You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Internal Analysis On McdonaldsDocument4 pagesInternal Analysis On McdonaldsMahmuda Umm OmarNo ratings yet

- FrankfurtersDocument38 pagesFrankfurtersAnamaria Blaga Petrean50% (2)

- Snapshot Pack - Alcholic BeveragesDocument7 pagesSnapshot Pack - Alcholic BeveragesAmit RajNo ratings yet

- Comprehensive Pack - Auto PDFDocument104 pagesComprehensive Pack - Auto PDFAmit RajNo ratings yet

- Snapshot Pack - Solar EnergyDocument5 pagesSnapshot Pack - Solar EnergyAmit RajNo ratings yet

- Power Pack - Solar EnergyDocument36 pagesPower Pack - Solar EnergyAmit RajNo ratings yet

- Comprehensive Pack - Solar EnergyDocument73 pagesComprehensive Pack - Solar EnergyAmit RajNo ratings yet

- Snapshot Pack - FMCGDocument9 pagesSnapshot Pack - FMCGAmit RajNo ratings yet

- Power Pack - FMCGDocument41 pagesPower Pack - FMCGAmit RajNo ratings yet

- Comprehensive Pack - Cold ChainDocument90 pagesComprehensive Pack - Cold ChainAmit RajNo ratings yet

- Power Pack - E-CommerceDocument33 pagesPower Pack - E-CommerceAmit RajNo ratings yet

- Snapshot Pack - E-CommerceDocument9 pagesSnapshot Pack - E-CommerceAmit RajNo ratings yet

- Power Pack - CementDocument38 pagesPower Pack - CementAmit RajNo ratings yet

- Comprehensive Pack - TelecomDocument64 pagesComprehensive Pack - TelecomAmit RajNo ratings yet

- Ann Taylor FinalDocument14 pagesAnn Taylor FinalPrince AroraNo ratings yet

- Gardenia ProcessDocument2 pagesGardenia ProcessJhun Michael LocusNo ratings yet

- Report EsDocument53 pagesReport Espankaj44dahimaNo ratings yet

- Materials GPQ PDFDocument20 pagesMaterials GPQ PDFAmirul IslamNo ratings yet

- 5S Powerpoint For MeetingDocument85 pages5S Powerpoint For MeetingJoan BandojoNo ratings yet

- Bosch Machine ManualDocument40 pagesBosch Machine ManualDarshitDadhaniyaNo ratings yet

- Final RMG Term Paper00Document18 pagesFinal RMG Term Paper00haddiness100% (1)

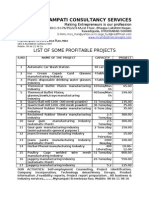

- List-Mynampati Consultancy ServicesDocument8 pagesList-Mynampati Consultancy Servicesmcs_msr302350% (2)

- 7 Stages of Quality Control Checks For Meat and PoultryDocument2 pages7 Stages of Quality Control Checks For Meat and PoultrysureshNo ratings yet

- Group 10 - ABC Case Study Corelio PrintingDocument10 pagesGroup 10 - ABC Case Study Corelio Printingmuhammad ifwatNo ratings yet

- Poly Bag Costing For Apparel MerchandisingDocument2 pagesPoly Bag Costing For Apparel MerchandisingerabbiNo ratings yet

- The Dairy Industry Act: RegulationDocument17 pagesThe Dairy Industry Act: RegulationelinzolaNo ratings yet

- Typs of Fabric LossDocument2 pagesTyps of Fabric LossarunkadveNo ratings yet

- Profile of BSEDocument45 pagesProfile of BSEprabhu_jay23No ratings yet

- IMSE3106 Course DescriptionDocument8 pagesIMSE3106 Course DescriptionChristal Chuk100% (1)

- A Study of The Total Quality Management at Amul: Ruchira PrasadDocument3 pagesA Study of The Total Quality Management at Amul: Ruchira PrasadAnmol AhujaNo ratings yet

- PR 465-Phthalic Anhydride - ProspectusDocument8 pagesPR 465-Phthalic Anhydride - ProspectusHuu LinhNo ratings yet

- White Oil NewDocument4 pagesWhite Oil NewVaradrajan jothiNo ratings yet

- GDCS Bandlock2 LiteratureDocument2 pagesGDCS Bandlock2 LiteratureFilipNo ratings yet

- Kapda Fashion Company Profile - KFDocument7 pagesKapda Fashion Company Profile - KFsnmulikNo ratings yet

- 07 Social Science Civics Key Notes Ch09 A Shirt in The MarketDocument1 page07 Social Science Civics Key Notes Ch09 A Shirt in The Marketsmruti sangitaNo ratings yet

- Final Report On MilkfoodDocument55 pagesFinal Report On Milkfoodneeti_bhalla1990100% (1)

- Soda Solvay Dense For Export: Soda Ash / Sodium CarbonateDocument2 pagesSoda Solvay Dense For Export: Soda Ash / Sodium CarbonateRizkyNo ratings yet

- Fashion OrientationDocument28 pagesFashion OrientationkeerthiNo ratings yet

- Apjmr-2017 5 1 15 PDFDocument11 pagesApjmr-2017 5 1 15 PDFAira SoriaNo ratings yet

- MEZAN MASHHOOD (Repaired)Document18 pagesMEZAN MASHHOOD (Repaired)Mashhood AliNo ratings yet

- Menu PlanningDocument5 pagesMenu PlanningLee Ann HerreraNo ratings yet

- Britannia Annual Report 2016-17 PDFDocument232 pagesBritannia Annual Report 2016-17 PDFAditya ramaiahNo ratings yet