Do What We Do Around DogsFrom EverandThe Other End of the Leash: Why We Do What We Do Around DogsRating: 5 out of 5 stars5/5 (65)

- The Dog Listener: Learn How to Communicate with Your Dog for Willing CooperationFrom EverandThe Dog Listener: Learn How to Communicate with Your Dog for Willing CooperationRating: 4 out of 5 stars4/5 (37)

- Roxane Gay & Everand Originals Presents: Good Girl: Notes on Dog RescueFrom EverandRoxane Gay & Everand Originals Presents: Good Girl: Notes on Dog RescueRating: 4.5 out of 5 stars4.5/5 (22)

- Merle's Door: Lessons from a Freethinking DogFrom EverandMerle's Door: Lessons from a Freethinking DogRating: 4 out of 5 stars4/5 (326)

- Puppy Training 101: How to Train a Puppy, Training Your Own Psychiatric Service Dog, A Step-By-Step Program so your Pup Will Understand You!From EverandPuppy Training 101: How to Train a Puppy, Training Your Own Psychiatric Service Dog, A Step-By-Step Program so your Pup Will Understand You!Rating: 5 out of 5 stars5/5 (85)

- Inside of a Dog: What Dogs See, Smell, and KnowFrom EverandInside of a Dog: What Dogs See, Smell, and KnowRating: 4 out of 5 stars4/5 (390)

- Show Dog: The Charmed Life and Trying Times of a Near-Perfect PurebredFrom EverandShow Dog: The Charmed Life and Trying Times of a Near-Perfect PurebredRating: 3.5 out of 5 stars3.5/5 (13)

- Come Back, Como: Winning the Heart of a Reluctant DogFrom EverandCome Back, Como: Winning the Heart of a Reluctant DogRating: 3.5 out of 5 stars3.5/5 (10)

- Dogland: Passion, Glory, and Lots of Slobber at the Westminster Dog ShowFrom EverandDogland: Passion, Glory, and Lots of Slobber at the Westminster Dog ShowNo ratings yet

- The Dog Who Couldn't Stop Loving: How Dogs Have Captured Our Hearts for Thousands of YearsFrom EverandThe Dog Who Couldn't Stop Loving: How Dogs Have Captured Our Hearts for Thousands of YearsNo ratings yet

- Your Dog Is Your Mirror: The Emotional Capacity of Our Dogs and OurselvesFrom EverandYour Dog Is Your Mirror: The Emotional Capacity of Our Dogs and OurselvesRating: 4 out of 5 stars4/5 (31)

- Meet Your Dog: The Game-Changing Guide to Understanding Your Dog's BehaviorFrom EverandMeet Your Dog: The Game-Changing Guide to Understanding Your Dog's BehaviorRating: 5 out of 5 stars5/5 (1)

- Edward's Menagerie: Dogs: 50 canine crochet patternsFrom EverandEdward's Menagerie: Dogs: 50 canine crochet patternsRating: 3 out of 5 stars3/5 (5)

- Arthur: The Dog Who Crossed the Jungle to Find a HomeFrom EverandArthur: The Dog Who Crossed the Jungle to Find a HomeRating: 4.5 out of 5 stars4.5/5 (19)

- The Wrong Dog: An Unlikely Tale of Unconditional LoveFrom EverandThe Wrong Dog: An Unlikely Tale of Unconditional LoveRating: 4.5 out of 5 stars4.5/5 (26)

- MINE!: A PRACTICAL GUIDE TO RESOURCE GUARDING IN DOGSFrom EverandMINE!: A PRACTICAL GUIDE TO RESOURCE GUARDING IN DOGSRating: 4 out of 5 stars4/5 (15)

- How To Speak Dog: Mastering the Art of Dog-Human CommunicationFrom EverandHow To Speak Dog: Mastering the Art of Dog-Human CommunicationRating: 4 out of 5 stars4/5 (66)

- The Art of Training Your Dog: How to Gently Teach Good Behavior Using an E-CollarFrom EverandThe Art of Training Your Dog: How to Gently Teach Good Behavior Using an E-CollarRating: 5 out of 5 stars5/5 (2)

- Arthur: The Dog who Crossed the Jungle to Find a HomeFrom EverandArthur: The Dog who Crossed the Jungle to Find a HomeRating: 4.5 out of 5 stars4.5/5 (16)

- Meet Your Dog: The Game-Changing Guide to Understanding Your Dog's BehaviorFrom EverandMeet Your Dog: The Game-Changing Guide to Understanding Your Dog's BehaviorRating: 5 out of 5 stars5/5 (34)

- Show Dog: The Charmed Life and Trying Times of a Near-Perfect PurebredFrom EverandShow Dog: The Charmed Life and Trying Times of a Near-Perfect PurebredNo ratings yet

- Talking to Animals: How You Can Understand Animals and They Can Understand YouFrom EverandTalking to Animals: How You Can Understand Animals and They Can Understand YouRating: 4.5 out of 5 stars4.5/5 (18)

- The Complete Guide to Pit Bulls: Finding, Raising, Feeding, Training, Exercising, Grooming, and Loving your new Pit Bull DogFrom EverandThe Complete Guide to Pit Bulls: Finding, Raising, Feeding, Training, Exercising, Grooming, and Loving your new Pit Bull DogRating: 3.5 out of 5 stars3.5/5 (4)

- For the Love of a Dog: Understanding Emotion in You and Your Best FriendFrom EverandFor the Love of a Dog: Understanding Emotion in You and Your Best FriendRating: 4 out of 5 stars4/5 (100)