You might also like

- 1 - Accounting For Partnership Firms - FundamentalsDocument12 pages1 - Accounting For Partnership Firms - FundamentalsAnkit RoyNo ratings yet

- Accounting For Partnership LectureDocument67 pagesAccounting For Partnership LectureChung Gyeum Lee100% (7)

- LLP Organization and Partnership AgreementsDocument6 pagesLLP Organization and Partnership AgreementsAhmad Al-Tarifi Abu JozephNo ratings yet

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah Basir33% (3)

- Michigan Sales Tax License RenewalDocument2 pagesMichigan Sales Tax License Renewalwaqar chNo ratings yet

- Mobil Philippines Exploration Inc Vs Customs Arrastre ServiceDocument2 pagesMobil Philippines Exploration Inc Vs Customs Arrastre Servicerodel_odz100% (2)

- Reaction Paper #11Document5 pagesReaction Paper #11Louelie Jean AlfornonNo ratings yet

- Basic Savings Account-I: Penyata AkaunDocument2 pagesBasic Savings Account-I: Penyata AkaunPuspavathy NadarajahNo ratings yet

- Accounting For Partnerships 2Document35 pagesAccounting For Partnerships 2Lazarus Henga100% (1)

- ENGEXAM IELTS CAE FCE practice materialsDocument2 pagesENGEXAM IELTS CAE FCE practice materialsValentina lamannaNo ratings yet

- Service Agreement - Arnel TaburdanDocument3 pagesService Agreement - Arnel TaburdanJacquelyn RamosNo ratings yet

- CMA Tarun Singhal 7838975916, 9599952599 - Accounting for Partnership FirmsDocument16 pagesCMA Tarun Singhal 7838975916, 9599952599 - Accounting for Partnership FirmsTarun SinghalNo ratings yet

- Class: XII Subject: Accountancy Notes On Partnership-FundamentalsDocument11 pagesClass: XII Subject: Accountancy Notes On Partnership-FundamentalsSurbhi DevnaniNo ratings yet

- Accounting For Partnership Firms - Fundamentals 2021Document183 pagesAccounting For Partnership Firms - Fundamentals 2021JPS J100% (1)

- CBSE Class XII Accountancy Chapter 1 RevisionDocument16 pagesCBSE Class XII Accountancy Chapter 1 Revisionniks525No ratings yet

- 12 Accountancy Revision Notes Part A CH 1Document16 pages12 Accountancy Revision Notes Part A CH 1SukhsanjamNo ratings yet

- HSC Commerce Partnership Final AccountsDocument30 pagesHSC Commerce Partnership Final AccountsViransh Coaching ClassesNo ratings yet

- Accounting For Partnership - Basic ConceptsDocument19 pagesAccounting For Partnership - Basic ConceptsAashutosh PatodiaNo ratings yet

- CH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Document12 pagesCH - 2 Accounting For Partnership Firms: Fundamentals: According To Section 4 of The Partnership Act 1932Laksh KhannaNo ratings yet

- Partnership FundamentalsDocument36 pagesPartnership FundamentalsSuman Choudhary100% (1)

- Topic 5 Accounting For PartnershipsDocument56 pagesTopic 5 Accounting For Partnershipstwahirwajeanpierre50No ratings yet

- Partnership FundamentalsDocument31 pagesPartnership FundamentalsAbhishek KhandelwalNo ratings yet

- Introduction To Partnership AccountsDocument88 pagesIntroduction To Partnership Accountssaheer100% (1)

- Chapter 6: Appropriation of Profits: Rohit AgarwalDocument4 pagesChapter 6: Appropriation of Profits: Rohit AgarwalbcomNo ratings yet

- Chapter 7: PARTNERSHIPDocument45 pagesChapter 7: PARTNERSHIPSuresh LamsalNo ratings yet

- 10 PartnershipDocument42 pages10 Partnershipravic25100% (1)

- 12 AccountancyDocument4 pages12 AccountancyAbhishek DhillonNo ratings yet

- Accounting For PartnershipsDocument43 pagesAccounting For PartnershipsAqibNo ratings yet

- 18bco31c U1Document4 pages18bco31c U1sc209525No ratings yet

- Study Material CH.-1 Fundamentals of Partnership 2023-24Document28 pagesStudy Material CH.-1 Fundamentals of Partnership 2023-24vsy9926No ratings yet

- Partnership AccountDocument67 pagesPartnership Accounttetteh godwinNo ratings yet

- Partnership AccountingDocument8 pagesPartnership Accountingferdinand kan pennNo ratings yet

- Fundamentals PDFDocument103 pagesFundamentals PDFDhairya JainNo ratings yet

- Class 12 Subject Accountancy Partnership (Fundamentals)Document4 pagesClass 12 Subject Accountancy Partnership (Fundamentals)Asra KitabNo ratings yet

- Partnership AccountsDocument26 pagesPartnership Accountsoneunique.1unqNo ratings yet

- Buku Nota PertnershipDocument33 pagesBuku Nota PertnershipmaiNo ratings yet

- PL Appropriation AcDocument6 pagesPL Appropriation AcShivangi Aggarwal100% (1)

- Part 1 Partnership BasicDocument11 pagesPart 1 Partnership BasicSagar YadavNo ratings yet

- Parnership Final Account Notes PDFDocument33 pagesParnership Final Account Notes PDF9221068415100% (1)

- What Is A PartnershipDocument15 pagesWhat Is A PartnershipApparatus BoxNo ratings yet

- Partnership Accounting BasicsDocument35 pagesPartnership Accounting BasicsERICK MLINGWA50% (4)

- Journal Entries For PartnershipsDocument11 pagesJournal Entries For PartnershipsRosette Revilala100% (1)

- Ahmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesDocument4 pagesAhmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesMohamed MuizNo ratings yet

- Ahmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesDocument4 pagesAhmadhiyya International School Syllabus: Subject: ACCOUNTING-Gr-11-Unit: Partnership Accounts-NotesMohamed MuizNo ratings yet

- Accounting For Partnership - UnaDocument13 pagesAccounting For Partnership - UnaJastine Beltran - PerezNo ratings yet

- Partnership profit distributionDocument19 pagesPartnership profit distributionpayal sachdevNo ratings yet

- Partnerships Organization and OperationDocument6 pagesPartnerships Organization and OperationAshraf Uz ZamanNo ratings yet

- Mediocre Non-Profit OrganizationDocument12 pagesMediocre Non-Profit OrganizationveenaNo ratings yet

- Project On Partnership Accounting PDFDocument17 pagesProject On Partnership Accounting PDFManish ChouhanNo ratings yet

- Fundamantal of Partnership PPT As On 21 12 2020Document50 pagesFundamantal of Partnership PPT As On 21 12 2020jeevan varma100% (1)

- 12 Accountancy Revision Notes Part A CH 6Document13 pages12 Accountancy Revision Notes Part A CH 6niks525No ratings yet

- Profit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership FirmDocument10 pagesProfit & Loss Appropriation Account, Admission, Retirement and Death of A Partner, and Dissolution of A Partnership Firmd-fbuser-65596417No ratings yet

- Chapter 1 Accounting for partnership firms fundamentalsDocument16 pagesChapter 1 Accounting for partnership firms fundamentalsVansh SharmaNo ratings yet

- Unit 5Document37 pagesUnit 5Rej HaanNo ratings yet

- Study Note 4.2, Page 169-197Document29 pagesStudy Note 4.2, Page 169-197s4sahith0% (1)

- Accounts Class 12th English MediumDocument27 pagesAccounts Class 12th English Mediumas5634703No ratings yet

- 12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01Document18 pages12 Accountancy ImpQ CH05 Retirement and Death of A Partner 01praveentyagiNo ratings yet

- Chapter 1 - Formation of PartnershipDocument31 pagesChapter 1 - Formation of PartnershipAisyah BasirNo ratings yet

- Final Account of Local Partnership FirmDocument12 pagesFinal Account of Local Partnership FirmSourabh SabatNo ratings yet

- Chapter 2 Dissolution and Liquadation of PartnersipDocument17 pagesChapter 2 Dissolution and Liquadation of PartnersipTekaling NegashNo ratings yet

- 4 General Accounts of Partnership FirmDocument16 pages4 General Accounts of Partnership FirmNisarga T DaryaNo ratings yet

- Partnership AccountingDocument14 pagesPartnership AccountingLongWongChengNo ratings yet

- Chapter Nine: Partnerships: Formation and OperationDocument44 pagesChapter Nine: Partnerships: Formation and OperationkjkjkjfffffffNo ratings yet

- Partnership FirmDocument15 pagesPartnership FirmNavpreet SinghNo ratings yet

- Lecture Notes - Chapter 15: Sole Trader and Partnership Fss Under Uk GaapDocument34 pagesLecture Notes - Chapter 15: Sole Trader and Partnership Fss Under Uk GaapThương ĐỗNo ratings yet

- Tax Invoice: G R U K Power Plant Consultants LLPDocument1 pageTax Invoice: G R U K Power Plant Consultants LLP150819850No ratings yet

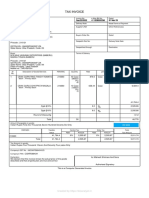

- Tax Invoice: Created by Https://bizanalyst - inDocument1 pageTax Invoice: Created by Https://bizanalyst - inSavera DixitNo ratings yet

- Raj Narain v. Indira Gandhi 1972 SC (Or. 11)Document12 pagesRaj Narain v. Indira Gandhi 1972 SC (Or. 11)Aanika AeryNo ratings yet

- Dwnload Full Operations Management 11th Edition Heizer Solutions Manual PDFDocument28 pagesDwnload Full Operations Management 11th Edition Heizer Solutions Manual PDFavosetmercifulmww7100% (14)

- Civil SocietDocument4 pagesCivil SocietAbdi Mucee TubeNo ratings yet

- SL 1063Document3 pagesSL 1063Yarisa VangeNo ratings yet

- China Post Shipping LabelDocument2 pagesChina Post Shipping LabelLuxury Palace100% (1)

- UP Urban Planning and Development Act-1973Document16 pagesUP Urban Planning and Development Act-1973ar_vikram100% (2)

- An Overview of Financial Management Forms of Business Organization PDFDocument2 pagesAn Overview of Financial Management Forms of Business Organization PDFPhil SingletonNo ratings yet

- CMA DataDocument23 pagesCMA DataAnupam JyotiNo ratings yet

- BEI&W - Mythili - PPT Presentation Write UpDocument2 pagesBEI&W - Mythili - PPT Presentation Write UpKOTHAPALLI SAI SARADA MYTHILINo ratings yet

- Isa 810 - PreciDocument1 pageIsa 810 - PreciJennifer GaiteNo ratings yet

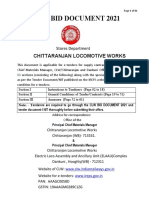

- CLW Bid Document 2021Document61 pagesCLW Bid Document 2021abhishekgupta9990No ratings yet

- Obstacles To Empowerment Local Politics and CivilDocument20 pagesObstacles To Empowerment Local Politics and CivilJeindrixz AsadilNo ratings yet

- DIN EN ISO 9013 062003-EnDocument27 pagesDIN EN ISO 9013 062003-EnChristopher MendozaNo ratings yet

- Aefpm5487a 2023Document4 pagesAefpm5487a 2023enjoy enjoy enjoyNo ratings yet

- Presentation Clarification Meeting - MV LV 2018Document15 pagesPresentation Clarification Meeting - MV LV 2018Bea MokNo ratings yet

- Acceptance of Trust As Executor: Complete in DuplicateDocument1 pageAcceptance of Trust As Executor: Complete in DuplicateBogdan RadulescuNo ratings yet

- Cancellation PDFDocument4 pagesCancellation PDFgmanju207No ratings yet

- Q1 Results Canara Bank 30.6.23Document31 pagesQ1 Results Canara Bank 30.6.23Hitendra KumarNo ratings yet

- Government of Pakistan notifies E-Pak-Procurement Regulations 2023Document35 pagesGovernment of Pakistan notifies E-Pak-Procurement Regulations 2023syed aamir shahNo ratings yet

- SF Upper Int 11D Elesson Answers PDFDocument1 pageSF Upper Int 11D Elesson Answers PDFAlina NikitinaNo ratings yet

- The Legalzoom Team: Ship ToDocument5 pagesThe Legalzoom Team: Ship ToRichard E ObedNo ratings yet

- CSR Assignment of UBL BankDocument6 pagesCSR Assignment of UBL BankZubair AhmedNo ratings yet