You might also like

- Daftar Type Dan Harga Mesin Printer Laser BrotherDocument2 pagesDaftar Type Dan Harga Mesin Printer Laser BrotherEKO HERI SUSANTONo ratings yet

- PGP 387 Divesh Paper ManufacturingDocument3 pagesPGP 387 Divesh Paper ManufacturingdiveshNo ratings yet

- FCR Prima t2 Brochure 01 PDFDocument2 pagesFCR Prima t2 Brochure 01 PDFshoaibNo ratings yet

- InFocus PRG Datasheet en 18MAY17Document4 pagesInFocus PRG Datasheet en 18MAY17Wiwin LatifahNo ratings yet

- Pro-Rsp SeriesDocument2 pagesPro-Rsp SeriesSiddharth rohillaNo ratings yet

- Insumos y Kit Mantenimiento en ToshibaDocument11 pagesInsumos y Kit Mantenimiento en ToshibaLourdes Anquise VelardeNo ratings yet

- 17 SeriesDocument1 page17 SeriesHi fiveNo ratings yet

- BSD+Product+Line Card+2017Document2 pagesBSD+Product+Line Card+2017Eduardo VillafañeNo ratings yet

- Multifunction Color Laser Devices: XC2132 XC4140 XC4150 XC6152 XC8160 XC9235 XC9245Document2 pagesMultifunction Color Laser Devices: XC2132 XC4140 XC4150 XC6152 XC8160 XC9235 XC9245Eduardo VillafañeNo ratings yet

- The Most Comprehensive Product Offering For Remanufactured Brother CartridgesDocument10 pagesThe Most Comprehensive Product Offering For Remanufactured Brother CartridgesIcs AsomNo ratings yet

- 2.1.2.2 Print Engine: Product Spec and FeatureDocument1 page2.1.2.2 Print Engine: Product Spec and FeatureAnton LuiggiNo ratings yet

- Q Drive Cut SheetDocument4 pagesQ Drive Cut SheetSatria GoNo ratings yet

- T2 - TutorialDocument8 pagesT2 - TutorialkeertanworksNo ratings yet

- Data Analysis Sample ProblemDocument2 pagesData Analysis Sample Problem510617055 MayankkumarNo ratings yet

- Apex435: Side Address Cardioid CondenserDocument1 pageApex435: Side Address Cardioid CondenserManu ZidNo ratings yet

- 2024 - FBS300 - Launch Pack - Q2 - Standard Costing, LC, LP - SolutionDocument4 pages2024 - FBS300 - Launch Pack - Q2 - Standard Costing, LC, LP - SolutionyankhoNo ratings yet

- Book 1Document1 pageBook 1SukainaNo ratings yet

- Digital Representation of Audio InformationDocument22 pagesDigital Representation of Audio InformationYuaris ArhamNo ratings yet

- InkDocument2 pagesInkghani ibnuNo ratings yet

- 4-Distributed Arithmetic SDDocument13 pages4-Distributed Arithmetic SDinturi venkata gopichandNo ratings yet

- Dell I3, 3040Document1 pageDell I3, 3040Shanto N ShanNo ratings yet

- Printer Line-Up 2001-2002: ML-4500 ML-4600 ML-1210 ML-1220M ML-1250 ML-1650 ML-7300NDocument1 pagePrinter Line-Up 2001-2002: ML-4500 ML-4600 ML-1210 ML-1220M ML-1250 ML-1650 ML-7300Nblackcat657No ratings yet

- DP-301U Printer Compatibility ListDocument4 pagesDP-301U Printer Compatibility ListAndry RAQANo ratings yet

- Technical Services Costing SheetDocument2 pagesTechnical Services Costing SheetyusrieNo ratings yet

- Printer Service Reference GuideDocument132 pagesPrinter Service Reference GuideDean StaceyNo ratings yet

- PC (Personal Computer) Harga Sewa Per HariDocument1 pagePC (Personal Computer) Harga Sewa Per HariBAYU KHARISMANo ratings yet

- Parsia CanonDocument5 pagesParsia CanonCopier ServicesNo ratings yet

- Template CBA KostDocument16 pagesTemplate CBA Kostandy kusumahNo ratings yet

- Bulk Trial Seatex On Ratna DewiDocument6 pagesBulk Trial Seatex On Ratna DewiEvanKusumaNo ratings yet

- Digital Black and White Multifunction Device: Major Specifications of 4000/ 3000Document2 pagesDigital Black and White Multifunction Device: Major Specifications of 4000/ 3000Dollar MulyadiNo ratings yet

- Global Pulley Specification - QFDocument1 pageGlobal Pulley Specification - QFrrobles011No ratings yet

- How Self-Training Cures Computerphobia: Special ReportDocument414 pagesHow Self-Training Cures Computerphobia: Special ReportMartin ChipilukNo ratings yet

- Narqg 01CDocument1 pageNarqg 01CdjokanomcaNo ratings yet

- Encod Ca500 en PDocument52 pagesEncod Ca500 en PTiago OliveiraNo ratings yet

- Epson SureLab SL-D830Document2 pagesEpson SureLab SL-D830arshvirsingh3956No ratings yet

- RS Series Full SpecificationsDocument2 pagesRS Series Full Specificationsinayat kusumaNo ratings yet

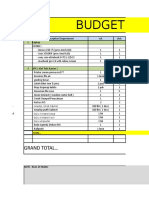

- BUDGET Properti: Grand TotalDocument4 pagesBUDGET Properti: Grand TotalAudrey FazrinNo ratings yet

- CatTrap Before and AfterDocument1 pageCatTrap Before and AfterrafaelNo ratings yet

- El.005.instalasi Sound System MusdalifahDocument1 pageEl.005.instalasi Sound System Musdalifahcahaya satujiwaNo ratings yet

- CRON Catalog Another Day Another DreamDocument20 pagesCRON Catalog Another Day Another Dreamy9dww6km7yNo ratings yet

- HAR Eps3000 HandlingInstructionDocument2 pagesHAR Eps3000 HandlingInstructionjeivison joséNo ratings yet

- Voltage Controlled Oscillator: FeaturesDocument1 pageVoltage Controlled Oscillator: Featuresafz 23BlrNo ratings yet

- Stampaci Color PoredjenjeDocument2 pagesStampaci Color PoredjenjeАрту ДитуNo ratings yet

- Air Distribution 101 Titus 1 PDFDocument324 pagesAir Distribution 101 Titus 1 PDFMohamed Aboobucker Mohamed IrfanNo ratings yet

- Toner Low Empty Control Perseus WSDocument8 pagesToner Low Empty Control Perseus WSYến PhạmNo ratings yet

- DM45 SOS (SpecOptSuppl)Document23 pagesDM45 SOS (SpecOptSuppl)IvayloNo ratings yet

- Booklist 3 To 8 2024-25 Agarwal BooksellersDocument2 pagesBooklist 3 To 8 2024-25 Agarwal BooksellersEntertainment VediosNo ratings yet

- Pcworld199unse PDFDocument218 pagesPcworld199unse PDF51hundredNo ratings yet

- FUJIFILM FCR CAPSULA XL Specifications: Fuji Computed RadiographyDocument3 pagesFUJIFILM FCR CAPSULA XL Specifications: Fuji Computed Radiographydony prabuNo ratings yet

- s910 SpecsDocument3 pagess910 SpecsFOROWNo ratings yet

- Boschert: CNC Busbar Cutting - Punching - Bending SolutionDocument42 pagesBoschert: CNC Busbar Cutting - Punching - Bending SolutiondemdiinNo ratings yet

- Graphic DesignDocument9 pagesGraphic Designcharity wangeciNo ratings yet

- Photo Continental PricelistDocument6 pagesPhoto Continental PricelistdenymdanNo ratings yet

- Curso de Control de Solidos de EntrenamientoDocument26 pagesCurso de Control de Solidos de EntrenamientoJavier RiosNo ratings yet

- Lexmark Color c522n DatasheetDocument2 pagesLexmark Color c522n DatasheetkswongNo ratings yet

- Fujifilm FCR Prima T2 Brochure With Logo Ver. Dec. 2017Document2 pagesFujifilm FCR Prima T2 Brochure With Logo Ver. Dec. 2017luilorna27No ratings yet

- Sadist CostingDocument2 pagesSadist CostingTaha AliNo ratings yet

- Key Performance Indicators: Unnamed ProjectDocument5 pagesKey Performance Indicators: Unnamed ProjectHenry Lambis MirandaNo ratings yet

- Gandhi Cloth Company - Integer & Mixed Integer ProgrammingDocument3 pagesGandhi Cloth Company - Integer & Mixed Integer ProgrammingChristina JunevaNo ratings yet

- W667 Job Completion CertificateDocument5 pagesW667 Job Completion CertificateMohamed ShafeeqNo ratings yet

- 7 Golden Rules of Mobile Testing TemplateDocument36 pages7 Golden Rules of Mobile Testing Templatestarvit2No ratings yet

- Fully Automated Luxury CommunismDocument8 pagesFully Automated Luxury CommunismNicoleta MeruțiuNo ratings yet

- Siklus RankineDocument26 pagesSiklus RankineArialdi Almonda0% (1)

- CO2 System ManualDocument11 pagesCO2 System Manualthugsdei100% (1)

- Ticketswap-Betonhofi-Slaybania-Ticket-20808722 2Document1 pageTicketswap-Betonhofi-Slaybania-Ticket-20808722 2Anderlik-Makkai GergelyNo ratings yet

- Guidance On Shipboard Towing and Mooring EquipmentDocument11 pagesGuidance On Shipboard Towing and Mooring EquipmentNuman Kooliyat IsmethNo ratings yet

- Mica PDFDocument2 pagesMica PDFomarNo ratings yet

- 5400 Replace BBU BlockDocument15 pages5400 Replace BBU BlockAhmed HaggarNo ratings yet

- Operation & Maintenance Manual d260 S3a-En Okt. 2014Document166 pagesOperation & Maintenance Manual d260 S3a-En Okt. 2014DrBollapu Sudarshan50% (2)

- Vale International Pellet Plant PDFDocument2 pagesVale International Pellet Plant PDFSrinivasanNo ratings yet

- Dahua ITC302-RU1A1Document2 pagesDahua ITC302-RU1A1Dms TsNo ratings yet

- Hardware Compatibility List (HCL) For Veritas Storage Foundation (TM) and High Availability Solutions 4.1 MP2 For SolarisDocument5 pagesHardware Compatibility List (HCL) For Veritas Storage Foundation (TM) and High Availability Solutions 4.1 MP2 For SolarisbennialNo ratings yet

- Saniaccess Pump Product SheetDocument1 pageSaniaccess Pump Product SheetArun UdayabhanuNo ratings yet

- Seagoing Tug "Mhan Aung-3": Ministry of TransportDocument2 pagesSeagoing Tug "Mhan Aung-3": Ministry of TransportnyaungzinNo ratings yet

- Stm32 Mcu FamilyDocument12 pagesStm32 Mcu FamilyriverajluizNo ratings yet

- 85001-0636 - Portable Loudspeaker SystemDocument2 pages85001-0636 - Portable Loudspeaker SystemmohammadNo ratings yet

- Spray Nozzle Flow Rate CalculatorDocument10 pagesSpray Nozzle Flow Rate CalculatorRavindra VasudevaNo ratings yet

- K2000-Serie ENDocument1 pageK2000-Serie ENbala subramaniyam TSNo ratings yet

- Perform Cover Hole DrillingDocument12 pagesPerform Cover Hole Drillingjulianusginting00No ratings yet

- Proses Bisnis Otomotif: Zummayroh, S.PDDocument26 pagesProses Bisnis Otomotif: Zummayroh, S.PDHannyka FebrianoNo ratings yet

- SEO For Growth: The Ultimate Guide For Marketers, Web Designers & EntrepreneursDocument7 pagesSEO For Growth: The Ultimate Guide For Marketers, Web Designers & EntrepreneursJoyce M LaurenNo ratings yet

- CBBEDocument23 pagesCBBECharuJagwaniNo ratings yet

- Saudi Electricity Company - Southern Region (Saudi Arabia)Document7 pagesSaudi Electricity Company - Southern Region (Saudi Arabia)azeemmet9924No ratings yet

- R H R C H E C R: Egenerating The Uman Ight TOA Lean and Ealthy Nvironment in The Ommons EnaissanceDocument229 pagesR H R C H E C R: Egenerating The Uman Ight TOA Lean and Ealthy Nvironment in The Ommons Enaissanceapi-250991215No ratings yet

- Chemical EarthingDocument18 pagesChemical EarthingDivay ChadhaNo ratings yet

- DC 850 X12 5010 I01 Purchase OrderDocument40 pagesDC 850 X12 5010 I01 Purchase OrderGeervani SowduriNo ratings yet

- Automatic Street Light ControllerDocument23 pagesAutomatic Street Light ControllerAnjali Sharma100% (2)

- What Is A Surge TankDocument13 pagesWhat Is A Surge TankAnikateNo ratings yet

- Lesson Plan MathsDocument3 pagesLesson Plan MathsRuthira Nair AB KrishenanNo ratings yet