You might also like

- Financial Modeling CMDocument3 pagesFinancial Modeling CMAreeba Aslam100% (1)

- Tgs Ar2020 Final WebDocument157 pagesTgs Ar2020 Final Webyasamin shajiratiNo ratings yet

- 2021Document12 pages2021Shalu PurswaniNo ratings yet

- Calculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Document1 pageCalculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Prachi NavghareNo ratings yet

- CF WACC, WC NewDocument5 pagesCF WACC, WC NewSanjana PottipallyNo ratings yet

- Financial Ratio Analysis Nestle India 2018: Akash Singh Niraj Abhijeet Pande Ramya EDocument14 pagesFinancial Ratio Analysis Nestle India 2018: Akash Singh Niraj Abhijeet Pande Ramya Eabhijeet pandeNo ratings yet

- Manpasand BeverDocument22 pagesManpasand BeverjenylshahNo ratings yet

- Britannia 1Document40 pagesBritannia 1Dipesh GuptaNo ratings yet

- Book 2Document4 pagesBook 2Aniket KolheNo ratings yet

- Markaz-GL On Financial ProjectionsDocument10 pagesMarkaz-GL On Financial ProjectionsSrikanth P School of Business and ManagementNo ratings yet

- Operating Lease Converter: InputsDocument44 pagesOperating Lease Converter: InputsJosé Manuel EstebanNo ratings yet

- Damodaran Excel - After Class - RegDocument2 pagesDamodaran Excel - After Class - RegAris KurniawanNo ratings yet

- Kim's Value Profit and Loss Account Notes Operating Capacity 1 2 3Document10 pagesKim's Value Profit and Loss Account Notes Operating Capacity 1 2 3sulthanhakimNo ratings yet

- TVS Motors Live Project Final 2Document39 pagesTVS Motors Live Project Final 2ritususmitakarNo ratings yet

- Profitability Analysis On Ultratech Cement: By, M.Praneeth Reddy 22397089Document19 pagesProfitability Analysis On Ultratech Cement: By, M.Praneeth Reddy 22397089PradeepNo ratings yet

- Company Financial Analysis and Ratio Comparison Over 5 YearsDocument6 pagesCompany Financial Analysis and Ratio Comparison Over 5 YearsAanchal MahajanNo ratings yet

- New Heritage Doll Capital Budgeting Case SolutionDocument5 pagesNew Heritage Doll Capital Budgeting Case SolutiontroyanxNo ratings yet

- Toyota Pakistan Ibf WordDocument20 pagesToyota Pakistan Ibf Wordifrahri123No ratings yet

- HW 2 - Ch03 P15 Build A Model - HrncarDocument2 pagesHW 2 - Ch03 P15 Build A Model - HrncarsusikralovaNo ratings yet

- Financial Performance of Interloop Limited (Ilp)Document2 pagesFinancial Performance of Interloop Limited (Ilp)Muhammad NadeemNo ratings yet

- Finance ProjectDocument9 pagesFinance ProjectMujtaba HassanNo ratings yet

- UltraTech Cements and Jaiprakash AssociatesDocument8 pagesUltraTech Cements and Jaiprakash AssociatesanushaNo ratings yet

- Bata India LTDDocument18 pagesBata India LTDAshish DupareNo ratings yet

- Infosys Ltd. Financial Analysis and ValuationDocument14 pagesInfosys Ltd. Financial Analysis and Valuationswaroop shettyNo ratings yet

- Financial Statement: Statement of Cash FlowsDocument6 pagesFinancial Statement: Statement of Cash FlowsdanyalNo ratings yet

- 100 BaggerDocument12 pages100 BaggerRishab WahalNo ratings yet

- Facts Given in The CaseDocument14 pagesFacts Given in The CaseYashasvi -No ratings yet

- Financial Model of Infosys: Revenue Ebitda Net IncomeDocument32 pagesFinancial Model of Infosys: Revenue Ebitda Net IncomePrabhdeep Dadyal100% (1)

- We Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)Document3 pagesWe Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)mayankNo ratings yet

- Key Competitors & Inditex Gap H&M Benetton Inditex Operating Results ( Millions)Document1 pageKey Competitors & Inditex Gap H&M Benetton Inditex Operating Results ( Millions)puneetdattaNo ratings yet

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocument6 pagesParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNo ratings yet

- New Heritage Doll Capital Budgeting Case SolutionDocument5 pagesNew Heritage Doll Capital Budgeting Case Solutionalka murarka50% (14)

- Group Activities g5 1Document281 pagesGroup Activities g5 12021-108960No ratings yet

- Glaxosmithkline Consumer Healthcare: Group MembersDocument19 pagesGlaxosmithkline Consumer Healthcare: Group MembersBilal AfzalNo ratings yet

- PRM Assignment 3Document18 pagesPRM Assignment 3ABDULNo ratings yet

- Financial Analysis Coles GroupDocument5 pagesFinancial Analysis Coles GroupAmmar HassanNo ratings yet

- Financial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)Document17 pagesFinancial (Rs Million) Mar-19 Mar-18 Mar-17 Mar-16 Mar-15 Y-O-Y Change (%) Y-O-Y Change (%)Berkshire Hathway coldNo ratings yet

- Hero Model - Equivalue 2Document48 pagesHero Model - Equivalue 2Neha RadiaNo ratings yet

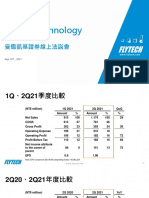

- Flytech TechnologyDocument7 pagesFlytech TechnologyLouis ChenNo ratings yet

- Financial PerformanceDocument16 pagesFinancial PerformanceADEEL SAITHNo ratings yet

- DCFTemplateDocument5 pagesDCFTemplateRob Keith100% (1)

- Restructuring at Neiman Marcus Group (A) Bankruptcy ValuationDocument66 pagesRestructuring at Neiman Marcus Group (A) Bankruptcy ValuationShaikh Saifullah KhalidNo ratings yet

- Berger 1Document8 pagesBerger 1Nikesh PandeyNo ratings yet

- Chapter 4. Solution To End-of-Chapter Comprehensive/Spreadsheet ProblemDocument3 pagesChapter 4. Solution To End-of-Chapter Comprehensive/Spreadsheet ProblemBen HarrisNo ratings yet

- Nasdaq Aaon 2018Document92 pagesNasdaq Aaon 2018gaja babaNo ratings yet

- Mattel - Financial ModelDocument13 pagesMattel - Financial Modelharshwardhan.singh202No ratings yet

- Year 2018 2019 2020: Task 1Document9 pagesYear 2018 2019 2020: Task 1Prateek ChandnaNo ratings yet

- BRITANIADocument6 pagesBRITANIAmeenatchi shaliniNo ratings yet

- Advanced Financial ManagementDocument5 pagesAdvanced Financial ManagementAkshay KapoorNo ratings yet

- IFS Dividends IntroductionDocument2 pagesIFS Dividends IntroductionMohamedNo ratings yet

- SV CMA DataDocument25 pagesSV CMA DataRaja SekharNo ratings yet

- Sensitivity Analysis On Percentage of Sales 9 11 04Document12 pagesSensitivity Analysis On Percentage of Sales 9 11 04Wan Mohamad Noor Hj IsmailNo ratings yet

- Hypothesis For 2003 and 2004: Profit and Loss Stateme Real Forecast Forecast 2002 2003 2004Document12 pagesHypothesis For 2003 and 2004: Profit and Loss Stateme Real Forecast Forecast 2002 2003 2004FeRnanda GisselaNo ratings yet

- Project ADVANCE FINANCIAL MANAGEMENTDocument11 pagesProject ADVANCE FINANCIAL MANAGEMENTBilal KhalidNo ratings yet

- Book 1Document10 pagesBook 1Sakhwat Hossen 2115202660No ratings yet

- IFS - Simple Three Statement ModelDocument1 pageIFS - Simple Three Statement ModelThanh NguyenNo ratings yet

- Abrar Engro Excel SheetDocument4 pagesAbrar Engro Excel SheetManahil FayyazNo ratings yet

- Creative Sports Solution-RevisedDocument4 pagesCreative Sports Solution-RevisedRohit KumarNo ratings yet

- Almarai's Quality and GrowthDocument128 pagesAlmarai's Quality and GrowthHassen AbidiNo ratings yet

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Real Estate IntroductionDocument16 pagesReal Estate IntroductionSuresh PandaNo ratings yet

- Colgate Annual ReportDocument166 pagesColgate Annual ReportRoopesh PandeNo ratings yet

- IC Marketing Budget Plan 8603Document7 pagesIC Marketing Budget Plan 8603Ando RamNo ratings yet

- 1 Z DB Corp Ltd. A: Match The Columns S.No. Column I Answers Column II CodeDocument3 pages1 Z DB Corp Ltd. A: Match The Columns S.No. Column I Answers Column II CodeSuresh PandaNo ratings yet

- Merger and AcquisitionsDocument3 pagesMerger and AcquisitionsSuresh PandaNo ratings yet

- Capital & ERC Finance CompendiumDocument55 pagesCapital & ERC Finance CompendiumRajan GoyalNo ratings yet

- Q1FY21 Earnings Discussion TranscriptDocument20 pagesQ1FY21 Earnings Discussion TranscriptSuresh PandaNo ratings yet

- Quick Company Analysis PVR Limited: ShikshaDocument10 pagesQuick Company Analysis PVR Limited: ShikshaSuresh PandaNo ratings yet

- Media and Entertainment: July 2020Document36 pagesMedia and Entertainment: July 2020Suresh PandaNo ratings yet

- Bharti Airtel's Financial PerformanceDocument14 pagesBharti Airtel's Financial PerformanceSuresh PandaNo ratings yet

- OperacleDocument2 pagesOperacleSuresh PandaNo ratings yet

- Frequently Asked Questions For Pgpim Program: A Corporate Communications Cell InitiativeDocument3 pagesFrequently Asked Questions For Pgpim Program: A Corporate Communications Cell InitiativeSuresh PandaNo ratings yet

- FTP Chapter 4 As On June 30 2019Document24 pagesFTP Chapter 4 As On June 30 2019Tirth PatelNo ratings yet

- BS AssignmentDocument12 pagesBS AssignmentSuresh PandaNo ratings yet

- Ips Data Upload 6 7 0 TSDDocument92 pagesIps Data Upload 6 7 0 TSDSuresh PandaNo ratings yet

- Luminaire: Signify PresentsDocument3 pagesLuminaire: Signify PresentsSuresh PandaNo ratings yet

- Mini-Baja 90% CompleteDocument59 pagesMini-Baja 90% CompleteamalgtlNo ratings yet

- Machine Learning Risk ModelsDocument26 pagesMachine Learning Risk ModelsSuresh PandaNo ratings yet

- Comparing group performance across 14 categoriesDocument2 pagesComparing group performance across 14 categoriesSuresh PandaNo ratings yet

- Slevin 1986Document9 pagesSlevin 1986YuliaNo ratings yet

- Mental Health and Self-Care ReflectionDocument2 pagesMental Health and Self-Care Reflectionapi-472652222No ratings yet

- Sparsh Gupta 14e-Anti Diabetes MCQDocument12 pagesSparsh Gupta 14e-Anti Diabetes MCQSubodh ChaudhariNo ratings yet

- Inhaled Anesthesia For BirdsDocument18 pagesInhaled Anesthesia For BirdsBianca PaludetoNo ratings yet

- 2021 BTCI FASTING PREPARATION (Part 1) - 2Document2 pages2021 BTCI FASTING PREPARATION (Part 1) - 2Andrew HunterNo ratings yet

- Life, Works and Writings of RizalDocument6 pagesLife, Works and Writings of RizalPatrickMendozaNo ratings yet

- Argumentative Essay - Sample 2 - Students Should Spend Less Time Listening To MusicDocument2 pagesArgumentative Essay - Sample 2 - Students Should Spend Less Time Listening To MusicRidhwan AfiffNo ratings yet

- The AdjectiveDocument3 pagesThe AdjectiveAna DerilNo ratings yet

- Young Consumer Green Purchase Behavior: Sohaib ZafarDocument20 pagesYoung Consumer Green Purchase Behavior: Sohaib ZafarFABIOLA SMITH QUISPE TOCASNo ratings yet

- Term Paper of Operating SystemDocument25 pagesTerm Paper of Operating Systemnannupriya100% (1)

- MUET Reading Task - Print OutDocument5 pagesMUET Reading Task - Print Out萱儿林No ratings yet

- Engineering Prob & Stat Lecture Notes 6Document12 pagesEngineering Prob & Stat Lecture Notes 6EICQ/00154/2020 SAMUEL MWANGI RUKWARONo ratings yet

- Review Center Association of The Philippines vs. Ermita 583 SCRA 428, April 02, 2009, G.R. No. 180046Document2 pagesReview Center Association of The Philippines vs. Ermita 583 SCRA 428, April 02, 2009, G.R. No. 180046Almer Tinapay100% (1)

- Pasan Ko Ang DaigdigDocument1 pagePasan Ko Ang DaigdigJermaine Rae Arpia Dimayacyac0% (1)

- Diff BTW CV and ResumeDocument3 pagesDiff BTW CV and ResumeHabib Ullah Habib UllahNo ratings yet

- Journal All Pages Jan2019 PDFDocument68 pagesJournal All Pages Jan2019 PDFmahadev_prasad_7No ratings yet

- De Thi Hoc Sinh Gioi TP HCM - 2020Document8 pagesDe Thi Hoc Sinh Gioi TP HCM - 2020Vi Nguyen TuyetNo ratings yet

- ARB Inclusion/Exclusion RulesDocument14 pagesARB Inclusion/Exclusion RulesanneNo ratings yet

- Herbal Cosmetics: Used For Skin and Hair: December 2012Document8 pagesHerbal Cosmetics: Used For Skin and Hair: December 2012Mas NuriNo ratings yet

- St. Paul University Philippines: School of Nursing and Allied Health Sciences College of NursingDocument3 pagesSt. Paul University Philippines: School of Nursing and Allied Health Sciences College of NursingKristiene Kyle AquinoNo ratings yet

- Cold War Irma MartinezDocument11 pagesCold War Irma Martinezapi-244604538No ratings yet

- Employees' Adaptability and Perceptions of Change-Related Uncertainty: Implications For Perceived Organizational Support, Job Satisfaction, and PerformanceDocument12 pagesEmployees' Adaptability and Perceptions of Change-Related Uncertainty: Implications For Perceived Organizational Support, Job Satisfaction, and PerformancesatirgNo ratings yet

- Ankit - KP Horary Software - Prashna Kundali Software - Free KP Astrology SoftwareDocument3 pagesAnkit - KP Horary Software - Prashna Kundali Software - Free KP Astrology SoftwareANKIT SINGHNo ratings yet

- "Under The Aegis of Man" - The Right To Development and The Origins of The New International Economic Order Daniel J. WhelanDocument17 pages"Under The Aegis of Man" - The Right To Development and The Origins of The New International Economic Order Daniel J. WhelanDavid Enrique ValenciaNo ratings yet

- Mutuum CommodatumDocument12 pagesMutuum CommodatumArceli MarallagNo ratings yet

- Reflection On Teaching Practice To YLsDocument3 pagesReflection On Teaching Practice To YLsivannasoledadNo ratings yet

- JAC - 2023 - ModelQuestion - 9 - Math 1Document4 pagesJAC - 2023 - ModelQuestion - 9 - Math 1Chandan JaiswalNo ratings yet

- Nistico 2018Document5 pagesNistico 2018Ingrid MaiaNo ratings yet

- Cardiology Pharmacist Guide to Acute Coronary SyndromeDocument38 pagesCardiology Pharmacist Guide to Acute Coronary SyndromeAnonymous100% (1)