You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Capital BudgetingDocument18 pagesCapital BudgetingNilesh SondigalaNo ratings yet

- Project Evaluation Techniques and Capital Budgeting MethodsDocument16 pagesProject Evaluation Techniques and Capital Budgeting MethodsRabinNo ratings yet

- Appraisal Criteria - Capital BudgetingDocument50 pagesAppraisal Criteria - Capital BudgetingNitesh NagdevNo ratings yet

- Capital BudgetingDocument52 pagesCapital Budgetingrabitha07541No ratings yet

- PETROLEUM ECONOMIC INDICATORSDocument57 pagesPETROLEUM ECONOMIC INDICATORSAlex CoolNo ratings yet

- Capital Budgeting Decisions ExplainedDocument42 pagesCapital Budgeting Decisions ExplainedPiyush ChitlangiaNo ratings yet

- Capital Budgeting 2Document49 pagesCapital Budgeting 2Naman LadhaNo ratings yet

- Financial Management Case Study-2 The Investment DetectiveDocument9 pagesFinancial Management Case Study-2 The Investment DetectiveSushmita DikshitNo ratings yet

- Capital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsDocument39 pagesCapital Budgeting A Nice Finance Topic Helpful For Mba and Bba StudentsNimish KumarNo ratings yet

- CH 08 Capital BudgetingDocument51 pagesCH 08 Capital BudgetingLitika SachdevaNo ratings yet

- Practice Question For Capital Budgeting: Ans: NPV (P) Rs. 5381, NPV (Q) Rs. 3814Document3 pagesPractice Question For Capital Budgeting: Ans: NPV (P) Rs. 5381, NPV (Q) Rs. 3814Sumit Kumar SahooNo ratings yet

- WK 3 DQ 1Document4 pagesWK 3 DQ 1Bharat PanthiNo ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingRuchika AgarwalNo ratings yet

- DR - Naushad Alam: Capital BudgetingDocument38 pagesDR - Naushad Alam: Capital BudgetingUrvashi SinghNo ratings yet

- Main Project Capital Budgeting MbaDocument110 pagesMain Project Capital Budgeting Mbasushain koulNo ratings yet

- Business Finance Module 9Document13 pagesBusiness Finance Module 9Kanton FernandezNo ratings yet

- CH - 08 Cap BudgetingDocument54 pagesCH - 08 Cap BudgetingfoglaabhishekNo ratings yet

- Capital Budgeting - I: Gourav Vallabh Xlri JamshedpurDocument64 pagesCapital Budgeting - I: Gourav Vallabh Xlri JamshedpurSimran JainNo ratings yet

- Capital Rationing and Interpretation of IRR and NPV with Limited CapitalDocument7 pagesCapital Rationing and Interpretation of IRR and NPV with Limited CapitalKazi HasanNo ratings yet

- Choosing Innovation ProjectDocument25 pagesChoosing Innovation ProjectChrisha Jane LanutanNo ratings yet

- 202005021259597527vijayshankarpandey Capital Budgeting TechniquesDocument49 pages202005021259597527vijayshankarpandey Capital Budgeting TechniquesanishaNo ratings yet

- BF 14Document5 pagesBF 14zhairenaguila22No ratings yet

- 1cm8numoo 253914Document105 pages1cm8numoo 253914sagar sharmaNo ratings yet

- Unit 3: Capital Budgeting: Techniques & ImportanceDocument17 pagesUnit 3: Capital Budgeting: Techniques & ImportanceRahul kumarNo ratings yet

- IRR NPV and PBP PDFDocument13 pagesIRR NPV and PBP PDFyared haftuNo ratings yet

- YhjhtyfyhfghfhfhfjhgDocument25 pagesYhjhtyfyhfghfhfhfjhgbabylovelylovelyNo ratings yet

- Lesson 4: Investment AppraisalDocument56 pagesLesson 4: Investment AppraisalYi WeiNo ratings yet

- Wright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueDocument6 pagesWright Technological College of Antique Senior High School Sibalom Branch Sibalom, AntiqueLen PenieroNo ratings yet

- 2006111512164611635642060Document60 pages2006111512164611635642060Awsaf Amanat Khan AuzzieNo ratings yet

- Capital Budgeting DecisionsDocument44 pagesCapital Budgeting Decisionsarunadhana2004No ratings yet

- Capital Budgeting 2Document23 pagesCapital Budgeting 2Rohit Rajesh RathiNo ratings yet

- LAS 4 Quarter 4 BFDocument4 pagesLAS 4 Quarter 4 BFAnna Jessica NallaNo ratings yet

- CH 08 RevisedDocument51 pagesCH 08 RevisedBhakti MehtaNo ratings yet

- Investement AppraisalDocument19 pagesInvestement AppraisalUmah MeerNo ratings yet

- Capital Budgeting MethodsDocument13 pagesCapital Budgeting MethodsAmit SinghNo ratings yet

- Faculty: Ahamed Riaz: Capital Budgeting DecisionsDocument51 pagesFaculty: Ahamed Riaz: Capital Budgeting DecisionsShivani RajputNo ratings yet

- L-4 Project AppraisalDocument9 pagesL-4 Project Appraisalattitudefirstpankaj8625No ratings yet

- Project Appraisal MethodsDocument20 pagesProject Appraisal MethodsGayatri Sharma82% (22)

- Project Evaluation Techniques-NPVDocument18 pagesProject Evaluation Techniques-NPVSamar PratapNo ratings yet

- Capital Budgeting: Corporate Finance, Dr. Hemendra GuptaDocument42 pagesCapital Budgeting: Corporate Finance, Dr. Hemendra GuptaRiya PandeyNo ratings yet

- Investment Decision: Unit IiiDocument50 pagesInvestment Decision: Unit IiiFara HameedNo ratings yet

- Capital Budgeting: Long-Term Investment Decisions - The Key To Long Run Profitability and Success!Document21 pagesCapital Budgeting: Long-Term Investment Decisions - The Key To Long Run Profitability and Success!Mari BossNo ratings yet

- Unit 2 Capital Budgeting Technique ProblemsDocument39 pagesUnit 2 Capital Budgeting Technique ProblemsAshok KumarNo ratings yet

- CAPITAL BUDGETING TECHNIQUESDocument9 pagesCAPITAL BUDGETING TECHNIQUESRishia Diniella PorquiadoNo ratings yet

- PROJECT APPRAISAL METHODSDocument28 pagesPROJECT APPRAISAL METHODSMîñåk ŞhïïNo ratings yet

- Investment Evaluation Methods for Capital Budgeting DecisionsDocument10 pagesInvestment Evaluation Methods for Capital Budgeting DecisionsGosaye Desalegn100% (1)

- Capital Budgeting Decisions AnalyzedDocument56 pagesCapital Budgeting Decisions AnalyzedSurya SivakumarNo ratings yet

- FI3300 Corporate Finance: Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of FinanceDocument42 pagesFI3300 Corporate Finance: Spring Semester 2010 Dr. Isabel Tkatch Assistant Professor of Financemahmoud08070058No ratings yet

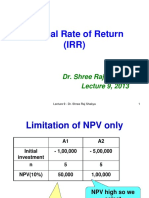

- Lecture9 IRRDocument29 pagesLecture9 IRRsuraj bhandariNo ratings yet

- 5, 6 & 7 Capital BudgetingDocument42 pages5, 6 & 7 Capital BudgetingNaman AgarwalNo ratings yet

- Measuring project performanceDocument3 pagesMeasuring project performancesanits591No ratings yet

- Unit-3 Capital Budgeting DecisionsDocument30 pagesUnit-3 Capital Budgeting DecisionsKrishna Chandran PallippuramNo ratings yet

- Project Appraisal TechniquesDocument31 pagesProject Appraisal TechniquesRajeevAgrawal86% (7)

- Capital BudgetingDocument37 pagesCapital Budgetingyashd99No ratings yet

- Cost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelFrom EverandCost Reduction Strategies for the Manufacturing Sector With Application of Microsoft ExcelNo ratings yet

- Effective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationFrom EverandEffective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationNo ratings yet

- Lecture7 Future Value MathodDocument23 pagesLecture7 Future Value Mathodsuraj bhandariNo ratings yet

- Lecture5 Cash Flow and Effective InterestDocument16 pagesLecture5 Cash Flow and Effective Interestsuraj bhandariNo ratings yet

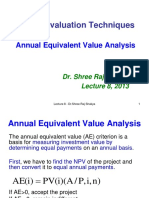

- Lecture8 Annual Equivalent MethodDocument21 pagesLecture8 Annual Equivalent Methodsuraj bhandariNo ratings yet

- Lecture9 IRRDocument29 pagesLecture9 IRRsuraj bhandariNo ratings yet

- Lecture5 Cash Flow and Effective InterestDocument16 pagesLecture5 Cash Flow and Effective Interestsuraj bhandariNo ratings yet

- Lecture4 Interest N CashflowDocument24 pagesLecture4 Interest N Cashflowsuraj bhandariNo ratings yet

- Kazi Abdur Rahman Rafi (56-D 3932)Document2 pagesKazi Abdur Rahman Rafi (56-D 3932)kazi A.R RafiNo ratings yet

- Income Taxation Ballada Solution Manual: Read/DownloadDocument2 pagesIncome Taxation Ballada Solution Manual: Read/Downloadcheche datingaling0% (1)

- General Manager Check List ChartDocument1 pageGeneral Manager Check List Chartmanishpandey1972100% (2)

- Sap Fi /co Course Content in Ecc6 To Ehp 5Document8 pagesSap Fi /co Course Content in Ecc6 To Ehp 5Mahesh JNo ratings yet

- Solutions To Problems: Pe On Estate TaxDocument11 pagesSolutions To Problems: Pe On Estate TaxErica NicolasuraNo ratings yet

- Bloomberg Default: Risk (DRSK)Document29 pagesBloomberg Default: Risk (DRSK)Dwitya Estu NurpramanaNo ratings yet

- Prime Finance First Mutrual Fund 31.12.19 - 2Document4 pagesPrime Finance First Mutrual Fund 31.12.19 - 2Abrar FaisalNo ratings yet

- W Wagner A Manufacturer Provided The Following Information For TheDocument1 pageW Wagner A Manufacturer Provided The Following Information For TheMiroslav GegoskiNo ratings yet

- Corporate Governance at Tata Sons Did They Walk The Talk CaseDocument12 pagesCorporate Governance at Tata Sons Did They Walk The Talk CaseAyush KapoorNo ratings yet

- Notice of The Sixteenth Annual General Meeting of Frieslandcampina Engro Pakistan LimitedDocument4 pagesNotice of The Sixteenth Annual General Meeting of Frieslandcampina Engro Pakistan Limitedfardasa123No ratings yet

- Module 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingDocument33 pagesModule 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingAlicia FelicianoNo ratings yet

- Midterm Exam Answer Sheet Course 8110Document8 pagesMidterm Exam Answer Sheet Course 8110kajalNo ratings yet

- Annual Report 2019 HighlightsDocument220 pagesAnnual Report 2019 HighlightsAnanda 17No ratings yet

- Empirical Chemicals LTD: Merseyside Project: Case StudyDocument20 pagesEmpirical Chemicals LTD: Merseyside Project: Case Study1b2m3100% (1)

- Materials Management in Hospitals - DR YC MahajanDocument167 pagesMaterials Management in Hospitals - DR YC MahajanizzykhalNo ratings yet

- Certificate of Creditable Tax Withheld at Source: Marfrancisco, Pinamalayan, Oriental MindoroDocument5 pagesCertificate of Creditable Tax Withheld at Source: Marfrancisco, Pinamalayan, Oriental MindoroChristcelda lozadaNo ratings yet

- NOTES TO FINANCIAL STATEMENTS OF PASIG CITYDocument37 pagesNOTES TO FINANCIAL STATEMENTS OF PASIG CITYKathleen Mae Amada - TorresNo ratings yet

- Account Paper MCQ PART 1 UpdateDocument67 pagesAccount Paper MCQ PART 1 Updateshivam kumarNo ratings yet

- General Questions: Pal SipDocument9 pagesGeneral Questions: Pal SipAura DewaNo ratings yet

- Question 686785 1Document11 pagesQuestion 686785 1rishu53840% (1)

- Precedent Transactions - TemplateDocument14 pagesPrecedent Transactions - TemplateStanley ChengNo ratings yet

- TDS Rates On The Income Tax of Bangladesh For 2019-20Document19 pagesTDS Rates On The Income Tax of Bangladesh For 2019-20Muhammad Asaduzzaman MonaNo ratings yet

- General Discussion of Balance Sheet: Accounting Principles AssetsDocument15 pagesGeneral Discussion of Balance Sheet: Accounting Principles AssetsNazmul Hossain RahatNo ratings yet

- Contingent Consideration Measurement PeriodDocument5 pagesContingent Consideration Measurement Periodjerald cerezaNo ratings yet

- Income Taxes (IAS 12)Document15 pagesIncome Taxes (IAS 12)Mahir RahmanNo ratings yet

- Jawaban Uas Pa 2 KasusDocument39 pagesJawaban Uas Pa 2 KasusSylviaNo ratings yet

- Formulae and Key Data: Number FormulaDocument3 pagesFormulae and Key Data: Number FormulaTrinh LinhNo ratings yet

- Detailed Analysis of Profit MarginDocument11 pagesDetailed Analysis of Profit MarginJeet SinghNo ratings yet

- Practical Accounting Problems IIDocument12 pagesPractical Accounting Problems IIRodNo ratings yet

- Mergers and Acquisitions (A Case Study On PVR and Cinemax) : Submitted byDocument40 pagesMergers and Acquisitions (A Case Study On PVR and Cinemax) : Submitted byVANSHIKA SHROFFNo ratings yet