You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Golden PitchbookDocument16 pagesThe Golden Pitchbookadsfasdfkj100% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Bocconi PE and VC CourseraDocument6 pagesBocconi PE and VC CourseraMuskanDodejaNo ratings yet

- Internship ReportDocument45 pagesInternship ReportTushar GargNo ratings yet

- Jaipur Rugs Supply ChainDocument11 pagesJaipur Rugs Supply Chainsamir muduli100% (1)

- Chapter 17 Non-Profit-Making Organisations (Clubs and Societies)Document5 pagesChapter 17 Non-Profit-Making Organisations (Clubs and Societies)melody shayanwakoNo ratings yet

- Argumentative EssayDocument2 pagesArgumentative EssayLenielynBisoNo ratings yet

- Business 682 Debate Outline Guidelines and ExampleDocument5 pagesBusiness 682 Debate Outline Guidelines and ExampleZainab AbidNo ratings yet

- Class - Participation - BUS - 682.03 - Summer17Document6 pagesClass - Participation - BUS - 682.03 - Summer17Zainab AbidNo ratings yet

- 1 Contact Information: San Francisco State University (Sfsu) Fin 350: Business Finance SUMMER 2017Document12 pages1 Contact Information: San Francisco State University (Sfsu) Fin 350: Business Finance SUMMER 2017Zainab AbidNo ratings yet

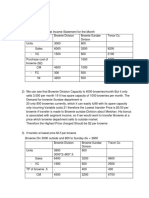

- Brownie Division Brownie Sundae Division Trevor CoDocument2 pagesBrownie Division Brownie Sundae Division Trevor CoZainab AbidNo ratings yet

- SFM Express Notes by Archana Kaithan Ma'AmDocument124 pagesSFM Express Notes by Archana Kaithan Ma'AmNishu DasNo ratings yet

- San Miguel Vs BF HomesDocument31 pagesSan Miguel Vs BF HomesRodney AtibulaNo ratings yet

- Capital Market ScamsDocument19 pagesCapital Market Scamssaibangaru25No ratings yet

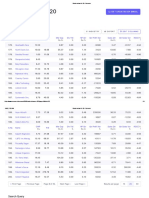

- 8.stocks Below Rs 20 - ScreenerDocument3 pages8.stocks Below Rs 20 - ScreenerVishnu varthanNo ratings yet

- OPM Inventory Balance Reconciliation DocumentDocument6 pagesOPM Inventory Balance Reconciliation DocumentKarthikeya BandaruNo ratings yet

- The Effect of Corporate Social Responsibility, Profitability, and Leverage Toward Tax Aggressiveness With Size of Company As Moderating VariableDocument7 pagesThe Effect of Corporate Social Responsibility, Profitability, and Leverage Toward Tax Aggressiveness With Size of Company As Moderating VariableStella Stella Aprilenia EndesNo ratings yet

- Shubh Nivesh Single PagerDocument2 pagesShubh Nivesh Single PagerANIL TIWARINo ratings yet

- Financial Planning Guide SampleDocument10 pagesFinancial Planning Guide SampleBalakrishnanNo ratings yet

- South Sea SockDocument43 pagesSouth Sea SockSaphi SPNo ratings yet

- Singhal Enterprises Private Limited RRDocument8 pagesSinghal Enterprises Private Limited RRRahulNo ratings yet

- Cotton Greaves FinalDocument34 pagesCotton Greaves FinalGautam KumarNo ratings yet

- Pakistan Remittance Initiative A BriefDocument7 pagesPakistan Remittance Initiative A BriefSniper ShaikhNo ratings yet

- Methylamine Market - Global AnalysisDocument45 pagesMethylamine Market - Global AnalysissomilpixelNo ratings yet

- 3 BR CostingDocument2 pages3 BR CostingDhruv SainiNo ratings yet

- To, Address: Mr. Jagdish Kanjariya C/o Adani MLTPL: Mundra Porbandar House Hold GoodsDocument1 pageTo, Address: Mr. Jagdish Kanjariya C/o Adani MLTPL: Mundra Porbandar House Hold GoodsJagdishKanjariyaNo ratings yet

- CustomDocument3 pagesCustompummysharmaNo ratings yet

- Schroders: Schroder ISF Global SMLR Coms A Acc USDDocument2 pagesSchroders: Schroder ISF Global SMLR Coms A Acc USDSam AbdurahimNo ratings yet

- EVID Syllabus Atty. SengaDocument16 pagesEVID Syllabus Atty. Sengagta0523No ratings yet

- Gaap QuizDocument3 pagesGaap QuizShadab KhanNo ratings yet

- Brockhaus-Long ApproximationDocument8 pagesBrockhaus-Long Approximationmainak.chatterjee03No ratings yet

- SC Fengbin InternationalDocument3 pagesSC Fengbin Internationalaji ajiNo ratings yet

- N1014SQSBFSIXLXIXDocument16 pagesN1014SQSBFSIXLXIXmkasi2k9No ratings yet

- The Process of Allotment of SharesDocument9 pagesThe Process of Allotment of SharesbhupenderNo ratings yet