You might also like

- On "Credit Facility by HDFC Bank" Towards Partial Fulfilment of Integrated Master of Business Administration (IMBA)Document106 pagesOn "Credit Facility by HDFC Bank" Towards Partial Fulfilment of Integrated Master of Business Administration (IMBA)Richa SachanNo ratings yet

- Pricing DecisionsDocument15 pagesPricing DecisionsHosahalli Narayana Murthy PrasannaNo ratings yet

- Performance Evaluation of PNB and HDFC BankDocument58 pagesPerformance Evaluation of PNB and HDFC BankEkam Jot100% (1)

- INTERNSHIP REPORT ON 15 DAYS INTERNSHIP PROGRAM AT SUMIT CEPLDocument25 pagesINTERNSHIP REPORT ON 15 DAYS INTERNSHIP PROGRAM AT SUMIT CEPLNarendra Singh100% (1)

- 11 Master Data Management Roadmap TemplateDocument20 pages11 Master Data Management Roadmap TemplateMARIA SELES TELES SOUSANo ratings yet

- Project SbiDocument103 pagesProject SbiShree Cyberia50% (2)

- Comparative Analysis of Corporate Salary Accounts With Respect To HDFC BankDocument65 pagesComparative Analysis of Corporate Salary Accounts With Respect To HDFC BankRavi Kokkar100% (1)

- Bank Credit Management Project ReportDocument49 pagesBank Credit Management Project ReportAnonymous nTOjIYeW50% (2)

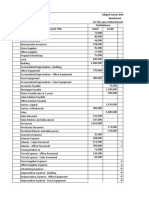

- Abigail Santos Boutique, Financial Statement For MerchandisingDocument9 pagesAbigail Santos Boutique, Financial Statement For MerchandisingFeiya Liu100% (1)

- Micro FinanceDocument69 pagesMicro FinanceDIgitalNo ratings yet

- Analysis HDFC BANKDocument83 pagesAnalysis HDFC BANKsilent readersNo ratings yet

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- A Study of Credit Assessment in Dena BankDocument48 pagesA Study of Credit Assessment in Dena BankDeepali MahilagiriNo ratings yet

- Odoo Inventory Management FeaturesDocument5 pagesOdoo Inventory Management FeaturesyudiNo ratings yet

- Cash ManagementDocument82 pagesCash ManagementAjiLalNo ratings yet

- Financial Services Offered by BankDocument52 pagesFinancial Services Offered by BankIshan Vyas100% (2)

- Retail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To StudentDocument51 pagesRetail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To Studentganeshkhale7052No ratings yet

- CMS Report 1Document101 pagesCMS Report 1Kamal PurohitNo ratings yet

- Kotak Mahindra Project NewDocument105 pagesKotak Mahindra Project NewPrgya SinghNo ratings yet

- WORKING CAPITAL OF AXIS BANKDocument84 pagesWORKING CAPITAL OF AXIS BANKSami Zama100% (2)

- Analysis of NPAs in Public and Private BanksDocument56 pagesAnalysis of NPAs in Public and Private BanksKhalid HussainNo ratings yet

- Comparative Analysis of The Products and Servies of Axis BankDocument29 pagesComparative Analysis of The Products and Servies of Axis Bankpavan100% (1)

- Blackbook FinalDocument70 pagesBlackbook FinalHunney MasandNo ratings yet

- A Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksDocument12 pagesA Comparative Study of Home Loan Schemes of Private Sector Banks Public Sector BanksKapil KumarNo ratings yet

- Project Cash Management in Banks ProjectDocument45 pagesProject Cash Management in Banks Projectkedar dhuriNo ratings yet

- BY: - Minaz Khan Sakina Kapadia Sandeep Arora Shailja SinghDocument18 pagesBY: - Minaz Khan Sakina Kapadia Sandeep Arora Shailja SinghSandiip AroraNo ratings yet

- Working Capital ManagementDocument78 pagesWorking Capital ManagementDrj Maz50% (2)

- A Study On Loans and Advances by Rohit RDocument91 pagesA Study On Loans and Advances by Rohit RChandrashekhar GurnuleNo ratings yet

- HDFC Bank Financial AnalysisDocument48 pagesHDFC Bank Financial AnalysisAbhinandan Bose50% (10)

- Understanding Home LoansDocument72 pagesUnderstanding Home LoansshaileshNo ratings yet

- Financial Products in Kotak Mahiindra Bank and Its CompetitorsDocument93 pagesFinancial Products in Kotak Mahiindra Bank and Its CompetitorsShobhit GoswamiNo ratings yet

- Project Report On Banking SystemDocument16 pagesProject Report On Banking SystemArun Kumar0% (1)

- Project Report ON: "Saving and Current Account"Document63 pagesProject Report ON: "Saving and Current Account"nitrosey100% (3)

- SBI Non Performing AssetsDocument43 pagesSBI Non Performing AssetsVikram RokadeNo ratings yet

- Consumer Awareness On Credit CardsDocument11 pagesConsumer Awareness On Credit Cardskartik palavalasaNo ratings yet

- Cash Flow For Study29072021Document60 pagesCash Flow For Study29072021URANo ratings yet

- Innovation in Banking SectorDocument21 pagesInnovation in Banking Sectoruma2k10No ratings yet

- Project On HDFC BankDocument67 pagesProject On HDFC BankAarti YadavNo ratings yet

- Banking System at HDFC BankDocument83 pagesBanking System at HDFC BankSuresh Verma100% (1)

- HDFC ProfileDocument10 pagesHDFC ProfilePunitha AradhyaNo ratings yet

- Blackbook Retail PDFDocument87 pagesBlackbook Retail PDFurmila ghoshNo ratings yet

- Study of Cash Management at ICICI BankDocument84 pagesStudy of Cash Management at ICICI BankRini Nigam100% (1)

- Understanding Financial Management ConceptsDocument90 pagesUnderstanding Financial Management ConceptsVamsi SakhamuriNo ratings yet

- Financial Performance of HDFC BankDocument51 pagesFinancial Performance of HDFC Bankabhasa50% (6)

- Report On HDFC BANK NewDocument19 pagesReport On HDFC BANK NewakashNo ratings yet

- Comparative Study of Home Loans of PNB and Sbi Bank Final ProjectDocument11 pagesComparative Study of Home Loans of PNB and Sbi Bank Final ProjectManish KumarNo ratings yet

- Brief History of Canara BankDocument35 pagesBrief History of Canara BankSambathkumar Madanagopal0% (1)

- Introduction To Financial Services MarketingDocument14 pagesIntroduction To Financial Services MarketingJitender Kaushal100% (1)

- Summer Internship Report - HDFC Digital BankingDocument32 pagesSummer Internship Report - HDFC Digital BankingMantosh SinghNo ratings yet

- Finance Project On Various Credit Schemes of SBIDocument46 pagesFinance Project On Various Credit Schemes of SBItaanvi00783% (6)

- DHFL Sip ReportDocument50 pagesDHFL Sip ReportPragatiNo ratings yet

- AXIS BANK'S MARKETING STRATEGIES AND CHINA EXPANSIONDocument58 pagesAXIS BANK'S MARKETING STRATEGIES AND CHINA EXPANSION2kd TermanitoNo ratings yet

- Loans & Advances Study at Ujjivan BankDocument75 pagesLoans & Advances Study at Ujjivan Banksachin mohanNo ratings yet

- Ratio Analysis in HDFC BankDocument82 pagesRatio Analysis in HDFC BankTanvir KhanNo ratings yet

- A Study of Credit Cards in Indian ScenarioDocument11 pagesA Study of Credit Cards in Indian ScenarioWifi Internet Cafe & Multi ServicesNo ratings yet

- Digital Marketing in Banking SectorDocument35 pagesDigital Marketing in Banking SectorSteven Pruitt100% (2)

- Impact of Fraud On The Indian Baking Sector.Document43 pagesImpact of Fraud On The Indian Baking Sector.Hani patelNo ratings yet

- Project On Cash ManagementDocument67 pagesProject On Cash ManagementShreya HadimaniNo ratings yet

- Isl Engineerng College: Master of Business AdministrationDocument17 pagesIsl Engineerng College: Master of Business Administrationammukhan khanNo ratings yet

- Understanding Cash Management in SBIDocument72 pagesUnderstanding Cash Management in SBIRasika chobeNo ratings yet

- R. Ramya Reddy - 058Document10 pagesR. Ramya Reddy - 058ammukhan khanNo ratings yet

- E00a1-Cash Management - IciciDocument64 pagesE00a1-Cash Management - IciciwebstdsnrNo ratings yet

- Final Assingment of WCMDocument21 pagesFinal Assingment of WCMswapnil swadhinataNo ratings yet

- Peos CertificateDocument1 pagePeos CertificateBruce Alain CodiamatNo ratings yet

- Simulation Probs UploadedDocument3 pagesSimulation Probs UploadedSiddarthanSrtNo ratings yet

- CH 35Document5 pagesCH 35Vishal GoyalNo ratings yet

- Tranfer PricingDocument36 pagesTranfer PricingSrikrishna DharNo ratings yet

- Partnership Dissolution: QuizDocument5 pagesPartnership Dissolution: QuizLee SuarezNo ratings yet

- 8 Common Business Plan Mistakes PDFDocument4 pages8 Common Business Plan Mistakes PDFNelPermatoNo ratings yet

- S Residence Painting WorksDocument4 pagesS Residence Painting WorksRON JAYSON ARCIAGANo ratings yet

- Jenil Desai ResumeDocument1 pageJenil Desai ResumeSujay TorviNo ratings yet

- 145 Ijmperdfeb2018145Document10 pages145 Ijmperdfeb2018145TJPRC PublicationsNo ratings yet

- DeVry ACCT 505 Final Exam 2Document12 pagesDeVry ACCT 505 Final Exam 2devryfinalexamscomNo ratings yet

- Hascol Internship Report To Be SubmittedDocument5 pagesHascol Internship Report To Be SubmittedNazir AnsariNo ratings yet

- Summary On StarbucksDocument3 pagesSummary On StarbucksSaleem BhattiNo ratings yet

- Bab03 Memanage Dalam Lingkungan GlobalDocument38 pagesBab03 Memanage Dalam Lingkungan GlobalPerbasi SidoarjoNo ratings yet

- Group C ActivityDocument3 pagesGroup C ActivityGerard Andrei B. DeinlaNo ratings yet

- Assignment PDFDocument31 pagesAssignment PDFKhanNo ratings yet

- Reading 48-Portfolio Management An OverviewDocument24 pagesReading 48-Portfolio Management An OverviewAllen AravindanNo ratings yet

- الموقف البريطاني من الحرب الأهلية الأمريكية 1861 - 1865Document61 pagesالموقف البريطاني من الحرب الأهلية الأمريكية 1861 - 1865Marah RafeaNo ratings yet

- Situation:: BDE Percentage EarningDocument2 pagesSituation:: BDE Percentage Earninganon_508740366No ratings yet

- Availability As of December 1, 2020: Classification Phase LOT Area List Price Exclusive of Vat & Oc Allocation StatusDocument7 pagesAvailability As of December 1, 2020: Classification Phase LOT Area List Price Exclusive of Vat & Oc Allocation StatusMia NungaNo ratings yet

- Payslip:: Petrofac International LTDDocument1 pagePayslip:: Petrofac International LTDRakesh PatelNo ratings yet

- 11 Activity 2 OMDocument1 page11 Activity 2 OMBea Catherine Laguitao0% (1)

- Chapter Four International Marketing Product PolicyDocument53 pagesChapter Four International Marketing Product PolicyEyob ZekariyasNo ratings yet

- An IRS Audit Is A ReviewDocument4 pagesAn IRS Audit Is A ReviewRohit BajpaiNo ratings yet

- Department of Agrarian Reform: "Gil" de Los ReyesDocument10 pagesDepartment of Agrarian Reform: "Gil" de Los ReyesGNCDWNo ratings yet

- Griffin Sas KB 6.1Document10 pagesGriffin Sas KB 6.1Tk KimNo ratings yet